UNIVERSITY OF ALLAHABAD, PRAYAGRAJ-211002

The Indian Journal of Economics, a peer reviewed/refereed journal, was established by Prof. H. Stanley Jevons, First Head of the Department of Economics, University of Allahabad. The first Issue of the Journal appeared in January, 1916.

Since 1949 the Indian Journal of Economics disassociated itself with the Indian Economic Association but has continued with its uninterrupted publication till date, and has wide national and international circulations. During the past 100 years, the Journal has succeeded in developing many debates on various aspects of Economic Theory and Policy.

The Journal is published with the three-fold objectives of providing a medium for the publication of articles on economic problems by authors of academic standing or authoritative positions, furnishing a convenient and compact vehicle for publication of original investigations and disseminating information about the economic activities of India and other countries. Its scope has been generally extended since then so as to cover every branch of economic science.

The journal follows double-blind peer-review system for ensuring the quality of papers published.

The articles and findings received for publication are regularly reviewed by experts before being accepted for publication. The Authors of accepted Papers will be supplied, one copy of the issue number concerned, free of cost. The Journal also publishes Book Reviews. The Indian Journal of Economics is Registered with the Registrar, News Papers of India (Regd. No. RN.28648/75) and its ISSN is 0019-5170.

UGC approved list of Journals - No. 20761 - ISSN No. 0019-5170

UGC - CARE Listed

ABDC Category C

To view details

Papers for consideration of Publication be sent by

Email - to

|  The 1991 Reforms, Indian Economic Growth, and Social ProgressThis paper analyzes the effects of the reforms initiated in India following the balance of payments (BOP) crisis of 1991 on economic performance. We do not find persuasive the contention of many analysts that growth accelerated after the mid-1980s when reforms were initiated. Nor does statistical analysis support the contention that reforms in the mid-1980s resulted in a growth acceleration. We show that there is an accelerating rate of growth of GDP after the mid 1970s and it is difficult to relate this gradual acceleration to specific policy changes. The changed policies in the 1980s did not mean a basic change in the policy framework. Furthermore, since corporate investment as a share of GDP did not increase in the 1980s it is difficult to identify the mechanism by which the more pro-business policies of the government were translated to higher growth. We also find that the differences with East Asia and particularly China depend on the basis of the comparison. We compare changes in performance since the reforms, which started in China in 1979 and in India in 1991. Such a comparison shows more similarities than differences. We finally examine social progress. We find that South Asia lags behind other regions in making progress towards the Millennium Development Goals (MDGs) and India lags behind other South Asian countries. The responsiveness of the improvement in the MDGs to increases in per capita income is usually low in Asia and particularly in India. This paper forms part of the research on a project on China and the BRICs conducted under support from the Ontario Research Fund. We are grateful to a seminar group at Western Ontario for comments. The views expressed herein are those of the authors and do not necessarily reflect the views of the National Bureau of Economic Research. MARC RIS BibTeΧ Download Citation Data Published VersionsMANMOHAN AGARWAL and JOHN WHALLEY (2015) The 1991 Reforms, Indian Economic Growth, and Social Progress. World Scientific Reference on Asia and the World Economy: pp. 3-22. More from NBERIn addition to working papers , the NBER disseminates affiliates’ latest findings through a range of free periodicals — the NBER Reporter , the NBER Digest , the Bulletin on Retirement and Disability , the Bulletin on Health , and the Bulletin on Entrepreneurship — as well as online conference reports , video lectures , and interviews .  The Society for Economics Research in India (SERI) promotes research collaboration, intellectual exchange and critique among economists in India.  Conferences Working PapersThe Official Journal of the Pan-Pacific Association of Input-Output Studies (PAPAIOS) - Open access

- Published: 09 May 2020

Tax structure and economic growth: a study of selected Indian states- Yadawananda Neog ORCID: orcid.org/0000-0002-3578-0460 1 &

- Achal Kumar Gaur 1

Journal of Economic Structures volume 9 , Article number: 38 ( 2020 ) Cite this article 50k Accesses 27 Citations 3 Altmetric Metrics details The present study examines the long-run and short-run relationship between tax structure and state-level growth performance in India for the period 1991–2016. The analysis in this paper is based on the model of Acosta-Ormaechea and Yoo ( 2012 ), and for the verification of the relationship between taxation and economic growth the panel regression method is used. With the use of 14 Indian states data, Panel Pool mean group estimation indicates that income tax and commodity–service tax have negative effects whilst property and capital transaction tax have a significant positive effect on state economic growth. This study finds ‘U’ shape relationship between tax structure and growth performance. Based on the analysis, we conclude that for faster growth of Indian states, policymakers should give more focus on property taxes along with the reduction in income taxes. 1 IntroductionThe study on the potential association between tax structure and growth performance has gathered a great deal of attention from policymakers, academicians and regulatory circles for several reasons. First, the developing and emerging economies require a large volume of tax revenues for the smooth and efficient functioning of the state at both the national and sub-national levels. Globalization has laid down the foundation for Goods and Service Tax (GST) in many developing countries (Mcnabb 2018 ). Due to competition, developing countries are also facing the difficulties to maintain existing tax revenues (Bird and Zolt 2011 ). Second, tax collection and structure of it create distortionary impacts in the economy through tax burden. Thus, the positive and negative impact of tax made the ‘tax–growth’ relationship more complex and the structure of taxation has a definite role in the development process of an economy. In a budget constraint economy like India, investigation of tax–growth relationship enables us to formulate the suitable policy measure for the more inclusive and equitable growth process. The budget crisis is usually resolved through the cut-down of public spending or/and an increase in tax revenues (Macek 2014 ). Rapid reduction in spending or increase in taxes is harmful to long-run growth performance. Thus, the concern of the government lies with the problem of fiscal consolidation with sustainable growth performance where tax policies are vital. Empirical evidence on the impact of tax structure on growth performance is not conclusive. India has adopted the Goods and Service Tax (GST) policy in 2017 intending to raise indirect tax collections and transform the indirect tax structure into a single market to avoid tax evasions and double taxation. GST is regarded as one of the major tax policy changes in independent India and economists are an optimist about its impact on revenue generations and growth performance. But this policy is not the only policy that shaped in independent India; other major policy changes also take place after independence. Footnote 1 Tax Reform Committee (TRC) report of 1991 regarded one of the productive and structured policy recommendations in the recent decade. At the state level, sales tax reform in the form of Value Added Tax (VAT) in 2005 becomes a fruitful policy initiative. However, the tax collections in both national and sub-national level are still low as compared to the international standards. Changes in tax policy also change in the tax structure in the economy and India witnessed these changes at both levels of governments. Recent studies proved that the changes in tax structure have decisive implication in the growth performance through work–leisure behaviour, investment decisions and overall productivity (Arnold et al. 2011 ; Gemmell et al. 2011 ; Macek 2014 ; Mdanat et al. 2018 ; Durusu-Ciftci 2018 ). In India, very few empirical studies are available which analyse the impact of these changes in tax structure on growth performance and this study will be first to investigate tax–growth nexus in India with the use of state-level data. This analysis primarily concerned with tax structure rather than to tax levels (usually measured as a tax–GDP ratio). The main advantage of tax structure analysis is that it provides revenue-neutral tax policy changes which remove the difficulties related with the question of how aggregate tax revenue changes relates with expenditure changes (Arnold et al. 2011 ). The empirical results from linear panel regression suggest us that property and capital transection tax are positively affecting the state’s growth performance, where commodity and service tax effect negatively. However, the non-linear panel regression indicates that the positive effect is only visible for property taxes at a higher level where the negative effect of commodity and service taxes becomes positive after a threshold point. The effect of income tax is not significant in long run irrespective of panel regression models. The structure of the paper is as follows: Sect. 2 deals with the theoretical framework and empirical literature, followed by a brief description of data and methodology in Sect. 3 . Empirical results and discussion are presented in Sect. 4 and our last Sect. 5 is for conclusions and recommendations. 2 Theoretical framework and empirical literatureGrowth literature very recently acknowledges the role of taxation in the growth process of an economy. Until recently, growth models are more concerned with the steady-state process and exogenous changes. On the theoretical ground, taxation does not have any impact on growth (Myles 2000 ). Development of endogenous growth models creates the space for fiscal policy especially tax policy in determining the growth performance. Barro ( 1990 ), King and Rebello ( 1990 ) and Jones et al. ( 1993 ) were the pioneer in this regard. Tax level and tax structure have an impact on the saving behaviour of the household and investment in human capital. On the other hand, the firm also changes its investment decisions and innovations following tax policies (Johansson et al. 2008 ). These decisions and incentives in the accumulation of physical and human capital create the ‘Growth’ disparities amongst the countries and state economies. A large body of literature available on “Tax-Growth” relationship is mostly dedicated to cross-country settings (Martin and Fardmanesh 1990 ; Karras 1999 ; Myles 2000 ; Tosun and Abizadeh 2005 ; Johansson et al. 2008 ; Vartia et al. 2008 ; Arnold 2011 ; Szarowska 2013; Macek 2014 ; Stoilova 2017 ; Safi et al. 2017 ; Durusu-Ciftci 2018 ) that investigates the effect of tax policy on economic performance. Income and corporation taxes are the major tax instruments for the governments irrespective of the level of developments of a country. The formation of tax structure with these two taxes has many implications in the growth performance. The study made by Arnold et al. ( 2011 ), Macek ( 2014 ) and Dackehag and Hansson ( 2012 ) has explored the negative relation of income and corporation tax with growth performance. Vartia et al. ( 2008 ) find the negative impact of corporation tax for OECD countries. If we consider the average and marginal tax rate, marginal tax is very influential than to average tax rate in investment decisions and labour supply. Empirical studies prove that marginal tax has a negative relation with growth, which indicate raising of marginal tax rate is associated with compromises with growth performance (Padovano and Galli 2001 ; Lee and Gordon 2005 ; Poulson and Kaplani 2008 ). Studies also established that other type of taxes also has a significant impact on growth performance, like consumption tax (Johansson et al. 2008 ; Durusu-Ciftci 2018 ), GST and Payroll (Tosun and Abizadeh 2005 ), property tax (Xing 2011 ), labour tax (Szarowska 2014 ), sales tax (Ojede and Yamarik 2012 ), excise (Reynolds 2006 ), etc. However, looking at the single country’s perspective, we find very little evidence on the same. Stockey and Rebelo ( 1995 ) with the use of the endogenous growth model study the role of tax reforms on U.S. growth performance. They have found that tax reforms have very minor implication with economic outcomes. There are several studies exist for US economy where they empirically try to establish the link between tax and growth. Atems ( 2015 ) finds the spatial spillover effect of income taxes on the growth of 48 contiguous states. On the other hand, Ojede and Yamarik ( 2012 ) have not found any kind of impact of income taxes on growth in these states. Their panel pool mean group estimation indicates that property and sales tax has detrimental consequences in development. With the use of data for the U.S. covering the period of 1912–2006, Barro and Redlick ( 2009 ) find that average marginal income taxes were halting the economic growth. However, they have provided an interesting argument that in wartime, the tax does not have any kind of relation with growth. In search of an answer to the question that whether corporate tax rise destroys jobs in the U.S., Ljungqvist and Smolyansky ( 2016 ) use firm-level data for the period 1970–2010. The main conclusion of the paper is that a rise in corporate tax is not good for employment and income and has very little impact on economic activity. Using the error correction model, Mdanat et al. ( 2018 ) find for Jordan that income tax, corporation tax and personal tax negatively impact the growth. They suggest that irrespective of tax collection, the prime focus of the government should be social justice of the people. Dladla and Khobai ( 2018 ) also find similar results for South Africa where income taxes are coming out to be negative. For the case of Italy, Federici and Parisi ( 2015 ) used the 880 firms’ data and results show that corporation tax is bad for investments with the consideration of both effective average and marginal taxes rates. Looking at the literature, the empirical relationship of tax structure with growth performance is still unclear for India. This study attempts to fill the gap by examining the effect of tax policy on economic performance in an emerging economy such as India at the state level. Second, with the use of panel Pool Mean Group (PMG) estimator which assumes slope homogeneity in the long run and heterogeneity in the short run, we can incorporate the dynamic behaviour of the variables which will be new to tax structure–growth study in India. Third, the tax–growth nexus may show a non-linear relationship due to the threshold effect. We consider this non-linearity in our panel regression model which will be a contribution to the existing literature. 3 Data and methodologyTo study the effect of tax policy on economic performance in India, we employed three models and included each tax instruments in the models separately to avoid the problem of Multicollinearity. Following the works of Arnold et al. ( 2011 ) and Acosta-Ormaechea and Yoo ( 2012 ), the tax structure is measured by the share of individual tax to the total state tax revenues. We investigate the tax–growth relationship with the following equation. Here, Y it is the growth rate of Per capita net state domestic product (NSDP), SGI is the state gross investment as a percentage of state domestic product, TAX is one of the tax shares (Property, Commodity & Services and Income), Tax Burden Footnote 2 is the ratio of total tax revenues to state domestic product and ϵ is the error term. Per the work of Acosta-Ormaechea and Yoo ( 2012 ), this study is more concerned with the impact of tax structure on growth rate rather than level effect. In model 1, we include property tax share, and in model 2 and model 3, we incorporate commodity & service tax and income tax, respectively. By following the approach of Arnold et al. ( 2011 ), we include total tax burden as a control variable which will reduce the biases that may occur from correlation in between tax mix and tax burden. We also included Secondary Enrollment Rate as a proxy variable for human capital in our model, but the inconsistent and insignificant results make us drop the variable from the final estimation model. In search of a possible non-linear relationship, we introduce a separate panel regression by introducing the square of each tax share into the models. If the coefficient of α 3 significant and carries an opposite sign to α 2 , then we can conclude that there is a non-linear relationship exist. In this study, we included 14 Indian states for the period 1991 to 2016 and excluded North-Eastern states due to their relatively small tax revenue collections. Data have been taken from the Centre for Monitoring Indian Economy (CMIE) and Handbook of Statistics on the Indian States, published by Reserve Bank of India. The states that are included in this study are Andhra Pradesh (undivided), Footnote 3 Assam, Gujarat, Haryana, Himachal Pradesh, Jammu & Kashmir, Karnataka, Kerala, Maharashtra, Punjab, Tamil Nadu, Orissa, Rajasthan and West Bengal. All the states are included in model 1 and model 2. For model 3, due to the data availability, we include only seven states Footnote 4 namely Andhra Pradesh, Assam, Gujarat, Karnataka, Kerala, Maharashtra, and West Bengal. The selection of the study period is primarily driven by the argument provided by Rao and Rao ( 2006 ) that after the market-oriented economic reform of 1991, more systematic and long-term goal-oriented tax reforms were initiated in state level for India. The economic reform also brings rapid growth in India and it becomes very interesting to look at the tax–growth nexus after the economic reform. The second restriction related to the use of long data span is the availability of data for each tax head for each of the states under this study. 3.1 Unit rootPool Mean Group (PMG) specification is very fruitful and widely used model to capture the dynamic behaviour of policy variables. This model is very powerful as it can investigate both I (0) and I (1) variables in a single autoregressive distributive lag (ARDL) model setup. A necessary condition in the ARDL model is that the model cannot deal with the I(2) variables. Thus, the investigation of stationarity becomes a compulsion. We used popular panel unit root tests like LLC (Levin et al. 2002 ), the IPS (Im et al. 2003 ), the ADF-Fisher Chi square (Maddala and Wu 1999 ) and PP-Fisher Chi square (Choi 2001 ) in this study. 3.2 Panel PMG modelThe Mean Group (MG) estimator was developed by Pesaran and Smith ( 1995 ) to solve the issue of bias related to heterogeneous slopes in dynamic panels. Traditional panel models like instrumental variables’ estimator of Anderson and Hsiao ( 1981 , 1982 ) and Arellano and Bond ( 1991 ) may produce inconsistent results in a dynamic panel framework (Pesaran et al. 1999 ). MG estimator takes the average value of every cross-section and provides the long-run estimate for ARDL or PMG. On the other hand, Pooled Mean Group (PMG) estimator developed by Pesaran et al. ( 1999 ) assumes slope homogeneity in the long run but heterogeneous slopes in the short run for cross-section units. Dynamic Fixed Effect (DFE) also works like PMG and restricts cointegrating vector to be equal across all panels and restricts the speed of adjustment to be equal. Under these assumptions, PMG is more efficient estimator than to MG and DFE estimator. The prime requirement for PMG estimator is that T should be sufficiently large to N. Panel ARDL or PMG works through maximum likelihood. Our basic PMG begins with the following equation. Here, x it is the vector explanatory variables and y i is the lag dependent variable. X it allows the inclusion of both I (0) and I (1) variables. State fixed effect is captured through μ i . Above equation can be re-parameterized to ARDL format. ɸ i measures the state-specific speed of adjustment and known as Error Correction Term. Β i is the vector of long-run relationships and α ij and θ ij are the vectors of short-run dynamic relationships. Pesaran et al. ( 1999 ) did not provide any statistical test for checking long-run relationship but it can be concluded form sign and magnitude of Error Correction Term (ECT). If it is negative and less than − 2, a long-run relationship can be established. 4 Results and discussionPanel unit root test results from Table 1 suggest that in the case of Model 1 & 2, the Growth rate of Per Capita Net State Domestic Product (PC-NSDP), Property tax and commodity taxes are stationary at level. Gross investment and total tax revenue share to GDP are stationary at the 1st difference in all models and income tax share is also stationary at the same order. 5 PMG model resultsWe have reported MG, PMG and DFE estimation in the Tables 2 and 3 . The Hausman test indicates that the PMG model is the best model for our data than to MG model. Negative and significant error correction terms in all the models show the long-run relationship in between variable. One major issue related to the tax–growth equation is the problem of endogeneity of the variables. As growth in per capita GDP is our dependent variables, there is a possibility that tax collections behave along with business cycles. Therefore, we tested the weak/strong exogeneity of the tax variables through the correlation analysis between business cycles and tax shares. Business cycles have been calculated using the Hodrick-Prescott (HP) Filter. We have found that all the tax instruments are very weakly related to the business cycles movement and thus, we conclude that variables are not truly endogenous. The speed of adjustment in PMG model 1, 2 and 3 are 78.9%, 78.4% and 79.6%, respectively. For the sake of completeness, we have reported MG and DFE Footnote 5 model results also. But we are more concerned with the results of PMG estimator as Hausman test suggested that PMG is a better model than to MG. The sign of the property tax is positive and significant in the long run as well as in the short run. Results are in line with the findings of Acosta-Ormaechea and Yoo ( 2012 ). Property tax generally considered a good revenue source for state and municipal governments for providing economic and social services in the city. This tax is also able to establish cost–benefit linkages and feasible decisions for the citizens. The positive impact of property taxes indicates that the revenue generation and productive utilization of these revenues exceed the distortionary effect in these states. As we expected, the tax burden is negatively associated with growth performance in both long run and short run. The relationship is showing the distortionary effect of the tax collection in the state economy. In all models, gross investment enhancing the growth in per capita SDP in the long run. Signs are readily justified as enlargement of capital formation has a positive impact on output and employment which channelized to the development outcomes (Swan 1956 , Solow 1956 ). Commodity and service taxes are negatively related to the growth in per-capita SDP in the long run as well as in short run and findings are similar to the work of Ojede and Yamarik ( 2012 ). Footnote 6 This tax now comes under the Goods & Services taxes, but in the pre-GST period, commodity and service taxes are reducing growth in per capita NSDP. Commodity taxes are indirect taxes and state own tax revenues mostly come from indirect taxes. As indirect taxes, it has certain disadvantages like inflationary pressure in the economy and regressive to the poor section of the society. Our results also support the same hypothesis that increased commodity tax share is harmful. In India, commodity and service tax includes central sale tax, state excise duty, vehicle tax, goods & passenger tax, electricity duty and entertainment tax. Central sale tax was imposed on interstate trade of commodities which is now transformed to Inter-State GST (IGST). According to Das ( 2017 ), if the IGST rate is high to the Revenue Neutral Rate, it will harm the aggregate demand in the economy through the reduction of disposable income. Heavy vehicle and passenger tax collections are creating an abysmal environment for industrial activities. The tax burden variable is also carrying a negative sign in both long run and short run and magnitude is very similar to model 1. Income tax share has become insignificant and positive in the long run and negative insignificant in the short run. After examining the linear relationships, we extended our analysis to the examination of a non-linear relationship with the use of PMG estimation model. The result from Tables 4 and 5 indicates the existence of a non-linear relationship between tax structure and growth performance for Indian states. The linear coefficient for property taxes has now become negative and the square of it turns out to be positive. Thus, the property taxes show a ‘U’-shaped relationship with states’ growth performance which implies that a rise in property taxes is bad for growth initially and after a threshold point, it becomes growth enhancing. The threshold point for property taxes is 1.88 which indicates that more than 80.77% observation is more than to threshold point. In the case of commodity and service taxes, both the linear and non-linear coefficients are significant with different signs. However, the coefficient magnitudes are abnormally large and this is due to the inclusion of both linear and quadratic terms into the single equation. The small commodity and service taxes are very bad for the state economy, whereas the large amount of it shows a positive relation. The threshold point for this tax is 4.45 which implies that 79.95% observation lies above the threshold. This is a very interesting result as high commodity and service taxes could lead to high inflation in the economy and high inflation regarded as atrocious for growth. Further investigation of these findings is highly recommendable. As like linear panel regression, the income tax shows no relation in our non-linear regression model also. However, the short-run coefficient for income tax is significant and shows a negative relationship. Income tax is considered to be distortionary tax to the economy in the presence of income and substitution effect (Kotlan 2011 ). Income tax mostly impacts the savings of the households and labour supply which is regarded as an engine of growth. 6 Conclusions and recommendationsIn this study, we try to find out the long-run and short-run relationship between different tax structure and economic growth in states of India. Empirical evidence from linear regression suggests that the property tax enhancing growth and commodity & service taxes reduce it. The non-linear regression validates these findings for property taxes where high property taxes are good for growth. In the case of commodity & service taxes, the results become opposite after the threshold point and affecting the growth negatively. Interestingly, we do not find any significant impact of income taxes on growth in both linear and non-linear regressions in the long run. As far as the total tax burden is concerned, negative relation with the growth performance is verified and results are in line with Arnold et al. ( 2011 ). The negative effect of commodity and service taxes in the short run is expected to be neutralized through the implementation of GST in India. Promotion of growth performance at the state level concerning income taxes is also very crucial. Income tax has a direct effect on individuals and their saving and investment behaviour. On the other side, tax revenues should be placed in productive investments. With the spending, the government can promote inclusive growth, equality and efficiency in the economy. The most promising path emerged through this study for long-run growth performance in Indian states is to lower the total tax burden and shifting from income and commodity taxes to property tax for revenue generations. The conclusion may be debatable on various grounds as the studied variables do not take into account institutional quality, administrative efficiency in tax collection, fiscal balance and condition of the states and existence of informal sectors. Future research can be done to incorporate these issues. Availability of data and materialsDataset analysed in this study is available from the corresponding author on reasonable request. One can see the writings of Rao and Rao ( 2006 ) for brief discussion. This is the proxy for total tax burden in the economy with certain limitations. It does not include informal economy and expenditure policies. Telangana state was established in 2014. We merged the data of Andhra Pradesh and Telangana to achieve aggregate data for undivided Andhra Pradesh. Data for Income tax are available for ten states, but inclusion of these states made the model inconsistent due to huge fluctuations in tax revenue collections. Most of the coefficients of PMG and DFE are in similar range and smaller than to MG estimator. This is due to MG estimator only takes the information of each state time series to estimate long-run and short-run coefficients. They use sale tax, where our study takes aggregate revenue for commodity and services. However, inference can be drawn as sale tax and is one of the dominant contributors in total commodity and service tax revenue in India. AbbreviationsNet state domestic product Goods and service tax Foreign direct investments Dynamic fixed effect Auto-regressive distributed lag The organization for economic co-operation and development Anderson TW, Hsiao C (1981) Estimation of dynamic models with error components. J Am Stat Assoc 76(375):598–606 Article Google Scholar Anderson TW, Hsiao C (1982) Formulation and estimation of dynamic models using panel data. J Econom 18(1):47–82 Arellano M, Bond S (1991) Some tests of specification for panel data: monte carlo evidence and an application to employment equations. Rev Econ Stud 58(2):277–297 Arnold JM et al (2011) Tax policy for economic recovery and growth. Econ J 121:59–80. https://doi.org/10.1111/j.1468-0297.2010.02415.x Atems B (2015) Another look at tax policy and state economic growth: the long and short run of it. Econ Lett 127(1):64–67 Barro RJ (1990) Government spending in a simple model of endogenous growth. J Politic Econ Univ Chicago Press 98(5):103–126 Barro RJ, Redlick CJ (2009) Macroeconomic effects from government purchases and taxes, ADB economics working paper series, No. 232 Bird RM, Zolt EM (2011) Dual income taxation: a promising path to tax reform for developing countries. World Dev 39(10):1691–1703 Choi I (2001) Unit root tests for panel data. J Int Money Fin. 20:249–272 Dackehag M, Hansson A (2012) Taxation of income and economic growth : an empirical analysis of 25 rich OECD countries Das S (2017) Some concerns regarding the goods and services tax. Econ Polit Wkly 52(9) Dladla K, Khobai H (2018) The impact of taxation on economic growth in South Africa, MPRA Paper No. 86219, 1–15 Durusu-çiftçi D, Gökmenoğlu KK, Yetkiner H (2018). The heterogeneous impact of taxation on economic development: new insights from a panel cointegration approach. Economic systems. Elsevier BV. https://doi.org/10.1016/j.ecosys.2018.01.001 Federici D, Parisi V (2015) Do corporate taxes reduce investments? Evidence from Italian firm level panel data. Cogent Econ Finance 3:1–14. https://doi.org/10.1080/23322039.2015.1012435 Gemmell N, Kneller R, Sanz I (2011) The timing and persistence of fiscal policy impacts ongrowth: evidence from OECD countries. Econ J 121(550):33–58 Im KS, Pesaran MH, Shin Y (2003) Testing for unit roots in heterogeneous panels. J Econometrics. 115:53–74 Johansson Å et al (2008) Taxation and economic. Growth. https://doi.org/10.1787/241216205486OECD Jones L, Manuelli R, Rossi P (1993) Optimal taxation in models of endogenous growth. J Polit Econ 101(3):485–517 Karras G (1999) Taxes and growth: testing the neoclassical and endogenous growth models. Contemporary Econ Policy. 17(2):177–188 King R, Rebelo S (1990) Public policy and economic growth: developing neoclassical implications. J Polit Econ 98(5):S126-50 Kotlán I, Machová Z, Janíčková L (2011) Vliv zdanění na dlouhodobý ekonomický růst. Politická ekonomie. 5:638–658 Lee Y, Gordon RH (2005) Tax structure and economic growth. J Public Econ 89(5–6):1027–1043. https://doi.org/10.1016/j.jpubeco.2004.07.002 Levin A, Lin CF, Chu CS (2002) Unit root tests in panel data: asymptotic and finite-sample properties. J Econometrics. 108(1):1–24 Ljungqvist A, Smolyansky M (2016). To cut or not to cut? On the impact of corporate taxes on employment and income, Finance and economics discussion series 2016–006. Washington: Board of Governors of the Federal Reserve System, http://dx.doi.org/10.17016/FEDS.2016.006 Macek R (2014) The impact of taxation on economic growth: case study of OECD countries. Rev Econ Perspect. 14(4):309–328. https://doi.org/10.1515/revecp-2015-0002 Maddala GS, Wu S (1999) A comparative study of unit root tests with panel data and a new simple test. Oxford Bull Econ Stat 61:631–652 Martin R, Fardmanesh M (1990) Fiscal variables and growth: a cross-sectional analysis. Public Choice 64:239–251 Mcnabb K (2018) Tax structures and economic growth: new evidence from the government revenue dataset. J Int Dev 30:173–205. https://doi.org/10.1002/jid.3345 Mdanat MF et al (2018) Tax structure and economic growth in Jordan, 1980–2015. EuroMed J Bus 13(1):102–127. https://doi.org/10.1108/EMJB-11-2016-0030 Myles GD (2000) Taxation and economic growth. Fiscal Studies. 21(1):141–168. https://doi.org/10.1016/0264-9993(93)90021-7 Ojede A, Yamarik S (2012) Tax policy and state economic growth : the long-run and short-run of it, Economics Letters. Elsevier BV, 116, No.2, pp. 161–165. https://doi.org/10.1016/j.econlet.2012.02.023 Ormaechea AS, Yoo J (2012) Tax composition and growth: a broad cross-country perspective. IMF Working Papers. https://doi.org/10.5089/9781616355678.001 Padovano F, Galli E (2001) Tax rates and economic growth in the OECD countries (1950–1990). Econ Inq 39(1):44–57 Pesaran MH, Smith RP (1995) Estimating long-run relationships from dynamic heterogeneous panels. J Econometrics. 68:79–113 Pesaran MH, Shin Y, Smith RP (1999) Pooled mean group estimation of dynamic heterogeneous panels. J Am Stat Assoc. 94:621–634 Poulson BW, Kaplani JG (2008) State income taxes and economic growth. Cato J 28(1):53–71 Google Scholar Rao MGR, Rao RK (2006) Trends and issues in tax policy and reform in India. INDIA POLICY FORUM Reynolds S (2006) The impact of increasing excise duties on the economy. Working Paper Series 58069. PROVIDE Project Saafi S, Mohamed MBH, Farhat A (2017) Untangling the causal relationship between tax burden distribution and economic growth in 23 OECD countries: fresh evidence from linear and non-linear Granger causality. Eur J Comp Econ. 14(2):265–301 Solow RM (1956) A contribution to the theory of economic growth. Q J Econ 70(1):65–94 Stoilova D (2017) Tax structure and economic growth: evidence from the European Union. Contaduría y Administración. 62:1041–1057. https://doi.org/10.1016/j.cya.2017.04.006 Stokey NL, Rebelo S (1995) Growth effects of flat-rate taxes. J Polit Econ 103(3):519–550 Swan TW (1956) Economic growth and capital accumulation. Econ Record 32:334–361. https://doi.org/10.1111/j.1475-4932.1956.tb00F434 Szarowska I (2014) Effects of taxation by economic functions on economic growth in the European Union. MPRA Paper No. 59781 Tosun MS, Abizadeh S (2005) Economic growth and tax components: an analysis of tax changes in OECD. Appl Econ 37:2251–2263. https://doi.org/10.1080/00036840500293813 Vartia L (2008) How do taxes affect investment and productivity ? An industry-level analysis of OECD countries. OECD Economics Department Working Papers 656 Xing J (2011) Does tax structure affect economic growth? Empirical evidence from OECD countries, Centre for Business Taxation, WP 11/20 Download references AcknowledgementsAuthors like to acknowledge the anonymous referee for his/her valuable comments. Not applicable. Author informationAuthors and affiliations. Department of Economics, Banaras Hindu University, Varanasi, India Yadawananda Neog & Achal Kumar Gaur You can also search for this author in PubMed Google Scholar ContributionsBoth the authors’ handled the data, analysed and contribute their part to write the manuscript. Both authors read and approved the final manuscript. Corresponding authorCorrespondence to Yadawananda Neog . Ethics declarationsCompeting interests. The authors declare that they have no competing interests. Additional informationPublisher's note. Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations. See Tables 1 , 2 , 3 , 4 and 5 . Rights and permissionsOpen Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/ . Reprints and permissions About this articleCite this article. Neog, Y., Gaur, A.K. Tax structure and economic growth: a study of selected Indian states. Economic Structures 9 , 38 (2020). https://doi.org/10.1186/s40008-020-00215-3 Download citation Received : 26 November 2019 Revised : 16 March 2020 Accepted : 29 April 2020 Published : 09 May 2020 DOI : https://doi.org/10.1186/s40008-020-00215-3 Share this articleAnyone you share the following link with will be able to read this content: Sorry, a shareable link is not currently available for this article. Provided by the Springer Nature SharedIt content-sharing initiative  General principlesRepec services, additional websites using repec. - RePEc help / FAQ

- Getting material into RePEc

- Contributing archives

- RePEc history

Quick links- MPRA : Munich Personal RePEc Archive

- EconPapers | IDEAS : working papers

- EconPapers | IDEAS : articles

- EconPapers | IDEAS : books

- EconPapers | IDEAS : book chapters

- EconPapers | IDEAS : software components

- EconPapers | IDEAS : authors

- EDIRC : Economics institutions

How RePEc operates:Every publisher or provider puts text files describing their publications on their own server. These files follow a simple but rigorous machine-readable syntax. They are then automatically mirrored and made available to the public on the various RePEc websites. Some RePEc services complement these data with additional information such as citations or author details. RePEc is thus a facilitator that organizes the data for others to use. How you can use RePEc as a provider or publisher:Join over 2000 providers and publishers to increase the visibility of your publications. Follow these step-by-step instructions to create your RePEc archive. They show how to quickly set up your RePEc archive on your http, https, or ftp server and describe the syntax of the required metadata for working papers, journal articles, books, chapters, and software. For the complete technical details on the infrastructure and the metadata, you can also read about the Guildford Protocol and ReDIF , the Research Documents Information Format. How you can use RePEc as a reader:You can explore economic literature on two RePEc services. On EconPapers and IDEAS , search and browse, or follow links to author profiles, references, citations, keywords, or classifications. You can get notifications of new material with two other RePEc services, NEP and MyIDEAS . How you can use RePEc as an author:With the RePEc Author Service , you can create a profile of your indexed works. This allows the other RePEc services to link your profile to your works and vice versa. You also get notifications about the visibility of your works and citations newly found by CitEc . And if your publisher does not participate in RePEc, you can upload missing items to MPRA , copyright permitting. How you can use RePEc as an institution:RePEc can help you make your working papers (pre-prints) more visible, track how your researchers publish, and provide metrics to evaluate impact. How you can leverage RePEc data as a researcher:Data assembled by RePEc can be used for many purposes. Examples are academic research, tracking how working papers get published, adding metrics to a website, and evaluating researchers or institutions. We have instructions on how to access the data, including through an API. There is much more that RePEc can do for you. Below is a list of all the RePEc services: | | | Authors in institutions lacking a participating RePEc archive can submit their papers to MPRA and get them included in the RePEc database. |

| | | | Author registration and maintenance of a profile on RePEc. | | | | The complete RePEc database at your disposal. Browse or search it all. | | | | Economics at your fingertips. EconPapers provides access to all of RePEc. Browsing and searching available. |

| | | | Directory of Economics institutions, with links to their members and publications listed on RePEc | | | | | | New Economics Papers is a free email, RSS and Twitter/X notification service for new downloadable working papers from over 90 specific fields. Archives are also available. | | | | Academic family tree for economics. | | | | Detailed download and access statistics for RePEc items and authors. | | | | Citation analysis from items in the RePEc database. | | | Rankings by co-authorship centrality for authors registered in the RePEc Author Service. | | | | Hand-selected bibliography of articles and papers in economics. | | | | Blog aggregator for discussion about economics research. | | Service to annotate RePEc papers in PDF and establish scientific relationships between papers. | --> | | | | An effort to curtail plagiarism of RePEc contents. | - Google Scholar

- Microsoft Academic Search

- OAISter/WORLDCAT

- ResearchGate

Adding bibliographic information to RePEcIf you intend to contribute information about your publications to RePEc, you may read the above documents or use these step-by-step instructions or sample templates . The same instructions apply for commercial publishers or research institutes. RePEc archive maintainers may also make good use of the template syntax and link checker , of tips and tricks and the FAQ . RePEc emerged from the NetEc group , created in 1992, which received support for its WoPEc project between 1996-1999 by the Joint Information Systems Committee (JISC) of the UK Higher Education Funding Councils, as part of its Electronic Libraries Programme (eLib). RePEc was created in June 1997 to decentralize the work done by WoPEc and thus make it independent of grant needs. RePEc is then guaranteed to remain free for all parties. - DOI: 10.62338/ejhy8c59

- Corpus ID: 267639019

A Comparative Study of India and China’s Economic Assistance to Maldives- Published in The Maldives National Journal… 30 November 2023

- Economics, Political Science

- The Maldives National Journal of Research

Related PapersShowing 1 through 3 of 0 Related Papers INCOME INEQUALITY: ECONOMIC SIGNIFICANCE AND RESEARCH CONTRADICTIONS IN THE INDIAN CASE  Discover the world's research - 25+ million members

- 160+ million publication pages

- 2.3+ billion citations

- S. R. Hashim

- Ravi Kanbur

- Kanbur Rhee

- Sadhana Satapathy

- Biswabas Patra

- Rajendra Prasad Patro

- A. W. Coats

- David Ricardo

- Andrew Berg

- Econ Polit Wkly

- DAVID LUDDEN

- Era Dabla-Norris

- Nujin Suphaphiphat

- Evridiki Tsounta

- Handbook Income Distrib

- Facundo Alvaredo

- Recruit researchers

- Join for free

- Login Email Tip: Most researchers use their institutional email address as their ResearchGate login Password Forgot password? Keep me logged in Log in or Continue with Google Welcome back! Please log in. Email · Hint Tip: Most researchers use their institutional email address as their ResearchGate login Password Forgot password? Keep me logged in Log in or Continue with Google No account? Sign up

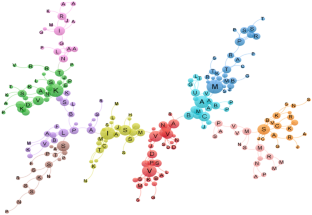

Advertisement  The Structure of Scholarly Publishing: a Case of Economics Research in India- Published: 17 April 2021

- Volume 13 , pages 1801–1818, ( 2022 )

Cite this article - Krishna Muniyoor ORCID: orcid.org/0000-0003-1504-712X 1

489 Accesses Explore all metrics There is a great deal of disparity in the creation and dissemination of scholarly publications across disciplines. The main objective of the study in this article is three-fold: first, to find empirical evidence of publishing regularity in economics journals in India; second, to examine what accounts for author concentration in journals, with a special focus on economics; and third, to understand the nature of scholarly collaboration. For this, authorship data from eight Indian economics journals and the Economic and Political Weekly (EPW), a prestigious periodical encompassing a range of areas in social sciences, were manually obtained. This study contributes to existing literature by substantiating that author concentration is not merely an outcome of the degree of journal specialization. Interestingly, the study shows that a journal with generic readership is likely to form a power-law distribution. The computed measures of social network analysis indicate that collaboration in Indian economics, unlike in world economics, is in a nascent stage, consisting of a large number of isolated authors on the one hand, and some fragmented groups of varied sizes, on the other. This is a preview of subscription content, log in via an institution to check access. Access this articleSubscribe and save. - Get 10 units per month

- Download Article/Chapter or eBook

- 1 Unit = 1 Article or 1 Chapter

- Cancel anytime

Price includes VAT (Russian Federation) Instant access to the full article PDF. Rent this article via DeepDyve Institutional subscriptions  Source: data compiled by the author from EPW. Note: Fig. 1 is drawn using VOSviewer Similar content being viewed by othersThe power law relationship between citation impact and multi-authorship patterns in articles in information science & library science journals, evolution and structure of scientific co-publishing network in korea between 1948–2011.  Publishing Trends in Political Science: How Publishing Houses, Geographical Positions, and International Collaboration Shapes Academic Knowledge ProductionThe government of India established the Indian Council of Social Science Research (ICSSR) in 1968 to support social science research in India. All the authors were given equal weight in case of co-authorship. This criterion applies to all journals except the Indian Journal of Economics . Authorship data compiled from the Indian Journal of Economics starts from 1962. In this paper, the chi-square goodness of fit test is used to test the presence or absence of Lotka’s law. If the observed value is less than the critical value, the null hypothesis is accepted; otherwise, it is rejected. Acceptance of null hypothesis means the presence of Lotka’s law. Coile ( 1978 ) recommends application of the Kolmogorov–Smirnov (generally known as “K-S test”) statistic. See, Trivedi ( 1993 ) on publication lag, Hamermesh ( 1994 ) on time for refereeing, and Gans and Shepherd ( 1994 ) on degree of rejection. Aagaard, K., Kladakis, A., & Nielsen, M. W. (2020). Concentration or dispersal of research funding? Quantitative Science Studies, 1 , 117–149. Google Scholar Ahmi, A., Saidin, S. Z., Mohd Nasir, M. H., & Ismail, Z. (2020). Applicability of Lotka’s law in eXtensible business reporting language (XBRL) studies. International Journal of Advanced Science and Technology, 29 , 282–289. Bino Paul, G. D., & Krishna, M. (2011). Does network matter in knowledge activity. Science, Technology & Society: An International Journal, 16 , 235–255. Article Google Scholar Bino, P. G. D., Subash, S., & Ramanathan, A. (2005). Concentration in knowledge output: A case of economics journals. The European Journal of Comparative Economics, 2 , 261–278. Borgatti, S. P., Everett, M. G., & Freeman, L. C. (2002). Ucinet 6 for Windows: Software for social network analysis . Analytic Technologies. Card, D., & DellaVigna, S. (2017). What do editors maximize? Evidence from four leading economics journals (No. w23282). National Bureau of Economic Research. Chung, K. H., & Cox, R. A. K. (1990). Patterns of productivity in the finance literature: A study of the bibliometric distributions. The Journal of Finance, 45, 301–309. Coile, R. C. (1978). Lotka’s frequency distribution of scientific productivity. Professional Paper No-216 , Centre for Naval Analysis/University of Rochester, Virginia Corbet, S., Dowling, M., Gao, X., Huang, S., Lucey, B., & Vigne, S. A. (2019). An analysis of the intellectual structure of research on the financial economics of precious metals. Resources Policy, 63 , 101416. Cowan, R., & Jonard, N. (2004). Network structure and the diffusion of knowledge. Journal of Economic Dynamics and Control, 28 , 1557–1575. Cowan, R. (2004). Network models of innovation and knowledge diffusion. MERIT Research Memoranda , 2004–01 . Cox, R. A. K., & Chung, K. H. (1991). Patterns of research output and author concentration in the economics literature. The Review of Economics and Statistics, 73, 740–747. Da Silva, S., Perlin, M., Matsushita, R., Santos, A. A., Imasato, T., & Borenstein, D. (2019). Lotka’s law for the Brazilian scientific output published in journals. Journal of Information Science., 45 , 705–709. Dobusch, L., & Kapeller, J. (2013). Striking new paths: Theory and method in path dependence research. Schmalenbach Business Review, 65 , 288–311. Ellison, G. (2002). The slowdown of the economics publishing process. Journal of Political Economy, 110 , 947–993. Gans, J. S., & Shepherd, G. B. (1994). How are the mighty fallen: Rejected classic articles by leading economists. Journal of Economic Perspectives, 8 , 165–179. Goyal, S., Van Der Leij, M. J., & Moraga González, J. L. (2006). Economics: An emerging small world. Journal of political economy, 114 , 403–412. Granovetter, M. (1985). Economic action and social structure: The problem of embeddedness. The American Journal of Sociology, 91 , 481–510. Granovetter, M. (2005). The impact of social structure on economic outcomes. Journal of Economic Perspectives, 19 , 33–50. Guha, R. (2004). Passing EPW and the thinking Indian, accessed from www.himalmag.com/2004/february/passing.htm , February Gupta, B. M., Dhawan, S. M., & Singh, U. (2009). Social science research in India. China and Brazil-A comparative study, DESIDOC Journal of Library and Information Technology, 29 , 15–23. Hamermesh, D. S. (1994). Facts and myths about refereeing. Journal of Economic Perspectives, 8 , 153–163. Hodgson, G. M., & Rothman, H. (1999). The editors and authors of economics journals: A case of institutional oligopoly. Economic Journal, 109 , F165–F186. Kawamura, M., C. D. L. Thomas, Y. Kawag. (2009). Lotka's law and the pattern of scientific productivity in the dental science literature. Medical Informatics and the Internet in Medicine, 24, 309-315 Klamer, A., & van Dalen, H. P. (2002). Attention and the art of scientific publishing. Journal of Economic Methodology, 9, 289–315. Krishna, M., & Paul, G. B. (2017). The structure of collaboration networks: An illustration of Indian economics. Journal of Social Structure , 18 , 0_1–18. Lotka, A. J. (1926). The frequency distribution of scientific productivity. Journal of the Washington Academy of Sciences, 16 , 317–323. Lovell, M. C. (1973). The production of economic literature: An interpretation. Journal of Economic Literature, 11, 27–55. Ministry of Human Resource Development (MHRD) (2016), data accessed from https://mhrd.gov.in/university-and-higher-education Moody, J. (2004). The structure of a social science collaboration network: Disciplinary cohesion from 1963–1999. American Sociological Review, 69 , 213–238. Murphy, L. J. (1973). Lotka’s law in the humanities. Journal of the American Society for Information Sciences, 24 , 461–462. Newman, M. E. J. (2001). ‘The structure of scientific collaboration networks. Proceedings of the National Academy of Sciences, USA, 98 , 404–409. Potter, G. W. (1981). Lotka’s law revisited. Library Trends, 30 , 21–39. Schorr, A. E. (1975). Lotka’s law and map librarianship. Journal of the American Society for Information Sciences, 26 , 189–190. Scott, J. (2000). Social network analysis, a Handbook . (2nd ed.). Sage Publications. Talukdar, D. (2011). Patterns of research productivity in the business ethics literature: Insights from analyses of bibliometric distributions. Journal of Business Ethics, 98 , 137–151. Trivedi, P. K. (1993). An analysis of publication lags in econometrics. Journal of Applied Econometrics, 8 , 93–100. Voos, H. (1974). Lotka and information science. Journal of the American Society for Information Science, 25 , 270–272. Wasserman, S., & Faust, K. (1994). Social network analysis: Methods and applications . Cambridge University Press. Book Google Scholar Yalcintas, A. (2013). The problem of epistemic cost: why do economists not change their minds (About the “Coase Theorem”). American Journal of Economics and Sociology, 72 , 1131–1157. Download references Author informationAuthors and affiliations. Department of Economics and Finance, Birla Institute of Technology and Science Pilani, Vidya Vihar, Pilani, Rajasthan, 333031, India Krishna Muniyoor You can also search for this author in PubMed Google Scholar Corresponding authorCorrespondence to Krishna Muniyoor . Additional informationPublisher's note. Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations. Appendix 1. Pattern of Scientific Productivity in Major Disciplines: an OverviewStudy | Period | Subject field | No. of authors | Key findings |

|---|

Leavens (1953)* | 1933–1952 | Econometrics | 721 | Presence of Lotka’s law | Murphy ( ) | 1959–1968 | Humanities | 170 | Presence of Lotka’s law | Voos ( ) | 1966–1970 | Information Science | 11,005 | Absence of Lotka’s law | Schorr ( ) | 1921–1973 | Map librarianship | 326 | Presence of Lotka’s law | Radhakrishnan and Kernizan (1979)* | 1968–1972 | Computer Science | –– | Absence of Lotka’s law | Chung & Cox ( ) | Inaugural to 1986 | Financial Economics | 6,270 | Presence of Lotka’s law | Cox & Chung ( ) | 1963–1988 | Economics | 13,576 | Presence of Lotka’s law | Kawamura et al. ( ) | 1971–1995 | Dental Science | 43,796 | Presence of Lotka’s law | Talukdar ( ) | 1982–2009 | Business | 4030 | Absence of Lotka’s law | Corbet et al. ( ) | 1990–2017 | Economics | 2521 | Presence of Lotka’s law | Ahmi et al. ( ) | Until April 2020 | XBRL | 648 | Presence of Lotka’s law |

- Compiled by author from their respective studies; *compiled from Gray Potter ( 1981 )

- a The presence of Lotka’s law was confirmed by Potter ( 1981 )

Appendix 2. Share of Top Three Institutional Contributors to Indian Economics Journals, 2005Journals and period | Rank 1 | Rank 2 | Rank 3 | Total |

|---|

Institution (%) | Institution (%) | Institution (%) | (%) |

|---|

IER (1966–2005) | Delhi School of Economics (12.1) | Indian Statistical Institute, Delhi (6.4) | Institute of Economic Growth (6.0) | 24.5 | IEJ (1978–05) | University of Bombay (6.2) | University of Delhi (2.0) | Delhi School of Economics (1.7) | 9.8 | JQE (1986–2005) | Indira Gandhi Institute of Development Research (5.5) | Reserve Bank of India (3.9) | Institute of Economic Growth (3.1) | 12.5 | IJAE (1964–2005) | Punjab Agricultural University (7.7) | Indian Agricultural Research Institute (5.1) | IIM, Ahmadabad (3.3) | 16.1 | IESHR (1985–2005) | University of Delhi (10.5) | Delhi School of Economics (6.1) | Jawaharlal Nehru University (3.2) | 19.7 |

- Tabulated from data compiled by the author

Appendix 3. Some Papers Rejected by Leading Economics Journals and Journals that Published themAuthor | Title of paper | Rejecting journal | Publishing journal |

|---|

Akerlof, George | The Market for “Lemons”: Quality, Uncertainty and the Market Mechanism | American Economic Review Journal of Political Economy Review of Economic Studies | Quarterly Journal of Economics (1970) | Arthur, W. Brian | Competing Technologies, Increasing Returns, and Lock-In by Historical Events | American Economic Review Quarterly Journal of Economics American Economic Review Economic Journal | Economic Journal (1989) | Becker, Gary S., | Competition and Democracy | Journal of Political Economy | Journal of Law and Economics (1958) | Bhagwati, Jagadish | Immiserizing Growth: A Geometrical Note | Quarterly Journal of Economics | Review of Economic Studies (1958) | Buchanan, James M | External and Internal Public Debt | Quarterly Journal of Economics | American Economic Review (1957) | Friedman, Milton | Professor Pigou's Method for Measuring Elasticities of Demand from Budgetary Data | Economic Journal | Quarterly Journal of Economics (1935) | Harrod, Roy | The Law of Decreasing Costs | Economic Journal | Economic Journal (1931) | Krugman, Paul R., | Increasing Returns, Monopolistic Competition, and International Trade | Quarterly Journal of Economics | Journal of International Economics | Modigliani, Franco | Fluctuations in the Savings-Income Ratio: A Problem in Economic Forecasting | Econometrica | Studies of Income and Wealth (1949) | Stolper, Wolfgang, and Samuelson, Paul A | Protection and Real Wages | American Economic Review | Review of Economic Studies (1941) |

- Gans and Shepherd ( 1994 )

Appendix 4. Descriptive Statistics of Collaboration Networks: a ComparisonNetwork properties | EPW | Goyal et al. ( ) |

|---|

Authors in collaboration networks | 1840 | 56,639 | Size of the giant component | 225 | 33,027 | Average degree | 1.92 | 1.672 | Average distance | 8.57 | 2.303 | Clustering coefficient (overall) | 0.69 | 0.157 |

- Data compiled by the author from EPW and Goyal et al. ( 2006 )

Rights and permissionsReprints and permissions About this articleMuniyoor, K. The Structure of Scholarly Publishing: a Case of Economics Research in India. J Knowl Econ 13 , 1801–1818 (2022). https://doi.org/10.1007/s13132-021-00797-8 Download citation Received : 30 July 2020 Accepted : 08 April 2021 Published : 17 April 2021 Issue Date : September 2022 DOI : https://doi.org/10.1007/s13132-021-00797-8 Share this articleAnyone you share the following link with will be able to read this content: Sorry, a shareable link is not currently available for this article. Provided by the Springer Nature SharedIt content-sharing initiative - Author concentration

- Economics journals

- Lotka’s law

- Knowledge creation

- Social network analysis

- Find a journal

- Publish with us

- Track your research

Jun 6th: Why and how the BJP’s tally fell short of its target  - Governing Board

- Funding Support

- Work With Us

- CPR - A Safe Space

- Agriculture

- Air Pollution

- Climate Change

- Environmental Law & Justice

- Energy & Electricity

- Governance, Accountability & Public Finance

- Health & Nutrition

- Indian Politics

- International Relations & Security

- Land Rights

- Social Justice

- State Capacity

- Urbanisation

- Miscellaneous

- Accountability Initiative

- Governance & Public Policy Initiative

- India Infrastructures & Ecologies Program

- Initiative on Cities, Economy & Society

- Initiative on Climate, Energy & Environment

- Land Rights Initiative

- Scaling City Institutions for India Initiative (SCI-FI)

- State Capacity Initiative

- The Jobs Initiative

- The Politics Initiative

- The Technology & Society Initiative

- TREADS: Transboundary Rivers, Ecologies & Development Studies

- Policy Briefs & Reports

- Journal Articles

Working Papers- Book Chapters

- Policy Engagements & Blogs

- Opinion & Commentary

- Faculty Emeriti

- Researchers

- Communications

- Operations & Finance

- Staff Directory

- Upcoming Events

- Past Events

- CPR Dialogues

South Asia in a Changing World: What Citizens in India, Pakistan and Bangladesh think 75 years post-PartitionRahul verma, nishant ranjan, satyam shukla, shamik vatsa praskanva sinharay, melvin kunjumon, yashwant deshmukh, sutanu guru, gaura shukla, aakanksha bariar. Centre for Policy Research and CVoter Foundation August 29, 2024 The partition of India and Pakistan in 1947 changed the sub-continent permanently, and eventually led to the birth of three sovereign countries. Each country has travelled its own unique trajectory, crafted its own political institutions, sought economic prosperity, and pursued external relations with other countries. Citizens in all three countries have adopted their own norms of political and social discourse. Do people in India, Pakistan and Bangladesh still share old cultural and civilisational ties? Have they been able to bury the past and move ahead? The Centre for Policy Research (CPR) and the CVoter Foundation launched an extensive project to mark 75 years of Partition involving a comprehensive survey of citizens of all three countries that was carried out between May and October 2022.  |

IMAGES

VIDEO

COMMENTS

The Indian Economic Journal

The paper is a review of critical current challenges faced by MSMEs in India in COVID-19. COVID-19 is a global pandemic which has caused global economic jeopardy. MSMEs are the backbone of the ...

Indian Economic Review

The study indicates that imports and FDI positively affect economic growth in India. On the other hand, exports and foreign remittances have negative and significant relationship with economic growth. This suggests that exports and foreign remittances take more time to spillover positive impact on economic performance of India.

Agency research offers more credibility and reliability. Five popular economic indicators: GDP growth rate, inflation, unemployment, interest rate and industrial output, were chosen for measurement of the impact. Findings for this paper are in the form of short-term and long-term projections for the key economic indicators.

This paper revisits the threshold level of inflation for India. The empirical analysis follows spline regression for the period 1996-97Q1 to 2019-20Q4. The results suggest the existence of a statistically significant threshold level of inflation at 5 to 5.5% in terms of both CPI and WPI. Below this level, the impact of inflation on growth is generally positive whereas it is negative above ...

India's financial sector has faced many challenges in recent decades, with a large, negative, and persistent credit to GDP gap since 2012. We examine how cyclical financial conditions affect GDP growth using a growth-at-risk (GaR) approach and analyze the link between bank balance sheets, credit growth, and long-term growth using bank-level panel regressions for both public and private banks ...

Research; Working Papers; Explaining the Income and Consumption… Explaining the Income and Consumption Effects of COVID in India ... Working Paper 28935 DOI 10.3386/w28935 Issue Date June 2021. The COVID-19 pandemic led to stark reductions in economic activity in India. We employ CMIE's Consumer Pyramids Household Survey to examine the timing ...

The Indian Journal of Economics was established by Prof. H. Stanley Jevons and Prof. C.D. Thomson of the Department of Economics, University of Allahabad. ... Book Reviews. The Indian Journal of Economics is Registered with the Registrar, News Papers of India (Regd. No. RN.28648/75) and its ISSN is 0019-5170.

Understanding Inflation in India

Working Paper 19024. DOI 10.3386/w19024. Issue Date May 2013. This paper analyzes the effects of the reforms initiated in India following the balance of payments (BOP) crisis of 1991 on economic performance. We do not find persuasive the contention of many analysts that growth accelerated after the mid-1980s when reforms were initiated.

The Society for Economics Research in India (SERI) promotes research collaboration, intellectual exchange and critique among economists in India. Subscribe to the Mailing List Call for Papers - Annual Workshop 2024.

The paper aims to examine the nonlinear effects of rice, wheat and maize crop production on agricultural growth in India from 1960 to 2019. Nonlinear autoregressive distributive lag (NARDL) and ...

The productive sectors—agriculture, industry and services—are pillars of growth and enablers to the dream of India's US$ 5 trillion economic target. The collective growth and contribution of these productive sectors have exhibited dynamic patterns in the history of Indian economy attracting attention of researchers and policy makers.

The present study examines the long-run and short-run relationship between tax structure and state-level growth performance in India for the period 1991-2016. The analysis in this paper is based on the model of Acosta-Ormaechea and Yoo (2012), and for the verification of the relationship between taxation and economic growth the panel regression method is used. With the use of 14 Indian ...

India's Recent Macroeconomic Performance

The pattern and causes of economic growth. in India. Kaushik Basu ∗and Annemie Maertens∗∗. Abstract This paper presents the broad macro parameters of the growth of the Indian economy since ...

RePEc: Research Papers in Economics

The Indian Journal of Labour Economics - SpringerLink

SUBMIT PAPER. Journal of Asian Development Research. Journal indexing and metrics. JOURNAL HOMEPAGE. SUBMIT PAPER. ... School participation in rural India (The Development Economics Discussion Paper Series). London School of Economics. ... The Journal of Applied Economic Research. May 2021. Restricted access. Determinants of Total Factor ...

This study aims to assess the comparative analysis of India and China's economic assistance to Maldives. Maldives is smallest country in South Asia. The republic of Maldives, so far, is one of the least known country in the international community. Maldives, a group of 1200 islands spanning around 90,000 square kilometres in the Indian Ocean Region, has been in the limelight for the last decade.

The study of income inequality and income mobility has been central to understanding India's recent economic development. This paper, based on the first two waves of the India Human Development ...

There is a great deal of disparity in the creation and dissemination of scholarly publications across disciplines. The main objective of the study in this article is three-fold: first, to find empirical evidence of publishing regularity in economics journals in India; second, to examine what accounts for author concentration in journals, with a special focus on economics; and third, to ...

The partition of India and Pakistan in 1947 changed the sub-continent permanently, and eventually led to the birth of three sovereign countries. Each country has travelled its own unique trajectory, crafted its own political institutions, sought economic prosperity, and pursued external relations with other countries. Citizens in all three countries have adopted their own norms […]

Economic reforms, FDI and economic growth in India: A sector level analysis. World Development, 36(7 ... Sen C. (2011). FDI in the service sector-propagator of growth for India? (MPRA Paper No. 30574). Retrieved from http ... This article was published in Asia-Pacific Journal of Management Research and Innovation. View All Journal Metrics ...

The total economic output, or gross domestic product, of Latinos in the U.S. reached $3.7 trillion in 2022, the researchers found, exceeding the historic $3.2 trillion mark set in 2021. The latest figure would make the U.S. Latino GDP the fifth largest GDP in the world for 2022 — greater than India, the United Kingdom and France.

During the first wave of the COVID-19 pandemic, various governments announced lockdowns. India went under lockdown from 25 March 2020 for 21 days. These lockdowns disrupted the social fabric and economic activities. We examined the demographic and socio-economic determinants of COVID-19 infections and deaths across over 400 districts in India.