REMINDER: All RCB offices will be closed on Monday, September 2nd, in observance of Labor Day.

New features have been added to Bill Pay! Find the FAQs here .

Virtual Gift Cards are available in Online & Mobile Banking! Click here for details.

Interested in our new Credit Builder Loan product? Learn more here .

Check out our 8-Month CD and Cash Booster Money Market accounts!

- Open an Account

- Online Banking & Bill Pay

- Mobile Banking

- Financial Planning

- Business Checking

- Business Savings

- Business Services

- Business Online Banking and Bill Pay

- Business Mobile Banking

- Cash Management

- Mortgage & Loans

Business Loans

- Locations & Hours

- In the Community

- Press Releases

- Para Español

- Accessibility

We love investing in our clients’ businesses. We offer lending products to help you strengthen and grow your business in whatever way fits your vision, with competitive rates and helpful service from other committed, local business professionals—us.

Refer-a-Friend

Earn $50 for each friend who opens a NEW RCB Checking Account!*

Our Lending Options

Small business loan.

Get a financial jumpstart with a small business loan from RCB.

We offer a streamlined process for small business loans up to $150,000* to businesses of all types and industries. Whatever your needs may be (new equipment, working capital lines of credit, or purchase inventory), RCB is here to ensure your success.

Should you have questions, our Community Development Officers would be happy to help find the right fit for you and your company.

Contact Our Team

*All loans are subject to credit approval.

Equipment Loans

With an equipment loan from RCB, you don’t have to dip into valuable cash reserves to buy the new equipment, trucks, or vehicles you need to keep your business going strong.

Commercial Construction Loans

RCB can help you build your business—literally—with loans for new construction, improvements to existing buildings, development and community redevelopment projects, with flexible financing structures tailored to your needs.

Business Acquisition Financing

Planning to grow your business by acquisition? Need financing for a family-owned business or buyout? We can provide the financing and guidance to make it work.

Permanent Real Estate Financing

RCB is where the real estate biz gets down to business, with competitive income property financing for industrial, retail, branch, mix-use, residential and other properties.

Lines of Credit

An asset-based line of credit is secured by your business assets rather than cash flow, and can be tied to the value of equipment, inventory, or accounts receivable. It’s a great choice for seasonal funding or letters of credit—and we’ll work with you to design customized lending based on your needs.

Small Business Administration Financing

RCB teams up with the Small Business Administration (SBA) to provide government-guaranteed loans to qualified applicants. It’s a great way to preserve working capital for other expenses while getting more flexible terms than conventional loans.

- Purchase or renovate real estate

- Acquire machinery or specialized equipment

- Supply working capital for ongoing financing needs

Business Financial Forms

We've compiled the list of helpful forms below for your convenience. Click to download.

- Schedule of Business Debt

- Business Rent Roll

- Schedule of Real Estate Owned

- Beneficial Owners Regulation

- Personal Financial Statement

meet our lenders

Put a face to your loan. Our lenders are knowledgeable, friendly, and ready to help.

checking & savings

No matter what size your business, we’ve got an account that fits.

online banking

Wherever-whenever tools for managing your accounts, paying your bills, and more.

keep that cash flowing

We can help, with a full range of business services

mobile banking

Manage your business accounts on the go without missing a beat

checking, savings, you

We’ve got accounts to fit every business need

Get in touch

Ready to learn more about our loan options? Our lenders are ready and waiting to help.

- Search Search Please fill out this field.

Why Do I Need a Business Plan?

Sections of a business plan, the bottom line.

- Small Business

How to Write a Business Plan for a Loan

How to secure business financing

Matt Webber is an experienced personal finance writer, researcher, and editor. He has published widely on personal finance, marketing, and the impact of technology on contemporary arts and culture.

:max_bytes(150000):strip_icc():format(webp)/smda1_crop-f0c167dd2b2144f68f352c63d17f7db5.jpg "business plan loan cooperative bank")

- How to Start a Business: A Comprehensive Guide and Essential Steps

- How to Do Market Research, Types, and Example

- Marketing Strategy: What It Is, How It Works, How To Create One

- Marketing in Business: Strategies and Types Explained

- What Is a Marketing Plan? Types and How to Write One

- Business Development: Definition, Strategies, Steps & Skills

- Business Plan: What It Is, What's Included, and How to Write One

- Small Business Development Center (SBDC): Meaning, Types, Impact

- How to Write a Business Plan for a Loan CURRENT ARTICLE

- Business Startup Costs: It’s in the Details

- Startup Capital Definition, Types, and Risks

- Bootstrapping Definition, Strategies, and Pros/Cons

- Crowdfunding: What It Is, How It Works, and Popular Websites

- Starting a Business with No Money: How to Begin

- A Comprehensive Guide to Establishing Business Credit

- Equity Financing: What It Is, How It Works, Pros and Cons

- Best Startup Business Loans

- Sole Proprietorship: What It Is, Pros & Cons, and Differences From an LLC

- Partnership: Definition, How It Works, Taxation, and Types

- What is an LLC? Limited Liability Company Structure and Benefits Defined

- Corporation: What It Is and How to Form One

- Starting a Small Business: Your Complete How-to Guide

- Starting an Online Business: A Step-by-Step Guide

- How to Start Your Own Bookkeeping Business: Essential Tips

- How to Start a Successful Dropshipping Business: A Comprehensive Guide

A business plan is a document that explains what a company’s objectives are and how it will achieve them. It contains a road map for the company from a marketing, financial, and operational standpoint. Some business plans are more detailed than others, but they are used by all types of businesses, from large, established companies to small startups.

If you are applying for a business loan , your lender may want to see your business plan. Your plan can prove that you understand your market and your business model and that you are realistic about your goals. Even if you don’t need a business plan to apply for a loan, writing one can improve your chances of securing finance.

Key Takeaways

- Many lenders will require you to write a business plan to support your loan application.

- Though every business plan is different, there are a number of sections that appear in every business plan.

- A good business plan will define your company’s strategic priorities for the coming years and explain how you will try to achieve growth.

- Lenders will assess your plan against the “five Cs”: character, capacity, capital, conditions, and collateral.

There are many reasons why all businesses should have a business plan . A business plan can improve the way that your company operates, but a well-written plan is also invaluable for attracting investment.

On an operational level, a well-written business plan has several advantages. A good plan will explain how a company is going to develop over time and will lay out the risks and contingencies that it may encounter along the way.

A business plan can act as a valuable strategic guide, reminding executives of their long-term goals amid the chaos of day-to-day business. It also allows businesses to measure their own success—without a plan, it can be difficult to determine whether a business is moving in the right direction.

A business plan is also valuable when it comes to dealing with external organizations. Indeed, banks and venture capital firms often require a viable business plan before considering whether they’ll provide capital to new businesses.

Even if a business is well-established, lenders may want to see a solid business plan before providing financing. Lenders want to reduce their risk, so they want to see that a business has a serious and realistic plan in place to generate income and repay the loan.

Every business is different, and so is every business plan. Nevertheless, most business plans contain a number of generic sections. Common sections are: executive summary, company overview, products and services, market analysis, marketing and sales plan, operational plan, and management team. If you are applying for a loan, you should also include a funding request and financial statements.

Let’s look at each section in more detail.

Executive Summary

The executive summary is a summary of the information in the rest of your business plan, but it’s also where you can create interest in your business.

You should include basic information about your business, including what you do, where you are based, your products, and how long you’ve been in business. You can also mention what inspired you to start your business, your key successes so far, and your growth plans.

Company Overview

In this section, focus on the core strengths of your business, the problem you want to solve, and how you plan to address it.

Here, you should also mention any key advantages that your business has over your competitors, whether this is operating in a new market or a unique approach to an existing one. You should also include key statistics in this section, such as your annual turnover and number of employees.

Products and Services

In this section, provide some details of what you sell. A lender doesn’t need to know all the technical details of your products but will want to see that they are desirable.

You can also include information on how you make your products, or how you provide your services. This information will be useful to a lender if you are looking for financing to grow your business.

Market Analysis

A market analysis is a core section of your business plan. Here, you need to demonstrate that you understand the market you are operating in, and how you are different from your competitors. If you can find statistics on your market, and particularly on how it is projected to grow over the next few years, put them in this section.

Marketing and Sales Plan

Your marketing and sales plan gives details on what kind of new customers you are looking to attract, and how you are going to connect with them. This section should contain your sales goals and link these to marketing or advertising that you are planning.

If you are looking to expand into a new market, or to reach customers that you haven’t before, you should explain the risks and opportunities of doing so.

Operational Plan

This section explains the basic requirements of running your business on a day-to-day basis. Your exact requirements will vary depending on the type of business you run, but be as specific as possible.

If you need to rent office space, for example, you should include the cost in your operational plan. You should also include the cost of staff, equipment, and any raw materials required to run your business.

Management Team

The management team section is one of the most important sections in your business plan if you are applying for a loan. Your lender will want reassurance that you have a skilled, experienced, competent, and reliable senior management team in place.

Even if you have a small team, you should explain what makes each person qualified for their position. If you have a large team, you should include an organizational chart to explain how your team is structured.

Funding Request

If you are applying for a loan, you should add a funding request. This is where you explain how much money you are looking to borrow, and explain in detail how you are going to use it.

The most important part of the funding-request section is to explain how the loan you are asking for would improve the profitability of your business, and therefore allow you to repay your loan.

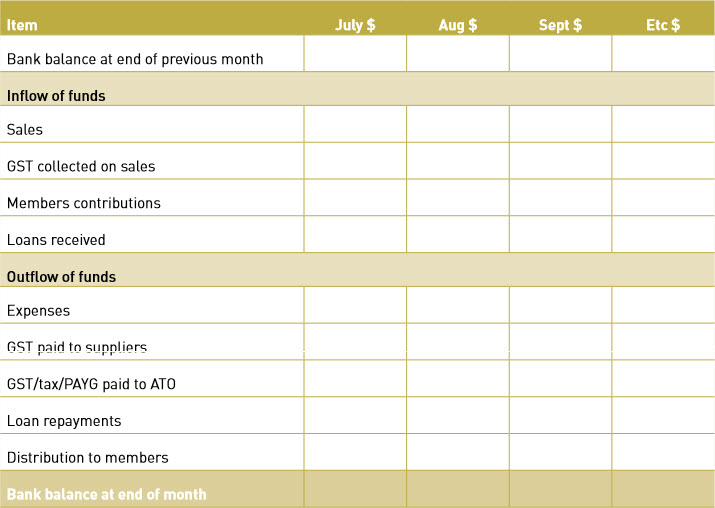

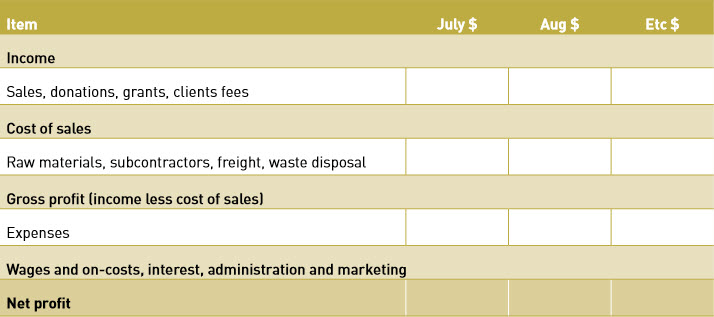

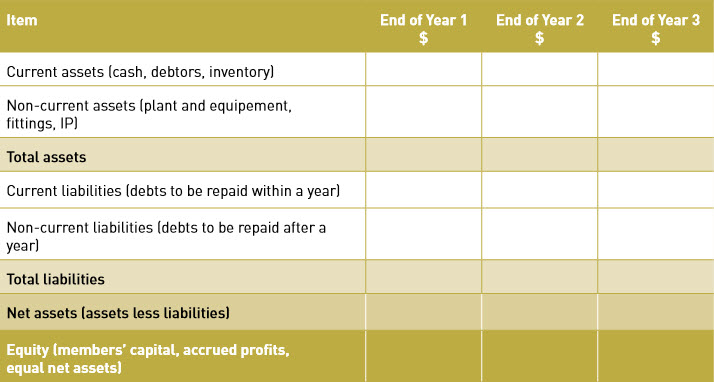

Financial Statements

Most lenders will also ask you to provide evidence of your business finances as part of your application. Graphs and charts are often a useful addition to this section, because they allow your lender to understand your finances at a glance.

The overall goal of providing financial statements is to show that your business is profitable and stable. Include three to five years of income statements, cash flow statements, and balance sheets. It can also be useful to provide further analysis, as well as projections of how your business will grow in the coming years.

What Do Lenders Look for in a Business Plan?

Lenders want to see that your business is stable, that you understand the market you are operating in, and that you have realistic plans for growth.

Your lender will base their decision on what are known as the “five Cs.” These are:

- Character : You can stress your good character in your executive summary, company overview, and your management team section.

- Capacity : This is, essentially, your ability to repay the loan. Your lender will look at your growth plans, your funding request, and your financial statements in order to assess this.

- Capital : This is the amount of money you already have in your business. The larger and more established your business is, the more likely you are to be approved for finance, so highlight your capital throughout your business plan.

- Conditions : Conditions refer to market conditions. In your market analysis, you should be able to prove that your business is well-positioned in relation to your target market and competitors.

- Collateral : Depending on your loan, you may be asked to provide collateral , so you should provide information on the assets you own in your operational plan.

How Long Does It Take to Write a Business Plan?

The length of time it takes to write a business plan depends on your business, but you should take your time to ensure it is thorough and correct. A business plan has advantages beyond applying for a loan, providing a strategic focus for your business.

What Should You Avoid When Writing a Business Plan?

The most common mistake that business owners make when writing a business plan is to be unrealistic about their growth potential. Your lender is likely to spot overly optimistic growth projections, so try to keep it reasonable.

Should I Hire Someone to Write a Business Plan for My Business?

You can hire someone to write a business plan for your business, but it can often be better to write it yourself. You are likely to understand your business better than an external consultant.

Writing a business plan can benefit your business, whether you are applying for a loan or not. A good business plan can help you develop strategic priorities and stick to them. It describes how you are going to grow your business, which can be valuable to lenders, who will want to see that you are able to repay a loan that you are applying for.

U.S. Small Business Administration. “ Write Your Business Plan .”

U.S. Small Business Administration. “ Market Research and Competitive Analysis .”

U.S. Small Business Administration. “ Fund Your Business .”

Navy Federal Credit Union. “ The 5 Cs of Credit .”

:max_bytes(150000):strip_icc():format(webp)/GettyImages-904536858-c089bc26f4fd4025b23f536345ba73ae.jpg "business plan loan cooperative bank")

- Terms of Service

- Editorial Policy

- Privacy Policy

10 Steps to Launch Your Own Co-operative Bank and Serve Your Community

Related blogs.

- Unveiling the Hidden Profits of the Co-Operative Bank: Discovering the True Wealth behind the Veil

- Breaking Down the Costs: How to Start Your Own Cooperative Bank and Build a Better Banking Industry

- Boost Your Co-Op Bank's Performance: Top 7 KPI Metrics to Track

1. Develop A Business Plan

Starting a co operative bank business requires careful planning and execution. Before you open your doors for business, it's essential to develop a business plan that outlines your goals, strategies, and potential challenges. Here are some chapters that your business plan should cover:

- Executive Summary: This section should provide an overview of your co operative bank business, including your mission, values, and vision. It should also include a brief summary of your financial projections.

- Market Analysis: In this section, you should research your target market and competition. This will help you identify opportunities and potential challenges you might face when starting and running your co operative bank business.

- Marketing Strategies: Here you should outline how you will market your co operative bank business to attract customers. Consider using strategies such as advertising, social media, and networking events.

- Operations Plan: This section should detail how your co operative bank business will operate. Topics to consider include staffing, technology, customer service, and compliance with regulations.

- Financial Projections: This is where you will outline your co operative bank business's financial projections. You should include revenue and expense projections, as well as projections for growth and profitability.

- Risks and Challenges: It's essential to identify potential risks and challenges that your co operative bank business may face. This will help you develop strategies to overcome these challenges and minimize risk.

- Management and Ownership: This section should detail who will own and manage your co operative bank business. It should also include information about your team's experience and qualifications.

Tips & Tricks:

- Be specific about your target market and competition. This will help you develop effective marketing strategies.

- Ensure that your financial projections are realistic and based on data and research.

- Develop contingency plans to mitigate potential risks and challenges.

| Co Operative Bank Business Plan ADD TO CART |

2. Outline Financial Model

Before launching a co operative bank, it is crucial to have a financial model in place. This will help you determine the viability of your business, project future revenue and expenses, and make informed decisions about how to allocate resources.

Revenue Streams

- List all possible sources of revenue for the co operative bank, including interest on loans, fees for financial services, and commissions on investment products.

- Estimate the percentage of revenue that will come from each source.

- Consider how revenue will be affected by market conditions, interest rates, and competition.

- List all fixed and variable expenses, including rent, salaries, legal fees, and technology costs.

- Estimate the monthly, quarterly, and annual costs of each expense.

- Identify any major capital expenses that will be required during the start-up phase or in the future.

Projections

- Use the revenue streams and expenses to project a monthly and annual income statement , balance sheet , and cash flow statement .

- Include assumptions such as customer base growth rate, increase in loan defaults, and market trends.

- Consider different scenarios, such as best-case, worst-case, and moderate-case situations.

Tips & Tricks

- Be realistic with your revenue and expense estimates. It's better to have conservative projections and outperform them than to have aggressive projections and fall short.

- Consult with financial experts, such as accountants and financial analysts, to ensure your financial model is accurate and complete.

- Update your financial model regularly, especially when market conditions or your business strategy change.

Creating a solid financial model is a critical step in launching a co operative bank. It will help you identify potential pitfalls, plan for growth, and attract investors if needed. Take the time to do it right and use it as a roadmap for your business.

3. Secure Funding

Starting a co operative bank business is a noble idea, but it requires a significant amount of investment to turn that idea into a functioning entity. So, the first step towards realizing your dream is to secure funding to support your startup expenses and ongoing operations. Here’s how:

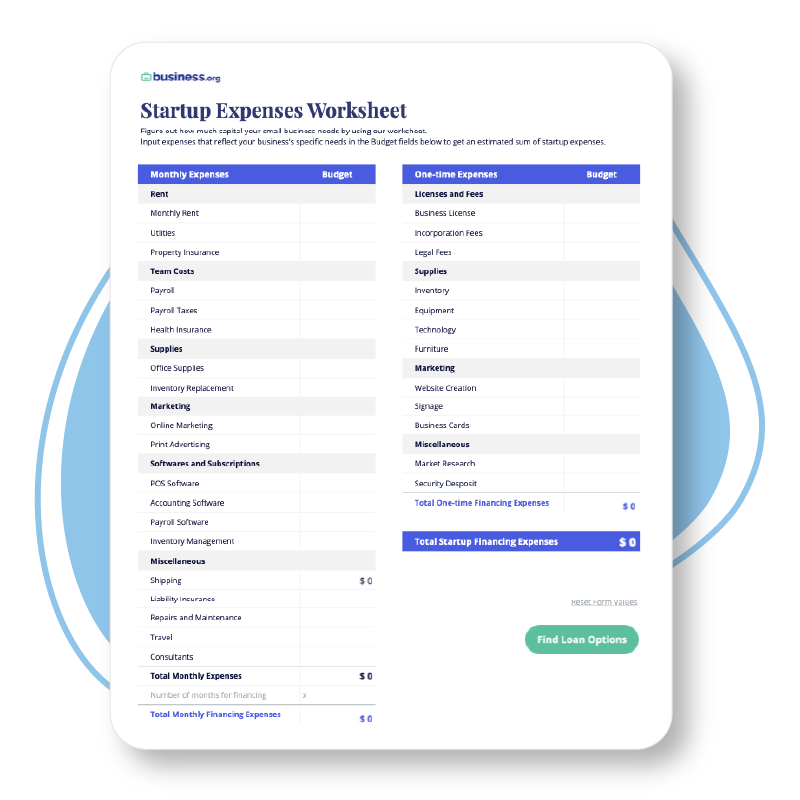

- Assess your financial needs: Before you approach any potential investors or lenders, make sure you have a clear understanding of your financial requirements. Make a list of your startup expenses, such as legal fees, registrations, office space rent, equipment, and salaries for staff, and estimate your ongoing operating costs, such as loan payments, salaries, and utilities. This will help you identify the amount of funding required for the launch and see how much money you need to operate.

- Build a reliable business plan: A business plan is an essential tool to demonstrate your vision, competitiveness, and potential profitability. A well-crafted business plan should include your mission statement, executive summary, industry analysis, marketing plan, financial projections, and funding request. A robust business plan that highlights your strengths and opportunities while addressing potential challenges and risks can help you stand out from other competing businesses, and it can be a strong selling point in securing funding.

- Explore funding options: Co-operative banks can explore a variety of financing options, including debt and equity financing. Debt financing involves a loan, usually from a bank, where you agree to pay back with interest over a set period. Equity financing involves selling shares of your business to investors who become your partners and share in your profits and losses. You can also consider financing from government schemes or other grants. It is best to research and investigate multiple financing options that best fit your business's needs and choose the option that provides the longest repayment term with the lowest interest rates.

- Prepare your pitch: Once you have assessed your financial needs and identified potential funding sources, it’s time to prepare your pitch. A pitch should be a persuasive presentation that highlights your business, its goals, objectives, competitive advantage, and the potential for success. Your pitch should also include your business plan and financial projections and address potential challenges and risks to investors.

- Approach potential investors or lenders: After preparing your pitch, you can approach potential investors or lenders. Make sure you have researched your target market and investors, and reach out to them with a personalized message tailored to their interests. You can also consider funding from family and friends or crowdfunding sites to generate investment funds. But, you need to be thoroughly familiar with regulations, legalities and taxation surrounding the raising of funds through such sources.

Tip and Tricks:

- Consider local co-operative banks as potential investors or lenders.

- Ensure that you understand all the terms and conditions of any lending agreement before signing

- If you do not get approved for funding at first, keep pushing. There are options for second chances.

With these steps outlined above, you should have the necessary knowledge to help you secure funding for starting a co operative bank business. Keep in mind that the competition for funding is high, so make sure your business plan and pitch stand out. Once you receive the funding required, efficient management is essential to a successful start-up.

4. Identify Suitable Location

Once you have researched, planned & executed the legal formalities, and set up the necessary infrastructure, it's time to find the perfect location for your co-operative bank. Here are some crucial steps to take to identify the most suitable location:

- Consider the demographics: Analyze the demographics of the area you are considering before making any decisions. Make sure the population is dense enough to sustain your business, and there is a need for co-operative banking in the area.

- Accessibility: Evaluate the accessibility of the location for your customers. A location that is easy to reach via public transportation, highways, or main roads is always an added advantage.

- Competition: Research the competition in the area. Consider opening your co-operative bank in an area where competitive banks have not ventured, or there is a gap in services being provided.

- Infrastructure & Security: Ensure that the location has the necessary infrastructure for banking, such as power, water supply, and proper security measures to protect the bank and its employees.

Tips & Trics:

- Consider renting a location rather than buying it as it reduces the initial investment.

- If you are considering setting up multiple branches, a centrally located office would be ideal.

- Consider the availability of parking and security cameras in the area for added customer convenience & safety.

By keeping these tips in mind and carefully selecting the location of your co-operative bank, you can ensure maximum revenue generation and business growth. Conduct a thorough analysis and make a well-informed decision that will benefit your bank in the long run.

5. Register The Business

Now that you have your business plan, funding, location, and team in place, it’s time to register your co-operative bank business.

Steps to Register Your Co-Operative Bank Business

- Choose a name for your business: First and foremost, you need to choose a name for your co-operative bank business. It should be unique and not already registered with the relevant authorities.

- Get your company registered: Register your co-operative bank business with the Registrar of Co-operative Societies. You will need to submit the necessary documents and pay the required fees.

- Get your business license: Once your business is registered, you need to obtain a license to operate your co-operative bank business. This license will be issued by the State Department of Co-operative Development.

- Register with the Central Bank of Kenya: Your co-operative bank business needs to be registered with the Central Bank for licensing and regulation.

- Obtain a Tax Identification Number (TIN): You will need to obtain a TIN from the Kenya Revenue Authority to handle taxes.

- Get your business permits: Depending on the area where your co-operative bank business is located, you may need to obtain other permits and licenses as per the local regulations.

- Open a bank account: Once you have all the necessary documents, it’s time to open a bank account for your co-operative bank business. This account will be used to deposit funds and manage finances.

- Register online: Many authorities offer online registration services. Take advantage of this to make the process quick and easy.

- Hire an attorney: You can hire an attorney to help you through the registration process and ensure that everything is done correctly.

Tips & Trics

- Research your competition: Before registering your business, do some research to find out what other co-operative banks in the area are offering. Use this information to differentiate your business and make it more attractive to potential customers.

- File your papers on time: Make sure you submit all the necessary documents on time to prevent any delays in the registration process.

- Be patient: The registration process can take some time, so be patient and stay positive.

Registering your co-operative bank business can seem like a daunting task, but with these steps and tips, you’ll be well on your way to launching a successful business.

6. Obtain Necessary Licenses

Before starting any co-operative bank business in any country, one must have to follow legal formalities and obtain the required licenses. The banking industry is one of the most regulated industries globally; Hence, being a financial institution, co-operative banks have to comply with strict legal policies and also obtain licenses to operate in a country.

- Obtain Approval from RBI: In India, the Reserve Bank of India is the governing body that grants licenses to co-operative banks. One has to submit all necessary documents and fulfill eligibility criteria to obtain approval for the license.

- Registration with ROC: In India, every co-operative society needs to register under the Registrar of Co-operative Societies (ROC) of the respective state. The application process may vary for different states.

- Operating Licenses: Once the bank receives approval from RBI and registration from ROC, they must obtain licenses to operate, including a license under the Banking Regulation Act and the Society Act.

- Insurance: The co-operative bank needs to have insurance coverage to protect its assets and depositors' deposits. In India, the Deposit Insurance and Credit Guarantee Corporation (DICGC) provides deposit insurance for co-operative banks.

Tips & Tricks for Obtaining Licenses:

- Consult with a Lawyer: It's crucial to consult with a legal professional before initiating the process of obtaining licenses to avoid any legal complications.

- Keep Record of Documents: Keeping records of all the necessary documents is crucial while applying for licenses. This will not only help keep organized but also speed up the approval process.

- Be Persistent: The process of obtaining licenses can be time-consuming and prolonged. Hence, being persistent and following up with the respective governing bodies is essential.

Once all the licenses are obtained, and the bank has all the necessary approvals, they can begin operations and focus on providing quality services to their customers.

7. Establish A Board Of Directors

The success of a co-operative bank heavily depends on the board of directors' leadership and management skills. Therefore, it is essential to establish a board of directors that is experienced and knowledgeable in co-operative banking and its regulations. Here are some of the important aspects to consider:

- Election Process: The election process for the board of directors must be democratic, transparent, and follow the guidelines of the co-operative society's governing act.

- Composition: The board of directors must comprise members with diverse skills and expertise in the relevant fields (finance, law, risk management, etc.)

- Responsibilities: The board of directors must be responsible for overseeing the bank's overall operations, making strategic decisions, and ensuring the co-operative bank's sustainability and growth.

Key tip: Ensure that every director is trained and understands their roles and responsibilities.

- Conduct regular training and development sessions to update the directors' knowledge.

- Provide ongoing support, guidance, and feedback to ensure that the directors are performing at their best.

Trick: Select candidates that share your bank's values and vision.

- Choose candidates that share your co-operative bank's vision, mission, and values.

- Carefully evaluate potential directors' personalities to ensure they align with your bank's cultural and social values.

Pro tip: Establish a board charter that outlines the board's roles, responsibilities, and governance processes.

- The charter should clearly define the board's goals, decision-making processes, and ethical standards.

- Ensure that the charter aligns with your co-operative bank's by-laws and codes of conduct.

Overall, establishing a board of directors in your co-operative bank is crucial for the bank's success and growth. Choose the directors carefully, ensure they are trained and understand their roles, and establish clear governance processes to ensure effective leadership and management.

8. Finalize Staff Requirements

One of the critical components of starting any businesses is hiring the right staff, and launching a co-operative bank is no exception. To ensure the success of your cooperative bank, it is essential to recruit capable and qualified professionals who share your vision and values. Therefore, you need to finalize your staff requirements as part of your checklist before opening the bank. Here's a guide to help you with this process:

- 1. Determine the Required Staff Strength: Before advertising for job openings, you need to assess your bank's workload and identify the requisite staff strength. Factors such as the bank's size, location, operations, and the services offered can influence this evaluation. A typical co-op bank would require a manager, tellers, bookkeepers, loan officers, and customer service representatives, among others.

- 2. Define Job Descriptions and Roles: The next step is to establish the various roles and responsibilities for each staff member based on their job titles. It's crucial to have clearly defined job descriptions to mitigate role ambiguity, boost productivity, and ensure accountability competently.

- 3. Determine the Eligibility Criteria: You must set a clear and concise eligibility criterion for job applicants to ensure that they match the qualifications needed. Criteria such as academic qualifications, years of experience, communicative abilities, and other crucial attributes should be considered when creating this criterion. It's important to prioritize hiring individuals with integrity, excellent work ethic, and experience in the banking sector.

- 4. Advertise the Job Openings: Once the eligibility requirement is established, you can advertise the job vacancies through different channels such as online job searches, local newspapers, and professional networks. Ensure that you provide a detailed job description and the required qualifications to attract the most suitable candidates to apply.

- 5. Conduct Interviews: In this stage, you will need to review and shortlist resumes that match the eligibility criteria, followed by the actual interviews. You can select a set of qualified individuals to proceed to the next stage of the recruitment process based on the results of the interviews.

- 6. Conduct Reference Checks: After shortlisting the candidates, it's imperative to conduct background checks and reference checks to verify their experiences and ensure that there are no red flags or issues with their past work history.

- 7. Offer Letters: After successfully completing reference checks, it's time to send out offer letters to successful candidates, highlighting the job responsibilities, salary, benefits, and the start date. Ensure that the new employees sign the offer letter as an acknowledgment of acceptance of the terms and conditions set forth in the letter.

- 8. Onboarding and Training: The final step is to ensure that the new employees undergo a thorough induction process to familiarize themselves with the bank's policies, procedures, systems, and culture. Providing comprehensive training will help them acquire necessary skills and knowledge, thus maximizing their productivity and efficiency as employees.

- Ensure that you take necessary precautions to prevent nepotism or favoritism while hiring.

- Consider including a probationary period before making a formal offer of employment.

- Set realistic targets for your new employees, and provide them with regular feedback on their performance.

9. Set Up Necessary Technology

Before launching your cooperative bank, you need to make sure you have the necessary technology in place. This will ensure that your operations run smoothly and your customers are satisfied with your services.

Here are some of the technology requirements you need to consider:

- Core Banking Software: This is a fundamental requirement for every bank, and it will enable you to manage your banking operations, such as account opening, deposits, withdrawals, loans, and more. You should choose a software that is user-friendly, secure, and scalable.

- Internet Banking: In today's digital age, most customers prefer to do their banking online. Therefore, you need to offer internet banking services that enable your customers to access their accounts, make transactions, pay bills, and more.

- Mobile Banking: Mobile banking apps are gaining popularity, especially among younger generations. You need to provide a mobile banking app that is convenient, easy to use, and secure.

- ATMs: ATMs are a must-have for any bank, and they provide convenience to your customers. You should consider installing ATMs at strategic locations, such as near shopping malls, universities, and residential areas.

- Payment System: Your cooperative bank should have a payment system that supports various payment options, such as debit and credit cards, electronic fund transfers, and mobile payments.

- Consider outsourcing your technology needs to a reliable vendor who has experience in providing technology solutions to banks.

- Invest in robust security measures to protect your customers' data and prevent fraudulent activities.

- Regularly upgrade your technology to keep up with the latest trends and improve customer satisfaction.

Setting up the technology infrastructure for your cooperative bank is an essential step that requires careful planning and execution. Ensure that you have the necessary resources, budget, and expertise to implement your technology solutions successfully.

10. Introduce Products/Services To The Market

Introducing a new product or service to the market can be a daunting task, especially for a co-operative bank. You need to ensure that your product or service stands out and is attractive enough to capture the attention of potential customers. Here are some steps to help you introduce your product or service to the market:

- 1. Conduct Market Research: Before introducing your product or service, it is important to conduct thorough market research to identify your target audience and their needs. This will enable you to tailor your product or service to meet their needs and preferences.

- 2. Develop a Marketing Plan: Once you have identified your target audience, you need to develop a comprehensive marketing plan that outlines your strategy for promoting your product or service. Your marketing plan should include the channels you will use to promote your product or service, such as social media, email marketing, or direct mail.

- 3. Create a Product Launch Plan: You will need a product launch plan that outlines the steps you will take to introduce your product or service to the market. Your launch plan should include the date of the launch, the channels you will use to promote your product or service, and the target audience.

- 4. Develop a Pricing Strategy: You will need to develop a pricing strategy that is attractive enough to potential customers but still profitable for your co-operative bank. You should consider the cost of production, the competition, and the value of your product or service before setting a price.

- 5. Conduct a Soft Launch: Conducting a soft launch will enable you to test your product or service with a small group of customers before introducing it to the wider market. This will enable you to identify any issues and make necessary adjustments before the official launch.

- 6. Plan a Launch Event: A launch event can create excitement and generate interest in your product or service. It is an opportunity to showcase your product or service and engage your target audience. You can organize a launch event in collaboration with other organizations or partners.

- 7. Leverage Digital Marketing: Digital marketing is an effective way to promote your product or service to a wider audience. You can use social media, email marketing, paid advertising, and search engine optimization (SEO) to reach your target audience.

- 8. Offer Incentives: Offering incentives such as discounts, free trials, and loyalty rewards can encourage potential customers to try your product or service. This can be an effective way to generate interest and attract new customers.

- 9. Monitor and Evaluate: After launching your product or service, it is important to monitor and evaluate its performance. This will enable you to identify any issues and make necessary adjustments to improve the product or service.

- 10. Provide Excellent Customer Service: Providing excellent customer service is crucial to the success of your product or service. You need to ensure that your customers are satisfied and their needs are met. This will create loyalty and generate positive word-of-mouth.

Tips and Tricks:

- Identify the USP (Unique Selling Point) of your product or service and highlight it in your marketing campaigns.

- Engage with your customers through social media and online platforms to build a community around your product or service.

- Invest in customer feedback and use it to improve your product or service, and stay ahead of the competition.

5-Year Excel

MAC & PC Compatible

Immediate Download

- Choosing a selection results in a full page refresh.

- Credit cards

- View all credit cards

- Banking guide

- Loans guide

- Insurance guide

- Personal finance

- View all personal finance

- Small business

- Small business guide

- View all taxes

You’re our first priority. Every time.

We believe everyone should be able to make financial decisions with confidence. And while our site doesn’t feature every company or financial product available on the market, we’re proud that the guidance we offer, the information we provide and the tools we create are objective, independent, straightforward — and free.

So how do we make money? Our partners compensate us. This may influence which products we review and write about (and where those products appear on the site), but it in no way affects our recommendations or advice, which are grounded in thousands of hours of research. Our partners cannot pay us to guarantee favorable reviews of their products or services. Here is a list of our partners .

How to Write a Successful Business Plan for a Loan

Many, or all, of the products featured on this page are from our advertising partners who compensate us when you take certain actions on our website or click to take an action on their website. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and here's how we make money .

Table of Contents

What does a loan business plan include?

What lenders look for in a business plan, business plan for loan examples, resources for writing a business plan.

A comprehensive and well-written business plan can be used to persuade lenders that your business is worth investing in and hopefully, improve your chances of getting approved for a small-business loan . Many lenders will ask that you include a business plan along with other documents as part of your loan application.

When writing a business plan for a loan, you’ll want to highlight your abilities, justify your need for capital and prove your ability to repay the debt.

Here’s everything you need to know to get started.

How much do you need?

with Fundera by NerdWallet

We’ll start with a brief questionnaire to better understand the unique needs of your business.

Once we uncover your personalized matches, our team will consult you on the process moving forward.

A successful business plan for a loan describes your financial goals and how you’ll achieve them. Although business plan components can vary from company to company, there are a few sections that are typically included in most plans.

These sections will help provide lenders with an overview of your business and explain why they should approve you for a loan.

Executive summary

The executive summary is used to spark interest in your business. It may include high-level information about you, your products and services, your management team, employees, business location and financial details. Your mission statement can be added here as well.

To help build a lender’s confidence in your business, you can also include a concise overview of your growth plans in this section.

Company overview

The company overview is an area to describe the strengths of your business. If you didn’t explain what problems your business will solve in the executive summary, do it here.

Highlight any experts on your team and what gives you a competitive advantage. You can also include specific details about your business such as when it was founded, your business entity type and history.

Products and services

Use this section to demonstrate the need for what you’re offering. Describe your products and services and explain how customers will benefit from having them.

Detail any equipment or materials that you need to provide your goods and services — this may be particularly helpful if you’re looking for equipment or inventory financing . You’ll also want to disclose any patents or copyrights in this section.

Market analysis

Here you can demonstrate that you’ve done your homework and showcase your understanding of your industry, current outlook, trends, target market and competitors.

You can add details about your target market that include where you’ll find customers, ways you plan to market to them and how your products and services will be delivered to them.

» MORE: How to write a market analysis for a business plan

Marketing and sales plan

Your marketing and sales plan provides details on how you intend to attract your customers and build a client base. You can also explain the steps involved in the sale and delivery of your product or service.

At a high level, this section should identify your sales goals and how you plan to achieve them — showing a lender how you’re going to make money to repay potential debt.

Operational plan

The operational plan section covers the physical requirements of operating your business on a day-to-day basis. Depending on your type of business, this may include location, facility requirements, equipment, vehicles, inventory needs and supplies. Production goals, timelines, quality control and customer service details may also be included.

Management team

This section illustrates how your business will be organized. You can list the management team, owners, board of directors and consultants with details about their experience and the role they will play at your company. This is also a good place to include an organizational chart .

From this section, a lender should understand why you and your team are qualified to run a business and why they should feel confident lending you money — even if you’re a startup.

Funding request

In this section, you’ll explain the amount of money you’re requesting from the lender and why you need it. You’ll describe how the funds will be used and how you intend to repay the loan.

You may also discuss any funding requirements you anticipate over the next five years and your strategic financial plans for the future.

» Need help writing? Learn about the best business plan software .

Financial statements

When you’re writing a business plan for a loan, this is one of the most important sections. The goal is to use your financial statements to prove to a lender that your business is stable and will be able to repay any potential debt.

In this section, you’ll want to include three to five years of income statements, cash flow statements and balance sheets. It can also be helpful to include an expense analysis, break-even analysis, capital expenditure budgets, projected income statements and projected cash flow statements. If you have collateral that you could put up to secure a loan, you should list it in this section as well.

If you’re a startup that doesn’t have much historical data to provide, you’ll want to include estimated costs, revenue and any other future projections you may have. Graphs and charts can be useful visual aids here.

In general, the more data you can use to show a lender your financial security, the better.

Finally, if necessary, supporting information and documents can be added in an appendix section. This may include credit histories, resumes, letters of reference, product pictures, licenses, permits, contracts and other legal documents.

| 5.0 | 4.7 | 4.5 |

| 20.00-50.00% | 27.20-99.90% | 15.22-45.00% |

| 625 | 625 | 660 |

Lenders will typically evaluate your loan application based on the five C’s — or characteristics — of credit : character, capacity, capital, conditions and collateral. Although your business plan won't contain everything a lender needs to complete its assessment, the document can highlight your strengths in each of these areas.

A lender will assess your character by reviewing your education, business experience and credit history. This assessment may also be extended to board members and your management team. Highlights of your strengths can be worked into the following sections of your business plan:

Executive summary.

Company overview.

Management team.

Capacity centers on your ability to repay the loan. Lenders will be looking at the revenue you plan to generate, your expenses, cash flow and your loan payment plan. This information can be included in the following sections:

Funding request.

Financial statements.

Capital is the amount of money you have invested in your business. Lenders can use it to judge your financial commitment to the business. You can use any of the following sections to highlight your financial commitment:

Operational plan.

Conditions refers to the purpose and market for your products and services. Lenders will be looking for information such as product demand, competition and industry trends. Information for this can be included in the following sections:

Market analysis.

Products and services.

Marketing and sales plan.

Collateral is an asset pledged to a lender to guarantee the repayment of a loan. This can be equipment, inventory, vehicles or something else of value. Use the following sections to include information on assets:

» MORE: How to get a business loan

Writing a business plan for a loan application can be intimidating, especially when you’re just getting started. It may be helpful to use a business plan template or refer to an existing sample as you’re going through the draft process.

Here are a few examples that you may find useful:

Business Plan Outline — Colorado Small Business Development Center

Business Plan Template — Iowa Small Business Development Center

Writing a Business Plan — Maine Small Business Development Center

Business Plan Workbook — Capital One

Looking for a business loan?

See our overall favorites, or narrow it down by category to find the best options for you.

on NerdWallet's secure site

U.S. Small Business Administration. The SBA offers a free self-paced course on writing a business plan. The course includes several videos, objectives for you to accomplish, as well as worksheets you can complete.

SCORE. SCORE, a nonprofit organization and resource partner of the SBA, offers free assistance that includes a step-by-step downloadable template to help startups create a business plan, and mentors who can review and refine your plan virtually or in person.

Small Business Development Centers. Similarly, your local SBDC can provide assistance with business planning and finding access to capital. These organizations also have virtual and in-person training courses, as well as opportunities to consult with business experts.

Business plan software. Although many business plan software platforms require a subscription, these tools can be useful if you want a templated approach that can break the process down for you step-by-step. Many of these services include a range of examples and templates, instruction videos and guides, and financial dashboards, among other features. You may also be able to use a free trial before committing to one of these software options.

A loan business plan outlines your business’s objectives, products or services, funding needs and finances. The goal of this document is to convince lenders that they should approve you for a business loan.

Not all lenders will require a business plan, but you’ll likely need one for bank and SBA loans. Even if it isn’t required, however, a lean business plan can be used to bolster your loan application.

Lenders ask for a business plan because they want to know that your business is and will continue to be financially stable. They want to know how you make money, spend money and plan to achieve your financial goals. All of this information allows them to assess whether you’ll be able to repay a loan and decide if they should approve your application.

On a similar note...

Home » Blog » Business Loans » How To Write A Business Plan For A Loan

💳 Save money on credit card processing with one of our top 5 picks for 2024

Level Up Your Business Today

Join the thousands of people like you already growing their businesses and knowledge with our team of experts. We deliver timely updates, interesting insights, and exclusive promos to your inbox.

How To Write A Business Plan For A Loan

A solid business plan is often critical to securing funding for your small business. Learn how to create a business plan for a loan that includes the information lenders want to see.

WRITTEN & RESEARCHED BY

Lead Staff Writer

Last updated on Updated August 18, 2024

REVIEWED BY

Editor & Senior Staff Writer

- Elements of a good business plan include an executive summary, company description, products and services, market analysis, marketing and sales plan, organizational structure, and other important information.

- Your business plan should address the "5 Cs of Credit" by demonstrating your business's financial health, investment, repayment ability, market conditions, and available assets.

- To improve loan approval chances, avoid jargon, show clear cash flow projections, document personal investment, seek professional help if needed, and be willing to revise your plan

A business plan is a crucial business document you need to have on hand when applying for business loans. However, the mere thought of writing a business plan for a loan is intimidating to a lot of business owners.

A one-page business plan may be sufficient for certain types of small business loans (for example, online loans), but bank loans and SBA loans typically require a more in-depth business plan that delves further into your financials.

If you need to write a business plan for a loan, you’ve come to the right place. Keep reading to learn more about everything you need to include in your business plan to improve your chances for loan approval.

Table of Contents

What Is A Business Plan For A Loan?

10 key sections to include in your business plan, what do lenders look for in a business plan, business plan examples, resources for writing a business plan for a loan, final thoughts on writing a business plan for a loan.

A business plan is a written document that provides a complete overview of your business, including information about your business’s services, strategies, finances, and goals. All businesses should have a business plan, but a business plan is especially important when applying for a business loan.

Most business plans should include some version of the following sections. Depending on your industry and other factors, such as whether you own a startup or established business, some sections could be condensed or combined. The exact verbiage for section titles can vary, as well.

For a business plan that’s longer than one page, it’s a good idea to preface these sections with a cover page and table of contents.

Executive Summary

This section is a condensed version of your entire business plan. It will likely include:

- Details of when, how, and why you started your business

- Your company mission statements

- High-level financial information about your business

- An explanation of how funding will help your business

Depending on whether you’re a startup or an established business, you may use this section to focus on your growth strategy or your past successes.

Company Description

Use this section to delve deeper into your company’s offerings, core principles, legal structure, and leadership. Your company description should also include your unique value proposition . Describe your company’s unique strengths that will ensure your success.

Products & Services

This section should detail the products and/or services your company provides. Make clear the problem that your offerings solve. Include information such as:

- Information on your raw materials and production process (if applicable)

- Profit margins

- Whether you have or plan to file patents or copyrights

Market Analysis

Use this section to demonstrate your understanding of your overall industry and the specific markets you serve, including market trends, competitors, and the demographics of your target customers. Some companies hire a consultant or agency to perform the research for the market analysis section.

Marketing & Sales Plan

Building off your market analysis, how will you market to your target customers and beat your competitors? How will you sell to them and distribute your product? What are your sales goals and projections? Provide these details in this section.

Organization & Management

Use this section to include your organizational and leadership structure, ideally including an organizational flowchart. Also include job descriptions, qualifications, and years of experience to demonstrate why your team is capable of delivering on your company goals and is worthy of investment.

Operational Strategy

This section is used to describe your day-to-day operational processes, including information about your location, facility, equipment, inventory, and daily production. If you have a service-based business, this section may focus more on your team’s daily activities and how they contribute to long-term goals.

Financial Outlook

This section should tell lenders how much you spend and how much you make in profits. Include up to five years of data if possible, including financial documents such as:

- Income statements

- Cash flow statements

- Balance sheets

- Capital expenditure budgets

- Sales forecasts

- Projected income statements

- Information on any collateral you have to secure the loan

Depending on how much financial documentation you have, you might refer to specific documents in this section and indicate that the full documents can be found in the Appendix section.

Though startups may not have all of this data, you can make projections based on monthly or quarterly data and industry averages.

Funding Request

Now that you’ve laid out your expenses and financial projections, it’s time to make your case for a loan. Be clear about how much money you need, how you will spend it, and how you will repay the loan. Be as detailed as possible.

In the Appendix, include any supporting documents, such as financial documents referred to in the Financial Outlook section. Some other types of documents you might include in this section are:

- Business licenses or permits

- Credit reports

- Product photos

- Marketing materials

- Letter of intent to purchase business

If you know what lenders are looking for in a business plan for a loan, you will increase your chances of approval. Learn the five things lenders want to see in your business plan, followed by five tips to create a loan-worthy business plan.

The 5 Cs Of Credit

The Five Cs of Credit is a phrase that summarizes what lenders look for when deciding whether to extend a loan to a business. Lenders will, accordingly, look for the five Cs when reviewing the business plan in your loan application. The five Cs are:

- Character: Your knowledge, experience, and creditworthiness

- Capacity: Your ability to repay the loan

- Capital: How much you have already invested in your business

- Conditions: Your market viability, considering your industry as well as overall economic conditions

- Collateral: Assets you can use to secure the loan

5 Business Plan Tips For Loan Approval

Besides emphasizing your “5 Cs,” there are a few other things you can do to make the best impression with your business plan to increase your chances of securing funding.

- Avoid Industry Jargon: Use plain English rather than industry terminology that the lender might not be familiar with. Remember that the loan underwriter may not have deep knowledge of your specific industry.

- Show Cash Flow: Cash flow is one of the most important factors that determine loan eligibility. You can even get a loan with bad credit as long as your cash flow is sufficiently high. The more insight you can provide into your past, current, and future cash flow, the better.

- Show Your Investment: Before extending a loan, the lender will want to see that you have already invested some of your own resources, such as personal savings, into your business. Be sure to include documentation that demonstrates your investment.

- Enlist Help: You will likely need some professional assistance in creating your business plan, whether that means hiring a writer, an industry consultant, or both. At the very least, you should have a third party review your business plan before you submit it as part of a loan application.

- Revise Your Plan As Needed: If this is the first time you’ve taken a close look at your business strategy and financials, you will surely learn some things about your business while creating your plan. For example, you may realize you cannot afford a business loan as large as you planned to ask for. Rather than trying to justify the number you started with, it’s better to modify your funding request (and other aspects of your plan) to align with your financial reality.

It’s easy to find templates and examples of business plans online. Though you may not want to copy and paste from a template verbatim, these samples provide a starting point and show you different ways a business plan can be structured. Here are a few to start with:

- Business plan template for a startup (from SCORE)

- Business plan template for traditional businesses (from the SBA)

- Business plan template for retail or eCommerce (from Shopify; requires email address)

These tools and resources can help you create a solid business plan for a loan. While some free business plan creation tools are available online, you will have to pay for some options.

SBA Business Plan Resources (Free)

The SBA has a great resource in its online learning center that includes business plan worksheets . In addition to business plan templates, the SBA also helps you connect to free local business counselors who may be able to help you with your business plan.

Business Plan Software ($)

If you need extra help creating a business plan and don’t mind spending a little bit of money, consider business plan creation software. For example, LivePlan ($20/month) is business plan software that connects with QuickBooks to import your financial data to your plan.

Business Plan Writer/Consultant ($$$)

If you’re willing to invest more heavily into your business plan, consider hiring a writer or consultant that specializes in creating business plans. This option costs anywhere from $2,000 to $20,000, with the lower end of that scale typically including only basic writing services and the higher end representing a specialized industry consultant agency.

While it’s helpful to know how to write a business plan for a loan, you can always hire someone to help you draft the plan if the task is too daunting. A business plan is a worthwhile investment no matter what type of business you have or whether you are currently trying to secure business funding. Even if you don’t need a loan right now, it’s important to maintain an updated business plan to serve as a guide for your own business decisions.

Was your loan denied because of your business plan (or another reason)? Learn what to do if your business loan was denied .

- Latest Posts

Shannon Vissers

@shannonvissers.

Latest posts by Shannon Vissers ( see all )

- Quiz: Find Your Perfect Credit Card Processing Match - August 26, 2024

- CardX by Stax Review - June 26, 2024

- Next-Day Funding Merchant Services - November 20, 2023

- 8 Best Merchant Account Providers For Small Business In 2024 - July 20, 2023

- How To Write A Business Plan For A Loan - July 12, 2023

We Want Your Feedback

Let us know how well the content on this page solved your problem today. All feedback, positive or negative, helps us to improve the way we help small businesses.

Guide To Business Loan Rates & Fees

Debt-To-Income Ratio: How To Calculate & Lower Your DTI

How To Calculate Business Loan Payments

Best Short-Term Loans For Small Businesses In 2024

" * " indicates required fields

Want to help shape the future of the Merchant Maverick website? Join our testing and survey community!

By providing feedback on how we can improve, you can earn gift cards and get early access to new features.

We Want Your Feedback!

Help us to improve by providing some feedback on your experience today.

Step 1 of 6

The vendors that appear on this list were chosen by subject matter experts on the basis of product quality, wide usage and availability, and positive reputation.

Merchant Maverick’s ratings are editorial in nature, and are not aggregated from user reviews. Each staff reviewer at Merchant Maverick is a subject matter expert with experience researching, testing, and evaluating small business software and services. The rating of this company or service is based on the author’s expert opinion and analysis of the product, and assessed and seconded by another subject matter expert on staff before publication. Merchant Maverick’s ratings are not influenced by affiliate partnerships.

Our unbiased reviews and content are supported in part by affiliate partnerships, and we adhere to strict guidelines to preserve editorial integrity. The editorial content on this page is not provided by any of the companies mentioned and has not been reviewed, approved or otherwise endorsed by any of these entities. Opinions expressed here are author’s alone.

Never show me any popup offer again.

Maverick Newsletter Signup 📬

- Checking/Money Market Accounts

Savings Accounts

- Retirement Accounts

- Online & Mobile Banking

- Loan Payments

- eStatements & Services

- Financial Education

Treasury Management

Checking accounts.

- Correspondent Banking

- Lockbox and Payment Processing

- Merchant Card Services

- Payment Options

Customer Success Stories

- Sectors We Serve

- Press Releases

- Publications

- 2023 Co-op Innovation Awards

- Community Impact

- Working at NCB

- Co-op Housing, Condo and HOA

- Credit Unions

- Personal & Small Business

- Personal Online Loan Payments

- Treasury 24/7

- Lockbox Services

- Investors Only

You are about to leave the website of National Cooperative Bank and view the content of an external website.

We provide links to external websites for convenience. National Cooperative Bank does not endorse and is not responsible for their content, links, privacy or securities policies.

Click OK to proceed, click Cancel to stay on this page

Sectors we Serve

Banking Solutions For Small Businesses

Our small business focus reflects our cooperative mission, serving independent retailers, purchasing co-ops and worker-owned co-ops nationwide.

Cooperative Solutions

Small businesses are the foundation of a strong community and create jobs and fuel local economy. We are committed to helping small businesses thrive and compete in today’s marketplace. Our small business focus reflects our cooperative mission, serving independent retailers, purchasing co-ops and worker-owned co-ops nationwide. We provide an array of banking solutions to help your business grow and compete with the big box chains. Whether your business is to looking to expand or renovate, NCB has banking solutions to help you meet the challenges of business ownership.

Products and Services

Save time and improve your cash flow operations with NCB’s treasury management solutions- built for small business retailers to large property management customers.

NCB’s business checking accounts are optimal for businesses and nonprofits of all shapes and sizes.

Maximize your returns with NCB’s competitive savings product including CD’s and MMDA accounts.

Commercial Loans

We offer flexible business loans and working capital lines of credit at competitive interest rates to meet your business needs.

Commercial Real Estate Loans

NCB provides first mortgages, second mortgages and lines of credit to commercial real estate properties across the country including housing cooperatives, multifamily and other commercial property types.

As a Preferred SBA Lender, NCB offers the SBA 7 (s) and SBA 504 loan programs to help independent businesses grow and succeed.

Get Started

Applications & forms.

Business Loan Application

Cooperative Business Loan Application

Personal Financial Statement

Business Location Profile

800.955.9622

2011 Crystal Drive, Suite 800 Arlington, VA 22202

- Mobile Privacy Policy

- Terms of Service

- Account Terms, Features, Notices and Disclosures

- Accessibility

- Community Reinvestment Act Public File

©2024 National Cooperative Bank. All Rights Reserved. NCB NMLS# 422343. Banking products and services provided by National Cooperative Bank, N.A. Member FDIC. We provide links to external websites for convenience. National Cooperative Bank does not endorse and is not responsible for their content, links, privacy or security policies. Privacy Policy

- Mar 30, 2023

The Ultimate Guide to Writing a Business Plan for a Loan: A Step-by-Step Walk-Through

The Ultimate Guide to Writing a Business Plan for a Loan: A Step-by-Step Walkthrough

As a business plan specialist and expert business planner, I'm here to guide you through the process of writing a comprehensive business plan for securing a loan. Whether you're a start-up or an established business looking to expand, a well-crafted business plan is essential for impressing potential lenders and securing the funding you need.

In this extensive, 5,000-word article, I'll cover everything you need to know about creating a top-notch business plan that will boost your chances of loan approval. We'll go through each section in detail, providing you with practical examples and tips to optimize your plan for success. So, let's get started!

Executive Summary

The executive summary is the first and most critical section of your business plan. It's a brief overview of your entire plan, highlighting the key points and giving readers an insight into your business.

Key elements to include in your executive summary:

Business concept: Briefly explain your business idea, the products or services you plan to offer, and the target market.

Company overview: Provide essential information about your company, including its legal structure, location, and mission statement.

Management team: Showcase the expertise and experience of your management team, emphasizing their ability to lead the business.

Market opportunity: Describe the market demand, trends, and target audience, highlighting the opportunity for your business to succeed.

Financial highlights: Summarize your financial projections, including sales, profits, and cash flow.

Loan purpose: Clearly state the purpose of the loan and the amount you're seeking.

Remember, the executive summary is often the first thing lenders read, so make it engaging and informative to grab their attention.

Company Description

The company description section is where you provide a more in-depth look at your business. It should give readers a clear understanding of your company's purpose, goals, and competitive advantages.

Key elements to include in your company description:

Business history: If your company has an existing history, briefly describe its origins and milestones achieved.

Mission statement: Articulate the purpose of your company and the value you aim to provide to customers.

Objectives: Outline the specific goals you want to achieve with your business, both short-term and long-term.

Products and services: Provide a detailed description of the products or services you plan to offer, emphasizing the benefits they provide to customers.

Target market: Identify your target audience, specifying their demographics, psychographics, and buying habits.

Competitive advantage: Explain what sets your business apart from the competition and how you plan to maintain this edge.

Market Analysis

The market analysis section demonstrates your understanding of the industry, market, and competition. It's crucial to show lenders that you've done your homework and have a comprehensive understanding of the market landscape.

Key elements to include in your market analysis:

Industry overview: Provide a high-level view of your industry, including its size, growth trends, and key players.

Market segmentation: Break down your target market into smaller segments, identifying their unique needs and preferences.

Target market characteristics: Describe the specific characteristics of your target market, such as demographics, psychographics, and geographic location.

Market demand: Present evidence of market demand, using data on customer needs, market trends, and buying behaviors.

Competitor analysis: Evaluate your main competitors, analyzing their strengths, weaknesses, and market share.

SWOT analysis: Conduct a SWOT analysis (Strengths, Weaknesses, Opportunities, and Threats) to assess your business's position in the market.

Marketing and Sales Strategy

In this section, outline your marketing and sales strategy to show lenders how you plan to attract and retain customers, as well as generate revenue. A well-defined marketing and sales strategy is crucial to demonstrate that you have a clear plan for growth and profitability.

Key elements to include in your marketing and sales strategy:

Marketing objectives: Define your marketing goals, such as brand awareness, lead generation, or customer retention.

Target audience: Reiterate your target market, emphasizing their needs and preferences.

Unique selling proposition (USP): Highlight your USP, the main reason customers should choose your products or services over the competition.

Marketing channels: Identify the marketing channels you plan to use, such as social media, email, content marketing, or paid advertising. Explain the rationale behind your choice of channels and how they align with your target audience.

Sales process: Describe your sales process, from lead generation to closing deals. Include details on your sales team structure, training, and compensation plans.

Key performance indicators (KPIs): List the KPIs you'll use to measure the success of your marketing and sales efforts, such as conversion rates, average deal size, or customer lifetime value.

Operations Plan

The operations plan section details the day-to-day activities required to run your business. It shows lenders that you have a clear understanding of the operational aspects of your company and the resources needed to support your growth.

Key elements to include in your operations plan:

Facilities: Describe your business's physical location, including its size, layout, and any equipment or machinery required.

Production process: If applicable, detail your production process, including the steps involved, quality control measures, and production capacity.

Supply chain: Outline your supply chain, identifying key suppliers, procurement processes, and inventory management practices.

Staffing: Explain your staffing requirements, including the roles, responsibilities, and qualifications of each team member.

Management structure: Provide an organizational chart, showcasing your company's management structure and reporting lines.

Legal and regulatory requirements: Identify any relevant legal or regulatory requirements, such as licenses, permits, or certifications needed to operate your business.

Financial Plan

The financial plan is arguably the most crucial section of your business plan when applying for a loan. It demonstrates your ability to manage finances, make informed decisions, and, ultimately, repay the loan.

Key elements to include in your financial plan:

Revenue projections: Estimate your future sales, breaking them down by product or service category and showing growth rates over time.

Expense projections: Forecast your expenses, including fixed costs (e.g., rent, utilities) and variable costs (e.g., marketing, salaries).