A business journal from the Wharton School of the University of Pennsylvania

What’s Behind Blackstone’s Investment Success?

May 31, 2016 • 10 min read.

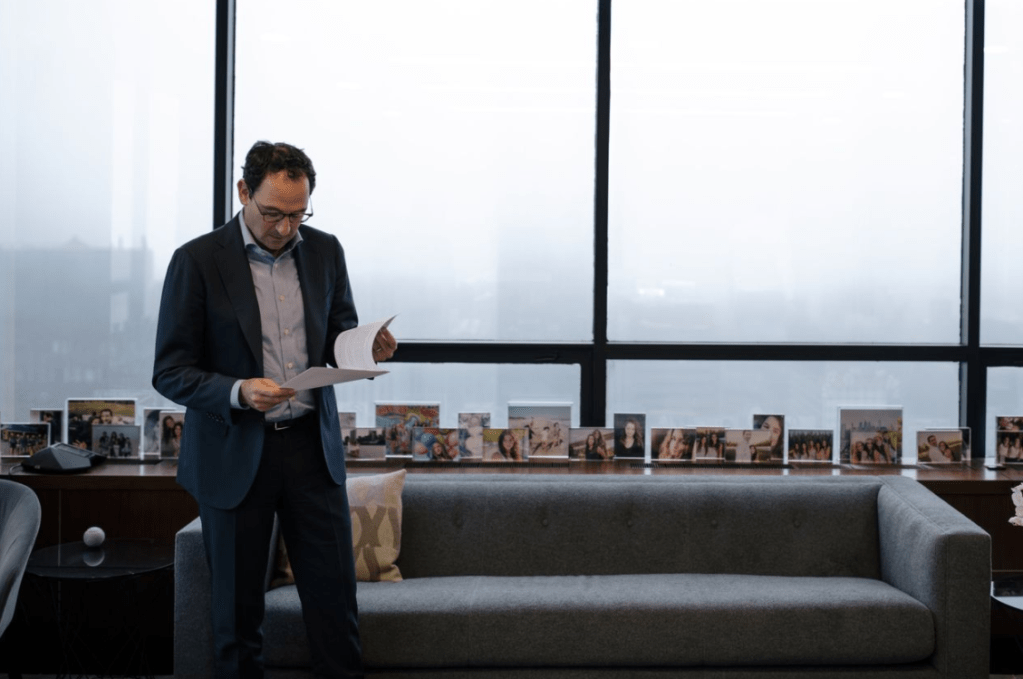

Blackstone CEO Stephen Schwarzman says a key to his firm’s investment success is understanding how people behave.

- Finance & Accounting

As the largest private equity firm in the world, the Blackstone Group understands firsthand what it takes to keep a big company nimble.

“Our biggest challenge is, how do we keep expanding and [still] keep the firm intimate and flexible and responsive?” Stephen Schwarzman, chief executive, chairman and co-founder of Blackstone, told an audience of University of Pennsylvania students recently. On stage at Penn’s Annenberg Center, he discussed the progression of his long career and the key factors responsible for his remarkable success. The moderator was his long-time friend, Howard Marks, now co-chairman of Oaktree Capital Management.

Schwarzman, who established Blackstone in 1985, began his Wall Street career at Lehman Brothers in 1972. In those days, “it was a completely different world than we have now,” he recalled. “It was great because we didn’t have what we have now — that is to say, specialists. Now everybody is a specialist at something. We were all generalists; so if you were in corporate finance, you did literally every type of activity, from rating agency presentations, to private placements, to equity offerings, debt offerings, mergers — anything that somebody needed, you did it. That was a really important element of my career. Because you sort of knew something about everything. In that way, you could sense trends, changes and so forth.”

Although the path of least resistance after Lehman would have been to start another investment bank, Schwarzman didn’t go there. Instead, he went into investment management. “We tried to figure out, ‘What could we do that everybody else in the world wasn’t doing?’ That’s an important way to think; not just trying to do better at what everybody else is doing,” he said.

The strategic plan that arose was, first of all, to enter the corporate advisory business, which is what Schwarzman had been in, and where he knew a lot of people. Going into the advisory business meant that no capital was required. “It’s always good to not need capital because then you don’t have to dilute your ownership. So we did that.”

The second piece of the strategic plan was to go into what was then called ‘leveraged buyouts.’ “A lot of my friends were the young people who were starting the other firms at that time,” such as KKR & Co. and the now defunct Forstmann, Little & Co., Schwarzman said. Those people had trouble getting anybody to represent them because “they were very small companies that had leveraged structures; it all seemed risky. Because I knew them, I took them on as clients.”

“We must have sent out 500 letters that said, ‘we’re in business; let us represent you.’ But nobody hired us. This was a very depressing moment.”

A major deal that attracted Schwarzman’s attention was the $380 million buyout of Houdaille Industries by Kohlberg Kravis Roberts that laid out the whole structure of leveraged buyouts (LBOs), which were “then kind of a secretive type of thing,” he recalled. “You looked at it and it was an amazing way to make money — just amazing. I knew I wanted to do that. I tried to get Lehman to start that, and we actually got a deal but it was turned down by the management committee [at Lehman], which is one reason they ended up broke. They weren’t always great decision makers, in my view.”

A third foundation of the strategy took advantage of the fact that the financial sector was going through an “amazing consolidation after May Day 1975 [when the SEC deregulated the brokerage industry, ushering in lower trading fees]. Commissions had basically been fixed, for, I guess, 200 years, and this led to a lot of different popcorn stands that were highly inefficient cost structures. These companies started combining, and it became very clear that there was going to be a massive increase in the size of firms.” How dramatic was that consolidation? Schwarzman said when he joined Lehman, “We had about 550 people but 25 years later, we had 30,000.”

The consequences of that consolidation were significant. “When I was at Lehman, I knew everybody by sight, a lot of people by name. But when you have a firm that has 30,000 people, it is a veritable impossibility. I thought that, strategically, there were a lot of people who liked to be in smaller-sized organizations and what we should do is to recruit those people when we saw an amazing opportunity — a market shift, something unusual happening. And that people who were ‘10s’ [highest-rated] on a scale of 10 [in terms of their capabilities], would be available simply because they didn’t want to work for these ever-consolidating big firms” that had become impersonal. “We could strengthen these businesses and have them generate intellectual capital, which we could use to make the business stronger.”

So Schwarzman laid out his plan, and waited for the phone to ring. Only, it did not ring. “We must have sent out 500 letters that said ‘We’re in business; let us represent you,’ but nobody hired us. This was a very depressing moment.” After waiting two weeks, they called prospects again, and “got lucky. Squibb, the pharma company, hired us for $50,000.” It was a modest but important step for Blackstone, which currently has more than $340 billion in assets under management. Looking back on his progress, Schwarzman said, “That sounds like a good trip, but the journey is always much rougher people imagine. But the strategic plan of the firm never changed. It is still a great plan, and we’re still executing on it.”

“This depersonalizes decision-making, because if … everyone is attacking you all the time, then no one is attacking you.”

Blackstone’s System for Success

As for Blackstone’s successful track record, Oaktree’s Marks noted wryly that the dearth of investment errors took away opportunities for his own firm to profit from them. “Our portfolios over the years have been a litany of private equity firms’ mistakes, but Blackstone is under-represented” among them. Oaktree’s main business is investing in distressed debt, which “primarily attempts to take advantage of the mistakes of others and of private equity firms. But Steve has not done his part to give us investment opportunities.”

Why has Blackstone made so few mistakes? Schwarzman traced the origins of his investment philosophy back to the fact that he “can’t stand” the idea of losing money. “It is just something that goes to the core of the person,” he said. “If you start out delivering newspapers, and shoveling snow and doing all the stuff you do in suburban Philadelphia to make money” as a young man, then “you don’t want to go backwards.”

Still, in the early days, “we didn’t have an investment process,” Schwarzman said. To his deep regret, one of his early customers lost $32 million, and he vowed that he was never going to let that happen again. “This is the risk of starting a business when you don’t know what you are doing, other than having great enthusiasm.” Embarrassed, Schwarzman and his colleagues set up an “amazing system,” which they still use today.

“They actually don’t understand how people behave. And so, it’s not distributed risk assessment”

A key to Blackstone’s investment success is a system that takes emotions out of proposing and vetting investment ideas. “If you are in any business where people are looking for approval of their proposal, if you don’t approve their proposal, they’ll think you don’t like them. You don’t value them.” So Blackstone set up a process to remove any emotional blowback by insisting that dissent should be backed by analysis. It consisted of “pretty rigid rules for anything that we are going to buy or invest in. There has to be written analysis of that, and it has to identify all the risk factors, with the objective of deciding how you could lose money — and it could never happen.”

Next, he related, “I realized that if one person was criticizing the deal, then the person who brought the deal and was leading the team wouldn’t like that person; and they would try to retaliate in some way, which stops everyone from being objective about the investment if it’s not such a good investment. So I insisted that everyone around the table speak, and they could only speak about analytic weaknesses in the deal and risks in the deal. So this is all geared to not losing money.”

The goal of the system is this: “This depersonalizes decision-making, because if everyone is following through” and addressing these issues in detail, “and everyone is attacking you all the time, then no one is attacking you.” By the time the analysis is complete, “the responsibility for that investment no longer resides with that team of people. It’s all the people at the table who own that.” If anything goes wrong, later on, the common feeling is, “ We got it wrong. That way, people are very comfortable going forward. And the chance that we lose money is really de minimis.”

“We are in the no-secrets business. Everybody is expected to pay attention and learn.”

Where Other Firms Fail

Why don’t other organizations undertake a similar process? Schwarzman explained, “They fall down in a lot of ways. First, they put somebody in charge of risk; that’s a person. … They believe in delegating this to someone who is setting this up as a profit center. Worse, they actually don’t understand how people behave. And so, it’s not distributed risk assessment.”

What is Blackstone’s greatest challenge in managing internal corporate relationships? “The key is that nobody wants to work in a big, impersonal place. Who would want to do that? That’s not fun. That’s one of the reasons why people start new businesses,” Schwarzman said. The firm’s challenge is to keep growing while maintaining intimacy, flexibility and responsiveness. Although Blackstone has become a global corporation, “Technology has solved this for us. We have offices all over the world.”

Every Monday, “each of our business lines — private equity, real estate, credit, hedge funds — meets as a group” through video conferencing. “We first look at what is going on in the world — any changes in the companies that we own that we can see as a trend. We go over [our investments all over] the world. Everybody is in that room, and anybody can talk. And anybody can ask questions about what we are doing,” Schwarzman said.

“We are in the no-secrets business. Everybody is expected to pay attention and learn. For younger people, this is like having a master class. As the older people in the group start asking questions about things — say, about tactics or industries or what’s going on — this is actually a lot of fun. Everybody likes being included. Nobody likes to be subordinated. This way, people learn about cycles. They learn about where we are in the cycle — whether it’s the U.S. economy, whether it’s the global economy, by industry and, ultimately, by asset class.”

More From Knowledge at Wharton

How Low-income Households Can Secure Their Retirement Finances

The Impact of Automation on Corporate Decision-making

Is College Worth It? | Peter Cappelli

Looking for more insights.

Sign up to stay informed about our latest article releases.

Blackstone Private Wealth Solutions

The wall street journal profiles blackstone’s firmwide growth and thematic investing strategy.

March 22, 2021

The Wall Street Journal today profiled how Blackstone in recent years has increasingly focused on investing in fast-growing sectors and high-conviction investment themes with strong secular tailwinds.

Blackstone has deployed significant capital across each of its businesses in areas such as life sciences, last-mile logistics, renewables, digitization, and online content that have benefitted from ongoing shifts in consumer behavior and demographics. The story also covers in depth Blackstone’s emphasis on cross-firm collaboration in investing behind these themes to leverage its scale and intellectual capital for its investors.

Blackstone’s President and COO Jon Gray told The Wall Street Journal in an interview for the piece: “Investing is about looking forward, but the future is now coming faster. You want to be exposed to businesses that benefit from this change.”

To read the article, please click the following link or the photo from the story below.

Related Articles

Investment Strategy

Joe Zidle: Optimism and Uncertainty on the Menu

Market Views

Jon Gray on the Early Stages of a Capital Markets Recovery

Private Credit: From Mid-Market to Real Economy Financier

Connect with our dedicated team that works directly with private wealth managers, family offices and financial advisors to help their clients access alternative solutions., individual investors.

Please contact your financial advisor to learn more.

Financial Professional Inquiries

Financial professional contact request submission.

WORK Email* First Name* Last Name* Company Name Phone Number Submit

[email protected] | +1 (212) 583-5200

This site and the materials herein are directed only to financial advisors or other investment professionals and are not intended to be shown to the general public.

I acknowledge that I am a financial advisor or investment professional.

Brightcove Lightbox

Understanding Blackstone Group’s Investment Strategy

By Jane Winterbottom – International Banker

The returns that Blackstone has earned since its establishment just over three decades ago are impressive by any standards. Its private-equity funds have made an average annual return of 19 percent; its real estate funds have realised 20 percent; while its credit funds have registered 14 percent. It started operations in 1985 with a balance-sheet size of $400,000. Assets under management have grown rapidly and currently stand at $361 billion.

What are the factors that have contributed to making co-founder and CEO Stephen Schwarzman’s Blackstone Group one of the largest and most successful private-equity firms in the world? Schwarzman says that his investment philosophy hinges on his personal belief that it is wrong to lose money in a deal. While that may sound simplistic, Blackstone’s timing and its execution abilities have given it a great advantage.

Blackstone’s real estate business . The initial fundraising exercise undertaken by the company in 1987 raised $635 million. It was completed just before the stock market plunged in October 1987. The savings and loan (S&L) crisis was picking up momentum at that time. Inflation was climbing, and so were interest rates, but the rate of interest that S&Ls could pay was set by the federal government. Consequently, there was a massive outflow of funds from S&Ls, leading to a large number of them failing.

The thrift industry in Texas was hit the hardest. An illustration of the extent of the problem is provided by the decision of the Federal Savings and Loan Insurance Corporation to burn some under-construction condos financed by a recently defunct Texas S&L instead of trying to sell them. At that time, the government-owned Resolution Trust Corporation began selling billions of dollars of assets. Blackstone was flush with cash and bought a large number of buildings in Arkansas and Texas at rock-bottom prices, establishing its real estate business that now has 117,000 multifamily units and144 million square feet of office space globally, among its other assets.

Purchase of General Electric’s commercial real estate portfolio . More recently, Blackstone bought properties valued at $14 billion from GE Capital in a transaction reported to have been done at the book value of the assets “with a built-in mechanism to mitigate Blackstone’s risk” for purchasing the properties after conducting only a brief due diligence. The deal included 24 million square feet of office space in the US and 18 million square feet of commercial properties and shopping malls in Europe.

A report in Forbes states that GE selected Blackstone because it was the only company with the bandwidth to handle a transaction that involved commercial mortgages across six countries. A hundred Blackstone employees completed the complex due-diligence process in just four weeks. Crucially, Blackstone also had the resources to finance the acquisition quickly.

Raising permanent capital. Once again, Stephen Schwarzman got his timing just right when he made his initial public offering (IPO) in June 2007. A sum of $4.1 billion was raised at an IPO price of $31, valuing the company at $33.6 billion. But just two years later, the price of Blackstone’s partnership units, the formal name for its shares, fell to $3.87. Referring to the precipitous fall in the value of the company’s shares, Schwarzman said, “It was a deluge which didn’t have anything to do with us”. Currently, the shares trade in the $25 range.

Blackstone could have been much bigger . According to a story in The Wall Street Journal , BlackRock, an investment-management company, started off as a venture promoted by Schwarzman back in 1988. But Laurence Fink, the person heading BlackRock, and Schwarzman decided to part ways 10 years later. BlackRock currently has $5.1 trillion in assets under management, and Schwarzman says that one of his greatest regrets is that BlackRock is not a part of Blackstone.

Blackstone’s deal-approval process . The firm’s ability to eliminate emotions when deciding upon a proposal is one of its greatest strengths. Each proposal has to meet a rigid set of rules before it is considered. A crucial part of the process is to identify how the idea could lose money. The analysis has to then demonstrate that it is highly unlikely that such an eventuality would arise.

Schwarzman insists that everyone at the table speak and provide an objective view of the weaknesses inherent in a proposal. The purpose of this exercise is to “depersonalise” the proposal and make every participant responsible for the decision and not just the team that is putting it up. This system has worked very well for the firm over the years and is at the core of its success.

Investment Banking’s Changing Face

New us strategy at credit suisse: a bank for billionaires, related articles, sheinbaum’s election victory is a ringing endorsement of..., what a new labour government means for the..., does soaring industrial demand in 2024 signal a..., what’s behind china’s gold-buying spree, why nations are rushing to join brics+, what the fed’s latest stress test says about..., lifting the veil: identifying ultimate beneficial owners, after much political turbulence, can a new faye-led..., the environmental impact of cloud computing and the..., why soybean prices have continued to fall throughout..., how the banking sector can conquer the role..., s&p’s downgrade reflects france’s fragile fiscal position, ethiopian banking sector’s development given major boost by..., the family-office boom is proving hugely positive for..., us banks: take a lesson (or three) from..., leave a comment cancel reply.

Save my name, email, and website in this browser for the next time I comment.

Full Name Email Address By subscribing I accept the privacy rules of this site

How Blackstone is helping to build India’s next generation of global companies

This interview is part of a series of India Ahead conversations with visionaries, future builders, and thought leaders on what it will take to drive India’s growth over the next 25 years.

A combination of investments in India and a doubling down across Asia appears to be a successful strategy for Blackstone’s Private Equity group. In India, its portfolio has a total market value of $60 billion. Marquee deals include purchasing a majority stake in IT service provider Mphasis, acquiring the glass packaging business of Piramal Group, and exiting from business service provider Intelenet for $1 billion (in 2018).

Leading the program is Amit Dixit, Blackstone’s head of Private Equity in Asia, who has been with the company since 2007. In a conversation with McKinsey’s Vivek Pandit, Amit discusses how the Indian market has evolved over the past decade and Blackstone’s approach to building value over time by using innovative technology and world-class talent. The following is an edited version of their conversation.

McKinsey: Blackstone Asia’s record is more India-centric than that of most regional funds. What makes you bullish on India?

Amit Dixit: India as a country offers scale. We have $60 billion in assets across private equity and real estate in India. Very few countries in emerging markets offer that scale. Second, India has a combination of both a large domestic market and a large export opportunity. Again, it’s a rare combination to find both in emerging markets, and we have played both. We have made several investments in export industries where India has a global competitive advantage—software, services, pharmaceuticals, and auto components—and several investments domestically in consumer, financial, healthcare services, and, biggest of all, real estate. These strengths are in addition to well-known aspects of India, including democracy, the rule of law, a large middle class, and our high GDP growth rate.

McKinsey: What would you say are the main contributors to Blackstone’s success in India?

Amit Dixit: When I look back on what has worked, I think it’s a few things. First, because our strategy is to be a value-adding investor, we need deep domain focus. We’ve bought and sold mostly in the same sectors for the last decade, and we haven’t deviated outside of that, so we have the right people, the right network, and the right domain expertise.

Second, we have learned to be a builder of businesses, not just a buyer of businesses. If the opportunity is only to buy and sell, that’s not for Blackstone. We buy to build, and in every situation we are looking for an opportunity to build the platform we have. That is something we believe is unique and has now been part of our DNA for over a decade.

Third, it’s all about alignment and partnerships with management, fellow shareholders, founders of companies, promoters, and owners. You have to row in the same direction and be a trustworthy, transparent partner. We dedicate an inordinate amount of emphasis to get that partnership and alignment right. One way to do it is to make sure everybody is completely aligned on the equity value creation plan. We are very transparent as to what our objectives are and what the investment plans are, and we agree on that up front.

Next, I would say we’ve learned, in the last three years, that technology is no longer a vertical. Technology is a horizontal. Every business is a technology business. If you get the technology transformation right, you get two benefits: you get accelerated revenue growth because you’re on trend, and, importantly, you get a very strong multiple upon your exit at the IPO because you future-proof the business, and the next investor is seeing a ten-year runway. For example, we converted Sona Comstar from a combustion engine auto company into an electric vehicle company, Mphasis from a traditional outsourcing company into a cloud migration company, and Aakash Educational from a physical-education company into an “edtech” company.

The last point is about management. The talent pool in India and the quality of management are very strong. We have learned it is key to align the talent with the shareholder and customer objectives. We think of ourselves as almost a glorified head-hunting firm because at all times we’re ensuring that the right people, with the right alignment, are in critical leadership roles in our companies. And when I say “leadership role,” I don’t mean just the CEO or CFO. Typically, our management teams have equity programs extending to 150 to 200 people. You need to get that right because if you get the management right, magic happens. The change in behavior between that same leader who was earlier a manager and is now an owner is dramatic. We have recognized the power of ownership and brought that equity ownership culture into the Indian management teams, and that’s worked well.

McKinsey: For a long time, a lack of adequate exits and options deterred some investors from India. How does the Indian private equity market stack up from a risk–reward perspective, and how has Blackstone adapted to account for this?

Amit Dixit: There have been two big changes in the market over the last decade. One, the shift from minority investing to what we call control deals, where a foreign investor owns more than 51 percent of the company. When Blackstone started in India, it was a rarity to have a control deal. It was almost a 100 percent minority investment market in India. If you fast-forward to today, we can see that control deals are becoming more common. And both control and minority deals are now much larger in size than they used to be. That’s a fundamental change.

We can see that control deals are becoming more common. And both control and minority deals are now much larger in size than they used to be. That’s a fundamental change.

The second big change is exits. To your point, it was always a great market to invest in but a difficult market to harvest. If you talk to the limited partners or investors, that would have been the most common complaint five years back. That has changed because the markets in India actually have done well, and not just the IPO market but the M&A market as well. We have seen exits from dividend recaps, from IPOs, secondary sales, trade sales, private equity sales, and multiple exits.

That’s a big change in our strategy. We have always focused on being a business builder and having a very active large stake in a company. What that gives us is exit optionality. It’s important in emerging markets to have exit optionality because IPO markets can be few and far between, as you saw between 2011 and 2013 in India, when the IPO market slowed down. Even in the last six months, we’re seeing IPO windows close. If you’re a minority investor, you’re largely stuck with an IPO exit, but having multiple options and exercising those options make a big difference. The Indian market is becoming deeper, larger, with more exits.

McKinsey: There is tremendous political and economic volatility today. How are private market investors like Blackstone responding to this uncertainty?

Amit Dixit: I would say there are a few aspects to this. First, you don’t have to put your head in the storm. We tend to be long-term investors and don’t have to either invest or exit anything right away. We don’t get caught up in the short term. I think that’s important, and, thankfully, our capital gives us the flexibility to do so because we raise long-term capital.

Second, in many businesses, inflation is so hard to pass on to your customers that it’s important to focus on costs. You have to balance the growth agenda with the productivity agenda. You have to make sure that your business is efficient because your customers expect you to do so, and the benefit will come when the inflationary environment eases. At that time, you will reap the rewards of being very prudent in this environment.

Third, there is an opportunity to, potentially, make acquisitions or be more aggressive in gaining market share. We have an acquisition conversation going on in every one of our companies or, in some companies, multiple acquisition conversations. We think it’s a very good environment for talking acquisitions and playing offense to increase market share.

In terms of new investments, we are navigating the environment with patience and dialing up on quality. As a US dollar investor, the world does look a lot cheaper. In most markets, keeping India aside, investors are now trading at a discount to the ten-year averages of the long-term market. We want to dial up on the quality, and quality is always expensive. It won’t be cheap, but it’s cheaper than it used to be 12 months back.

That’s where being a builder comes in, because whatever you are buying will be relatively expensive in somebody’s eyes unless you have a differentiated point of view on what you build, not what you’re buying. In our investment committee approval meeting , we have that value creation plan—what we call the business building plan—up front. Many years back, those plans would come into place six months after the investment or even a year after. Now, they come six months before the investment. As soon as an investment closes, you hit the ground running.

McKinsey: As someone who works closely with family businesses and entrepreneurs in India, what advice would you have for families seeking to partner with private equity firms and build high-performing organizations?

Amit Dixit: We have, over the last 15 years, partnered with many family-owned businesses. It’s important to have the business governance ready. Good governance is good business. What do I mean by that? Have a well-reputed accounting firm do your audits, have a diversified board, have the right people, have proper financial controls in place, and put an ERP [enterprise resource planning] system in place. For any kind of activity you want to do—whether it’s an IPO or private equity—it’s just good governance. Even growing your own business is very hard to do if you don’t have this basic infrastructure in place.

Second, what has contributed to Blackstone’s success is what is going to contribute, and is contributing, to the success of family-owned businesses: attract, retain, and incentivize best-in-class management. I cannot emphasize how much of a difference a great manager versus a good manager can make. It’s a very big point, but for great managers to succeed, you have to give them the operating freedom, the empowerment, and the ability to execute, and you do not second-guess on the strategy. That requires a certain amount of framework alignment, and I think the onus is on family businesses to make it work.

The third thing, I would say, is to focus. India is growing and has become very competitive and very organized. There are multiple competitors in each space. You have to put in your 150 percent no matter where you are. Otherwise, you cannot even have a shot at winning. Pick your spots, pick your focus, and don’t have that diversified sort of approach. Yes, you will have to make sharp choices. It’s not easy.

McKinsey: Looking ahead, where do you see the greatest investment opportunities in India over the next five to ten years?

Amit Dixit: From the Indian perspective, broadly, there can be two buckets: domestic and exports. In the domestic area, the digital consumer is a long-term theme. I’m purposefully using the term “digital consumer” and not “consumer” because I think the trend of consumption is becoming digital, whether it’s consumption in healthcare or consumption in retail moving to digital channels. Another big theme is the aging population and the impact on life sciences and healthcare. And the growth of financial services in India as GDP grows is expected to drive Indian savings away from real estate, gold, or other physical assets into financial assets. So, financial services is another multidecade trend.

In the exports area—opportunities where India has a global competitive advantage—exporting software services is a classic. It’s an almost $200 billion export industry for India. It is a big sector for Blackstone itself, both in private equity and real estate or real-estate tenants. We have also had very strong success now with manufacturing, where the opportunity—what we call the make-in-India opportunity— is much bigger than what we have tapped. India can be a manufacturer of a lot more goods, including pharmaceuticals and chemicals.

These are some of the themes I would focus on, both domestically and from an export standpoint, for a ten-year point of view.

Amit Dixit is senior managing director and head of Asia for Blackstone Private Equity. Vivek Pandit is a senior partner in McKinsey’s Mumbai office.

This article was edited by Astrid Sandoval, an executive editor in the London office.

Comments and opinions expressed by interviewees are their own and do not represent or reflect the opinions, policies, or positions of McKinsey & Company or have its endorsement.

Explore a career with us

Related articles.

Inside Rishad Premji’s quest to create a high-performing culture at Wipro

India as a pharma innovation hub: An interview with Dr. Reddy’s G. V. Prasad

Why Infosys’s cofounder Nilekani is urging leaders to use tech for good

- The Investment & Markets Channel

Blackstone & QTS to spend $8bn building new data centers, as investor prepares for “once in a generation” AI boom

Has already spent $1bn on buying land for AI land grab

Blackstone’s $68 billion flagship property fund is selling assets and preparing to spend billions on data centers.

The Financial Times reports that the Blackstone Real Estate Income Trust, or Breit, plans to pump $8bn into building new data centers through its asset QTS Data Centers, as it predicts a surge in artificial intelligence workloads.

Breit spent around $60 billion on properties from hotels, warehouses, and self-storage facilities from the beginning of 2021 to the third quarter of 2022. But then the trust reversed course, and has since made no large purchases, instead selling more than $10bn in assets.

The company plans to sell a Texas resort for $800m, and self-storage properties for $2.2bn, as it raises cash to build data centers for a potential AI wave.

“Large technology companies are in the midst of an AI arms race which we believe will be a once-in-a-generation engine for future growth in data centers and is driving tremendous demand on the ground,” Breit told investors.

The FT reports that Blackstone has committed to spending more than $8bn to build new data centers, likely for hyperscalers. The investment is through QTS Realty Trust, which Blackstone acquired for $10bn in September 2021.

The company has already spent more than $1bn to buy land to build new data centers in five states across the US, and QTS has tripled its leased space since it was acquired. The company is preparing to further double its size, the FT reports, and QTS’ valuation has risen to about $20bn.

DCD spoke to QTS' chief growth officer earlier this year about the company's plans to build multiple gigawatt campuses. “All of the power in the state of Arizona today is seven gigs,” Tag Greason told us. “And we're going to them and saying, 'we'd like to build one gig.'”

The new investment comes as analysts and industry figures predict a wave of AI investment. Analyst outfit Dell'Oro Group this month said that data center capex will hit $500 billion by 2027 to support AI workloads, while TD Cowen said that around ~2.1GW of data center leases were signed in the last 90 days driven by AI requirements - a new record.

More in The Investment & Markets Channel

Issue 52 - 3D printing a data center

IBM to buy infrastructure management software vendor HashiCorp for $6.4bn

Episode Will India become the driving force of data centers in APAC?

- Blackstone Real Estate

- QTS Data Centers

- QTS Realty Trust

- Blackstone Infrastructure Partners

You are using an outdated browser. Please upgrade your browser to improve your experience.

Blackstone Return on Investment 2010-2024 | BX

- Revenue & Profit

- Assets & Liabilities

- Price Ratios

- Other Ratios

- Other Metrics

- Current Ratio

- Quick Ratio

- Debt/Equity Ratio

- Return Tang Equity

| Blackstone ROI - Return on Investment Historical Data | |||

|---|---|---|---|

| Date | TTM Net Income | LT Investments & Debt | Return on Investment |

| 2024-06-30 | $4.57B | $28.47B | 15.96% |

| 2024-03-31 | $4.75B | $28.28B | 16.38% |

| 2023-12-31 | $3.04B | $28.20B | 10.40% |

| 2023-09-30 | $3.33B | $29.57B | 11.19% |

| 2023-06-30 | $2.26B | $29.78B | 7.71% |

| 2023-03-31 | $0.81B | $29.40B | 2.76% |

| 2022-12-31 | $3.55B | $30.32B | 11.91% |

| 2022-09-30 | $6.18B | $27.97B | 20.90% |

| 2022-06-30 | $9.65B | $29.58B | 32.54% |

| 2022-03-31 | $12.78B | $31.21B | 45.18% |

| 2021-12-31 | $13.10B | $29.44B | 50.22% |

| 2021-09-30 | $11.85B | $28.38B | 49.83% |

| 2021-06-30 | $9.98B | $24.13B | 46.51% |

| 2021-03-31 | $8.31B | $22.39B | 39.06% |

| 2020-12-31 | $2.62B | $20.25B | 12.38% |

| 2020-09-30 | $1.58B | $19.09B | 6.98% |

| 2020-06-30 | $0.67B | $23.35B | 2.75% |

| 2020-03-31 | $-0.05B | $22.00B | -0.19% |

| 2019-12-31 | $3.37B | $26.25B | 13.32% |

| 2019-09-30 | $2.41B | $25.97B | 9.74% |

| 2019-06-30 | $2.53B | $24.85B | 10.34% |

| 2019-03-31 | $3.52B | $24.24B | 14.39% |

| 2018-12-31 | $3.32B | $23.79B | 13.79% |

| 2018-09-30 | $4.23B | $24.92B | 16.74% |

| 2018-06-30 | $4.15B | $24.86B | 16.27% |

| 2018-03-31 | $3.19B | $22.77B | 12.56% |

| 2017-12-31 | $3.39B | $28.45B | 13.37% |

| 2017-09-30 | $3.22B | $25.92B | 13.67% |

| 2017-06-30 | $3.05B | $24.32B | 13.89% |

| 2017-03-31 | $2.88B | $22.81B | 13.98% |

| 2016-12-31 | $2.20B | $21.27B | 11.32% |

| 2016-09-30 | $1.79B | $19.47B | 9.63% |

| 2016-06-30 | $0.67B | $18.74B | 3.64% |

| 2016-03-31 | $0.50B | $18.14B | 2.69% |

| 2015-12-31 | $1.56B | $18.21B | 7.68% |

| 2015-09-30 | $2.41B | $18.69B | 11.13% |

| 2015-06-30 | $3.50B | $19.59B | 15.58% |

| 2015-03-31 | $4.36B | $24.60B | 18.78% |

| 2014-12-31 | $3.63B | $23.85B | 15.94% |

| 2014-09-30 | $3.81B | $21.88B | 16.85% |

| 2014-06-30 | $3.62B | $22.56B | 16.10% |

| 2014-03-31 | $2.97B | $22.80B | 13.42% |

| 2013-12-31 | $2.75B | $23.21B | 12.54% |

| 2013-09-30 | $1.70B | $21.26B | 7.79% |

| 2013-06-30 | $1.64B | $21.39B | 7.43% |

| 2013-03-31 | $1.00B | $21.73B | 4.54% |

| 2012-12-31 | $0.76B | $22.85B | 3.42% |

| 2012-09-30 | $0.47B | $22.34B | 2.27% |

| 2012-06-30 | $-0.57B | $21.23B | -2.90% |

| 2012-03-31 | $-0.13B | $22.29B | -0.70% |

| 2011-12-31 | $-0.14B | $17.13B | -0.81% |

| 2011-09-30 | $-0.09B | $17.47B | -0.53% |

| 2011-06-30 | $0.44B | $17.88B | 2.83% |

| 2011-03-31 | $-0.46B | $15.09B | -3.27% |

| 2010-12-31 | $-1.03B | $14.91B | -7.87% |

| 2010-09-30 | $-1.56B | $13.80B | -14.27% |

| 2010-06-30 | $-1.92B | $12.94B | -21.29% |

| 2010-03-31 | $-1.99B | $10.42B | -27.97% |

| 2009-12-31 | $-2.47B | $6.68B | -42.39% |

| Sector | Industry | Market Cap | Revenue |

|---|---|---|---|

| $96.958B | $8.023B | ||

| Blackstone Inc. is an asset manager of alternative investments and a provider of financial advisory services globally. The company operates its businesses through four segments: Real Estate, Private Equity, Hedge Fund Solutions and Credit & Insurance. They invest across classes on behalf of their investors, including pension funds, insurance companies and individual investors. | |||

| Stock Name | Country | Market Cap | PE Ratio |

|---|---|---|---|

| United States | $180.607B | 19.94 | |

| United States | $85.602B | 41.71 | |

| Japan | $27.557B | 11.07 | |

| Mexico | $21.862B | 0.00 | |

| United States | $18.825B | 9.09 | |

| Canada | $18.015B | 29.20 | |

| United States | $16.314B | 7.09 | |

| United States | $13.117B | 7.68 | |

| United States | $11.832B | 26.66 | |

| Japan | $11.598B | 13.69 | |

| Brazil | $10.990B | 12.99 | |

| United States | $10.620B | 31.69 | |

| United States | $8.815B | 8.72 | |

| United States | $7.037B | 13.86 | |

| United States | $6.670B | 5.58 | |

| United States | $5.944B | 37.31 | |

| United States | $5.667B | 7.46 | |

| United States | $5.562B | 5.64 | |

| United States | $5.402B | 24.69 | |

| $5.230B | 15.02 | ||

| United States | $4.647B | 14.61 | |

| United States | $4.617B | 15.51 | |

| United States | $3.738B | 13.66 | |

| United States | $3.676B | 9.52 | |

| United Kingdom | $3.562B | 0.00 | |

| United States | $3.133B | 17.80 | |

| United States | $2.985B | 32.08 | |

| United States | $2.980B | 0.00 | |

| Brazil | $2.748B | 7.29 | |

| United States | $2.683B | 0.00 | |

| United States | $2.604B | 11.14 | |

| United States | $1.995B | 77.64 | |

| Canada | $1.832B | 4.84 | |

| United States | $1.809B | 71.96 | |

| United States | $1.769B | 7.39 | |

| United States | $1.694B | 37.23 | |

| United States | $1.664B | 0.00 | |

| United Kingdom | $1.660B | 0.00 | |

| China | $1.606B | 0.00 | |

| China | $1.536B | 4.99 | |

| United States | $1.535B | 20.63 | |

| United States | $1.388B | 7.34 | |

| United States | $1.294B | 7.75 | |

| United States | $1.259B | 29.63 | |

| United States | $1.153B | 12.00 | |

| Canada | $1.113B | 0.00 | |

| United States | $0.990B | 13.90 | |

| United States | $0.946B | 0.00 | |

| United States | $0.944B | 0.00 | |

| United States | $0.926B | 235.00 | |

| Singapore | $0.789B | 0.00 | |

| Hong Kong, SAR China | $0.621B | 0.00 | |

| Brazil | $0.615B | 18.16 | |

| China | $0.608B | 0.00 | |

| United States | $0.568B | 4.37 | |

| United States | $0.564B | 0.00 | |

| United States | $0.501B | 8.07 | |

| United States | $0.432B | 16.55 | |

| United States | $0.402B | 0.00 | |

| United States | $0.370B | 11.09 | |

| Canada | $0.364B | 0.00 | |

| United States | $0.329B | 7.36 | |

| United States | $0.324B | 15.83 | |

| United States | $0.304B | 7.78 | |

| United States | $0.292B | 12.60 | |

| United States | $0.267B | 13.30 | |

| United States | $0.263B | 28.28 | |

| United States | $0.253B | 0.00 | |

| United States | $0.248B | 9.26 | |

| United States | $0.220B | 14.79 | |

| China | $0.213B | 1.24 | |

| United States | $0.186B | 8.06 | |

| United States | $0.129B | 5.47 | |

| $0.124B | 0.00 | ||

| United States | $0.118B | 8.94 | |

| United States | $0.111B | 0.00 | |

| Hong Kong, SAR China | $0.109B | 0.00 | |

| United States | $0.104B | 0.00 | |

| United States | $0.088B | 0.00 | |

| United Kingdom | $0.078B | 0.00 | |

| United States | $0.074B | 11.67 | |

| $0.073B | 0.00 | ||

| United States | $0.069B | 5.75 | |

| China | $0.057B | 0.00 | |

| Singapore | $0.049B | 0.00 | |

| United States | $0.043B | 0.00 | |

| Hong Kong, SAR China | $0.041B | 0.00 | |

| United States | $0.035B | 12.70 | |

| United States | $0.034B | 0.00 | |

| United States | $0.026B | 0.00 | |

| United States | $0.025B | 0.00 | |

| United States | $0.021B | 0.00 | |

| United States | $0.020B | 0.00 | |

| China | $0.018B | 0.00 | |

| United States | $0.016B | 50.40 | |

| United States | $0.014B | 0.00 | |

| Hong Kong, SAR China | $0.012B | 0.00 | |

| United States | $0.010B | 0.00 | |

| Hong Kong, SAR China | $0.009B | 0.00 | |

| United States | $0.007B | 0.00 | |

| Hong Kong, SAR China | $0.007B | 0.00 | |

| Singapore | $0.006B | 0.00 | |

| China | $0.006B | 0.00 | |

| Hong Kong, SAR China | $0.006B | 0.00 | |

| China | $0.003B | 0.00 | |

| China | $0.003B | 0.00 | |

| Singapore | $0.001B | 0.00 | |

| $0.000B | 7.65 | ||

| Peru | $0.000B | 11.33 | |

| Hong Kong, SAR China | $0.000B | 0.00 |

Try our new stock screener!

We need your support.

If you use our chart images on your site or blog, we ask that you provide attribution via a "dofollow" link back to this page. We have provided a few examples below that you can copy and paste to your site:

| Link Preview | HTML Code (Click to Copy) |

|---|---|

| "> | |

| "> | |

| "> |

Your image export is now complete. Please check your download folder.

If you use our datasets on your site or blog, we ask that you provide attribution via a "dofollow" link back to this page. We have provided a few examples below that you can copy and paste to your site:

Your data export is now complete. Please check your download folder.

- Sign In / Register

- Update your database profile

- US private equity deal-making data

- News Briefs

- Fintech News

- Healthcare News

- Energy/Power

- Business Services

- Consumer & Retail

- Industrial/Manufacturing

- Women in Private Equity

- Quarterly M&A Deals

- Quarterly M&A Exits

- Leveraged Loans

- Distressed Assets

- Legal Advisor League Table

- Financial Advisor League Tables

- Global events calendar

- Sign-in FAQ

- Suggest a story

Nearly there!

A verification email is on its way to you. Please check your spam or junk folder just in case.

Need help signing in?

Issues with signing in? Click here

Don't have an account? Register now

Blackstone CTO John Stecher: ‘Generative AI can enhance private equity dealmaking’

Blackstone is building an in-house tool that ‘has the potential to intelligently augment our investment process using generative AI.'

Create an account to continue reading

Gain instant access to our expert editorial analysis and in-depth insight., already have an account sign in.

- About PE Hub

- Sign In FAQ

- Privacy Notice

- Cookie Notice

- Terms & Conditions

Register now

Get limited access to our industry news, analysis and data, plus regular email updates

To register, please review and accept our terms and conditions and privacy notice .

Sign in to your account

Email address not recognised.

Don't have an account? Click here to register

Copyright PEI Media

Not for publication, email or dissemination

34 Facts About Balashikha

Written by Rea Cartwright

Modified & Updated: 29 Jul 2024

Reviewed by Jessica Corbett

Balashikha, a vibrant city situated in the Moscow Oblast of Russia, is a captivating blend of rich history, cultural heritage, and modern developments. As you delve into the heart of Balashikha, you'll discover a myriad of fascinating facts that unveil the essence and allure of this dynamic locale. From its intriguing historical landmarks to its flourishing arts and cultural scene, Balashikha beckons visitors to explore its multifaceted identity.

In this article, we'll embark on a journey to unravel 34 captivating facts about Balashikha, offering a comprehensive glimpse into its past, present, and future. Whether you're a history enthusiast, an avid traveler, or simply curious about this enchanting city, these facts will provide an enriching insight into the unique tapestry of Balashikha. Let's venture into the realm of Balashikha and uncover the wonders that await within its embrace.

Key Takeaways:

- Balashikha, a city in Russia, has over 215,000 residents and offers a vibrant cultural scene with museums, theaters, and traditional festivals. It’s a blend of tradition and modernity, making it a captivating destination for exploration and discovery.

- Nestled on the banks of the picturesque Pekhorka River, Balashikha embraces its natural surroundings, providing tranquil retreats like the Balashikha Forest Park and the Botanical Garden. The city’s diverse cultural tapestry invites visitors to savor unique flavors and traditions.

Balashikha is a city in Russia.

Located in the Moscow Oblast, Balashikha is a prominent city in the Moscow metropolitan area, known for its rich history and cultural significance.

The city has a population of over 215,000 people.

Balashikha is home to a diverse community, with a population of over 215,000 residents contributing to the city's vibrant atmosphere.

Balashikha is situated on the Pekhorka River.

The picturesque Pekhorka River flows through the city, adding to the natural beauty and charm of Balashikha.

The city experiences a humid continental climate.

Balashikha's climate is characterized by distinct seasonal changes, with warm summers and cold winters shaping the local environment.

Balashikha is known for its cultural landmarks.

The city boasts a rich cultural heritage, with numerous landmarks and attractions that reflect its historical and artistic significance.

The Balashikha Museum of History and Art is a popular cultural institution.

This renowned museum showcases the city's history and artistic achievements, offering visitors a captivating journey through Balashikha's past and present.

The city has a strong industrial presence.

Balashikha is home to various industries, contributing to the economic vitality and development of the region.

Balashikha is in close proximity to Moscow.

The city's strategic location near the Russian capital provides residents with convenient access to the cultural and economic opportunities offered by Moscow.

The Balashikha Arena is a prominent sports and entertainment venue.

This modern arena hosts a wide range of events, including sports competitions, concerts, and cultural performances, enriching the city's entertainment scene.

Balashikha has a rich tradition of folk music and dance.

The city's cultural heritage is celebrated through vibrant folk music and traditional dance performances , showcasing the local artistic talent.

The Balashikha Forest Park offers a tranquil natural retreat.

Residents and visitors can enjoy the serene beauty of the Balashikha Forest Park, a peaceful escape from the urban bustle.

The city's economy is diverse and dynamic.

Balashikha's economic landscape encompasses various sectors, fostering growth and innovation within the local business community.

Balashikha has a network of educational institutions.

The city is committed to providing quality education, with a network of schools and colleges catering to the academic needs of its residents.

The Balashikha Central Market is a bustling hub of commerce.

This vibrant market showcases local produce, crafts, and goods, serving as a focal point for economic activity and community interaction.

Balashikha is known for its traditional cuisine.

The city's culinary traditions reflect a blend of flavors and recipes unique to Balashikha, offering a delightful culinary experience for food enthusiasts.

The Balashikha Drama Theater is a cultural gem.

The theater enriches the city's cultural scene with captivating performances, showcasing the talent and creativity of local and international artists.

Balashikha has a strong sense of community spirit.

The city's residents are known for their warm hospitality and strong community bonds, creating a welcoming and inclusive environment.

The Balashikha Music School nurtures young talent.

Aspiring musicians receive quality training at the music school, contributing to the city's vibrant music culture and artistic legacy.

Balashikha celebrates traditional festivals and events.

The city's calendar is filled with colorful festivals and events that highlight its cultural diversity and heritage, attracting visitors from near and far.

The Balashikha History and Architecture Museum preserves the city's legacy.

This esteemed museum showcases the architectural heritage and historical legacy of Balashikha, offering valuable insights into the city's evolution over time.

Balashikha is a hub for creative arts and crafts.

Artisans and crafters contribute to the city's creative tapestry, producing unique works of art that reflect Balashikha's artistic identity.

The city has a strong tradition of winter sports.

Balashikha's winter sports enthusiasts enjoy a range of activities, from ice skating to skiing, embracing the winter season with enthusiasm and energy.

Balashikha's architectural landmarks are a testament to its history.

The city's architectural marvels stand as a testament to its rich history, with iconic buildings and structures shaping its urban landscape.

The Balashikha Youth Theater fosters young talent.

Aspiring actors and performers find a platform for artistic expression at the youth theater, contributing to the city's vibrant cultural scene.

Balashikha's public parks offer recreational spaces for residents.

The city's well-maintained parks provide residents with inviting spaces for leisure, relaxation, and outdoor activities.

The Balashikha Philharmonic Society promotes musical excellence.

Musical enthusiasts can indulge in captivating performances at the philharmonic society, where talented musicians showcase their artistry.

Balashikha's local businesses contribute to its economic vitality.

The entrepreneurial spirit thrives in Balashikha, with local businesses playing a significant role in driving the city's economic growth and prosperity.

The Balashikha City History Museum chronicles the city's past.

Visitors can explore the city's historical narrative at the history museum, delving into the events and milestones that have shaped Balashikha's identity.

Balashikha's cultural diversity is reflected in its cuisine.

The city's culinary landscape mirrors its cultural diversity, offering a delightful array of flavors and culinary traditions for residents and visitors to savor.

The Balashikha Puppet Theater captivates audiences of all ages.

Young and old alike are enchanted by the puppet theater's enchanting performances, adding a touch of magic to the city's cultural offerings.

Balashikha's natural surroundings inspire artistic expression.

Artists and creatives draw inspiration from the city's natural beauty, infusing their works with the essence of Balashikha's scenic landscapes.

The Balashikha City Library is a treasure trove of knowledge.

Enthusiastic readers and scholars find a wealth of literary resources at the city library, fostering a love for learning and intellectual exploration.

Balashikha's vibrant street markets showcase local craftsmanship.

The city's street markets buzz with activity, offering an eclectic mix of handmade crafts and artisanal products that reflect Balashikha's creative spirit.

The Balashikha Botanical Garden is a haven of tranquility.

Nature enthusiasts can immerse themselves in the beauty of the botanical garden, where diverse plant species create a serene and enchanting environment.

Balashikha, a city brimming with cultural vibrancy and historical significance, offers a tapestry of experiences for residents and visitors alike. From its rich artistic heritage to its thriving economic landscape, Balashikha embodies a harmonious blend of tradition and modernity. With a population of over 215,000 people, the city exudes a strong sense of community spirit, fostering warm hospitality and inclusive camaraderie. Nestled on the banks of the picturesque Pekhorka River, Balashikha embraces its natural surroundings, providing tranquil retreats such as the Balashikha Forest Park and the Botanical Garden. The city's cultural scene thrives with institutions like the Balashikha Museum of History and Art, the Drama Theater, and the Philharmonic Society, showcasing the talent and creativity of local artists. Balashikha's culinary delights, traditional festivals, and vibrant street markets reflect its diverse cultural tapestry, inviting visitors to savor the flavors and traditions unique to the city. As a hub for education, creativity, and economic dynamism, Balashikha continues to evolve while preserving its architectural landmarks and historical legacy, making it a captivating destination for exploration and discovery.

In conclusion, Balashikha is a city of rich history, vibrant culture, and breathtaking natural beauty. From its fascinating historical landmarks to its modern amenities, Balashikha offers a diverse range of experiences for visitors and residents alike. Whether you're exploring the city's architectural marvels, indulging in its culinary delights, or immersing yourself in its artistic heritage, Balashikha has something to captivate every soul. With its strategic location near Moscow and an array of recreational opportunities, Balashikha stands as a testament to the harmonious blend of tradition and progress. This city is a hidden gem waiting to be discovered, and its allure is bound to leave an indelible mark on anyone who has the pleasure of experiencing it.

What are some must-visit attractions in Balashikha? Balashikha boasts several must-visit attractions, including the iconic Balashikha Arena, the serene Pechorka Park, and the historic Church of the Resurrection.

What are the best times of the year to visit Balashikha? The best times to visit Balashikha are during the spring and summer months when the weather is pleasant, and outdoor activities and festivals are in full swing.

Balashikha's fascinating history, vibrant culture, and modern developments make it a city worth exploring. Uncover more intriguing facts about other cities in the Moscow Oblast, such as the captivating Kolomna . Dive into the unique stories of Russian cities like Orenburg, each offering its own distinctive charm and character.

Was this page helpful?

Our commitment to delivering trustworthy and engaging content is at the heart of what we do. Each fact on our site is contributed by real users like you, bringing a wealth of diverse insights and information. To ensure the highest standards of accuracy and reliability, our dedicated editors meticulously review each submission. This process guarantees that the facts we share are not only fascinating but also credible. Trust in our commitment to quality and authenticity as you explore and learn with us.

Share this Fact:

MOSCOW - RUSSIA

Ewf b.v east west forwarding.

Edelveis, Right Entrance, 2nd Floor Davidkovskaja, 121352 Moscow, Russia

- Phone: +7 495 938-99-66

- Mobile: +7 495-997-0977

- Fax: +7 495 938-99-67

- email: [email protected]

- web: www.eastwestforwarding.com

Company Profile

- LIST WITH US

To: EWF B.V EAST WEST FORWARDING

Enter the security code:

+7 495 938-99-67

+7 495-997-0977

+7 495 938-99-66

Directory of Freight Forwarders, Cargo Agents, Shipping Companies, Air, Ocean, Land, Logistics and Transportation Brokers

- Institutional Investors

- Financial Advisors & Family Offices

Private Wealth Solutions

Financial Advisors, visit our dedicated website to learn how you can partner with Blackstone.

- Private Equity

- Real Estate

- Credit & Insurance

- Blackstone Multi-Asset Investing

- Strategic Partners

- Tactical Opportunities

- Infrastructure

- Life Sciences

- Blackstone Growth

- Blackstone Energy Transition Partners

- Institutional Clients

- Individual Investors & Financial Advisors

- Technology & Innovations

- Portfolio Operations

- Diversity, Equity & Inclusion

- Blackstone Career Pathways

- Blackstone LaunchPad

- Shareholders

- Press Releases

- In the News

- BX Highlights

- Portfolio Spotlight

- Market Views

- Portfolio Insights

Pattern Recognition: Insights from the World’s Leading Alternative Asset Manager

Building Sustainable Businesses

Our mission at Blackstone is to fulfill our fiduciary duty by creating long-term value for our investors. We aim to do this by strengthening the more than 230 companies, ~12,500 real estate assets and other investments in our portfolio, equipping them to thrive amidst a changing global economy.

OUR APPROACh

Reinforcing strong governance, a foundation of resilient companies, investing in the energy transition and driving value-accretive emissions reduction across our portfolio, building stronger workplaces by expanding talent pools, view our 2023 building sustainable businesses update, view our esg policy, view our 2023 climate-related financial disclosures report, corporate approach, within blackstone, we support our operations and business activities with value-enhancing governance policies, programs and systems., building stronger workplaces, corporate sustainability, blackstone charitable foundation, practicing good governance.

Our integrated ESG team operates through a hub and spoke model that incorporates dedicated coverage at the firm level, within our corporate groups and at individual business units. Blackstone is a signatory to PRI (Principles for Responsible Investment) as of July 2021 and is a supporter of TCFD (Taskforce on Climate-related Financial Disclosures) as of October 2021.

Developing and Advancing Talent

We believe that by focusing on recruiting, talent development, community and inclusion and accountability, we will create an environment that drives retention and advancement opportunities for our employees. We are focused on building a broad pipeline of talent for the next generation of leaders at Blackstone and throughout the financial services industry. We’re committed to the engagement, development and retention of our workforce through tailored skill development opportunities.

Our Corporate Carbon Footprint

Throughout our global offices, we seek opportunities to improve energy efficiency and environmental performance. Our 2023 greenhouse gas (GHG) emissions across our corporate operations are detailed in Blackstone’s 2023 Climate-related Financial Disclosures Report.

Closing the Opportunity Gap

Blackstone LaunchPad, the signature program of the Blackstone Charitable Foundation, seeks to close the opportunity gap by equipping college and university students with the entrepreneurial skills they need to build lasting careers. Blackstone employees are highly engaged in giving back, with nearly 90% of employees participating in annual firm-sponsored charitable activities in 2023.

“We provide capital to help our portfolio companies grow and improve performance. In doing so, we seek to generate lasting value for our investors.”

President and Chief Operating Officer

across our portfolio

We believe our efforts reflect what are simply good business practices that support competitiveness and enable growth, ultimately building stronger businesses., blackstone decarbonization accelerator, blackstone career pathways, veterans hiring programs, investing in the energy transition and driving value-accretive emissions reduction.

We believe we can strengthen and create value at companies and real estate assets in our portfolio by, among other levers, helping them reduce energy costs and emissions. We engage select companies and assets through our Emissions Reduction Program, carbon accounting and our recently launched Decarbonization Accelerator, which collectively support a wide range of decarbonization activities. We also continue to invest in energy transition and climate solution macro-trends across our business.

Accessing and Advancing Untapped Talent

Through Blackstone Career Pathways™, we aim to broaden the high-quality talent networks from which our portfolio companies recruit, develop and advance talent. We believe these efforts position our companies to be better able to generate lasting value for our investors.

Supporting Veterans

Through the Veterans Hiring Initiative, more than 100,000 veterans, veteran spouses and caregivers have been hired across our portfolio companies since 2013. 1

Industry Engagement

We engage with several organizations to help inform our approach*..

Note: All figures as of September 30, 2023, unless otherwise indicated. 1. As of July 2021. While Blackstone believes ESG factors can enhance long-term value, Blackstone does not pursue an ESG-based investment strategy or limit its investments to those that meet specific ESG criteria or standards (except with respect to products or strategies that are explicitly designated as doing so in their offering documents or other applicable governing documents). Any such considerations do not qualify Blackstone’s objectives to maximize risk-adjusted returns. Pursuant to Section 44475.2 of Division 26 of the California Health and Safety Code (AB 1305), please see our most recent Climate-related Financial Disclosures report aligned with TCFD recommendations for more details on our emissions reduction program and related initiatives. *All rights reserved. All rights to the trademarks and/ or logos presented herein belong to their respective owners and Blackstone’s use hereof does not imply an affiliation with, or endorsement by, the owners of these logos.

Welcome to Blackstone

Portions of this site are directed only to persons in certain jurisdictions. By selecting the relevant option, you certify that it accurately reflects your residency.

For office-specific contact information, please visit our offices page . Switchboard: +1 (212) 583-5000

Media Contacts

For press inquiries, contact [email protected] .

To view recent press releases, click here .

Stay up-to-date

To receive email alerts from Blackstone, sign up below.

By submitting this request, you consent to receive email from Blackstone. For information on our privacy practices see our Privacy Policy .

Connect with our dedicated team

Our dedicated team works directly with private wealth managers, family offices and financial advisors to help their clients access alternative solutions.

Individual Investors

Please contact your financial advisor to learn more.

Financial Professional Inquiries

[email protected] +1 (212) 583-5200

NCR: The Blackstone Legacy And What's Ahead

- Blackstone was brought in by NCR in December 2015 as an experienced technology investor to add value to and accelerate NCR's strategic transformation to an integrated software and services company.

- Exit from its investment in 2019 was profitable for Blackstone. NCR's transformation continues with acquisition of Cardtronics, but appears to still be very much a work in progress.

- NCR management reports Non-GAAP diluted EPS on an adjusted EBITDA basis.

- NCR Non-GAAP diluted EPS is considered a useful tool by NCR management but excludes significant expenses of relevance to common stockholders.

- Current and prospective NCR common stockholders need to look beyond the company's headline Non-GAAP EPS measures for something appropriate for assessing the fair value of NCR.

Philip Openshaw/iStock Editorial via Getty Images

Image: An NCR ATM cash machine on a wall in Leeds city center

Investment Thesis: NCR Incorporated

Blackstone has exited its investment in NCR (NCR) and new management coming on board in 2018 have had time to settle in and put their own stamp on the business. I find changes to segment organization and financial presentations have resulted in significant reductions in disclosures of information relevant to common stockholders. My review of NCR Corporation's financial statements leads me to conclude the construct of NCR's non-GAAP diluted EPS results in significant overstatement of EPS due to exclusion of regularly recurring costs such as interest expense and depreciation and amortization. While NCR's reported TTM non-GAAP P/E ratio of 15.42 might seem reasonable, inclusion of interest expense in non-GAAP EPS calculation would result in a doubling of P/E multiple to ~31.0. Including normal depreciation and amortization would increase the P/E ratio to ~58.0. Inclusion of both these presently omitted expenses would result in non-GAAP earnings converting to losses. I do not see value in NCR shares at the current share price. The company has recently acquired Cardtronics plc. I will be interested to maintain a watch on NCR's continuing transformation to see if it can achieve a boost in earnings with all relevant costs and expenses included in determining non-GAAP results. Below, I provide a wrap up on the Blackstone period, followed by additional detail on my concerns with current NCR financial reporting.

NCR: The Blackstone Legacy

I previously analyzed NCR Corporation in my July 12, 2019, article, " NCR: The Blackstone Opportunity Updated ," with the share price at $30.91.

My thesis at that time was Blackstone were likely to engineer an exit of the balance of their investment in NCR at a premium price, as happened with their partial exit in 2017. Savvy investors might be best to take advantage of any increase in share price and follow Blackstone out the door. Blackstone exited soon after on September 20, 2019, with details disclosed in an SEC 13D/A filing , including following excerpts,

The Issuer repurchased 237,672.8 shares of the Preferred Stock held by the Blackstone Purchasers (the “Repurchased Shares”) for an aggregate purchase price of $302 million in a privately negotiated transaction pursuant to a Stock Repurchase and Conversion Agreement dated as of September 18, 2019, among the Issuer and the Blackstone Purchasers (the “Stock Repurchase Agreement”). The Stock Repurchase Agreement contains customary representations, warranties and covenants. The Blackstone Purchasers sold the balance of the Converted Shares held by them (9,129,966 shares) in an underwritten block trade in the open market (the “Block Trade”) at a purchase price to the public per share of $32.75 pursuant to an Underwriting Agreement dated as of September 18, 2019, among the Issuer, Goldman Sachs & Co. LLC and Wells Fargo Securities, LLC (the “Underwriters”), and the Blackstone Purchasers (the “Underwriting Agreement”), with a settlement date of September 20, 2019

The outcome of these transactions was favorable for Blackstone, with NCR paying ~$38 per share to Blackstone for the equivalent of 7.9 million common stock shares and NCR facilitating the sale by Blackstone of a further 2.2 million common stock shares at ~$32.24 per share on market. For other common stockholders their only avenue for exit at that time was on the open market.

Summing up the Blackstone legacy, based on statistics at December 2015, when Blackstone came on board, and statistics at December 2019 following Blackstone's exit.

- Total revenue average growth of 2.1% per year from $6,373 million in 2015 to $6,915 million in 2019.

- ATM revenue average growth of 1.6% per year from $1,183 million in 2015 to $1,263 million in 2019.

- Cumulative GAAP earnings 2016 to 2019 $586 million.

- Cumulative reported non-GAAP earnings 2016 to 2019 $1,603 million.

- Dividends paid 2016 to 2019 - nil.

- Increase of $384 million in common stockholders' equity to $1,104 million.

- Increase of $123 million in net debt to $3,050 million.

- Reduction in net debt as a percentage of net debt plus equity from 80.3% to 73.4%

- Increase of 3.1 million in outstanding shares to 127.7 million.

- Share price at end December 2015 $24.46, share price at end December 2019 $35.16. Average yearly share price growth 9.5% (equivalent to 9.5% rate of return).

- Per SEC filing, following appointment as CEO of NCR in April 2018 , Mr Michael Hayford said,

The company has undergone a successful transformation, and is today a leader in technology solutions for financial services, retail and hospitality markets.

NCR Corporation: A Business Undergoing Continuing Transformation

Regardless of the success or otherwise of transformation at the time of appointment of the present CEO in 2018, it is clear NCR is still undergoing significant transformation. Here, I have to be critical of the company's financial reporting. It is confusing, it is not consistent, and it does not provide accountability for stewardship of the common stockholders' financial interests. Let me explain. Following appointment as CEO in April 2018, the CEO introduced a new reporting format effective January 1, 2019 as per FY 2019 10-K filing ,

As of January 1, 2019, NCR began management on an industry basis, changing from the previous model of management on a solution basis. As a result, we categorize our operations into the following segments: Banking, Retail, Hospitality and Other.

The reporting for 2019 showed restated figures on the new basis for 2018 only, so comparability to earlier years is lost. But it gets worse. Gross margin by segment is no longer disclosed, nor the detail of any non-GAAP adjustments in arriving at gross margin. Effective 2021 reporting, operating income by segment is no longer disclosed, nor the detail of any non-GAAP adjustments in arriving at operating income. Instead, a different construct, "Adjusted EBITDA", is provided by segment. Here is the announcement of the change and the definition from Q3 2021 10-Q ,

Management evaluates the performance of the segments based on revenue and adjusted EBITDA. The Company previously evaluated the performance of the segments based on segment operating income. Adjusted EBITDA is defined as GAAP net income (loss) from continuing operations attributable to NCR plus interest expense, net; plus income tax expense (benefit); plus depreciation and amortization; plus stock-based compensation expense; plus other income (expense); plus pension mark-to-market adjustments, pension settlements, pension curtailments and pension special termination benefits and other special items, including amortization of acquisition-related intangibles, restructuring charges, among others. The special items are considered non-operational so are excluded from the adjusted EBITDA metric utilized by our chief operating decision maker in evaluating segment performance and are separately delineated to reconcile back to total reported GAAP net income (loss) from operations attributable to NCR.

There are two issues I have here.

- Firstly, once again, management have changed the basis of segment reporting, but have only provided comparative figures by segment for 2020. The 2020 year was distorted and depressed by impact of COVID-19 so is not a good basis for judging performance in 2021 and beyond.

- Secondly, adjusted EBITDA is not just being used by management to judge operating performance, it's being used as the basis for calculating non-GAAP diluted EPS. I wonder how many investors looking at the current TTM non-GAAP P/E ratio of 15.42 (current share price $37.16 divided by TTM non-GAAP EPS $2.41) believe this to be a relatively low P/E ratio. Many companies adjust EPS for items affecting comparability between periods. But they do not adjust EPS for regularly recurring expenses such as interest on borrowings, depreciation and income tax expense. It's estimated inclusion of interest expense net of tax in the calculation would reduce non-GAAP EPS from $2.41 to $1.20, doubling the P/E ratio to ~31.0. Inclusion of depreciation and amortization net of tax in the calculation is estimated to reduce non-GAAP EPS from $2.41 to ~$0.64, increasing the P/E ratio to ~58.0. Inclusion of both would turn the non-GAAP EPS into a loss per share.

NCR: Summary and conclusions

I do not have an issue with NCR management using an adjusted EBITDA for measuring internal operating performance. I do have an issue with any apparent abdication of responsibility for overall financial performance of the company. I believe publishing a non-GAAP diluted EPS figure that fails to take into account interest expense and other regularly recurring expenses tends to distort financial measures such as P/E ratios and to overstate regularly recurring earnings or understate losses. I do not consider NCR shares an attractive investment option at current share price based on any assessment using more realistically calculated earnings per share.

Dividend Growth Income+ Club - Register today for your Free Trial.

Click Triple Treat Offer (1) Your Free 2 Week Trial; (2) 20% Discount New Members; (3) Bespoke reviews for tickers of interest to subscribers.

This article was written by

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. I do not recommend that anyone act upon any investment information without first consulting an investment advisor and/or a tax advisor as to the suitability of such investments for their specific situation. Neither information nor any opinion expressed in this article constitutes a solicitation, an offer, or a recommendation to buy, sell, or dispose of any investment, or to provide any investment advice or service. An opinion in this article can change at any time without notice.

Seeking Alpha's Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Recommended For You

About vyx stock.

| Symbol | Last Price | % Chg |

|---|

More on VYX

Related stocks.

| Symbol | Last Price | % Chg |

|---|---|---|

| VYX | - | - |

Trending Analysis

Trending news.

- Today's news

- Reviews and deals

- Climate change