How to write a balance sheet for a business plan

Table of Contents

What is a balance sheet?

Elements of a balance sheet, liabilities, how to write a balance sheet, manage your business finances with countingup.

A balance sheet is one of three major financial statements that should be in a business plan – the other two being an income statement and cash flow statement .

Writing a balance sheet is an essential skill for any business owner. And while business accounting can seem a little daunting at first, it’s actually fairly simple.

To help you write the perfect balance sheet for your business plan, this guide covers everything you need to know, including:

- What are assets?

- What are liabilities?

- What is equity?

A balance sheet is a financial statement that shows a business’ “book value”, or the value of a company after all of its debts are paid.

For those inside the business, it provides valuable financial insights, allowing the owners to assess their current financial situation and plan for the future.

For external investors, a balance sheet lets them know whether it’s a worthwhile investment.

Putting a balance sheet together isn’t all that difficult. You just need to know the value of three things:

- Owner’s equity

Once you know these three figures, there’s just a little bit of maths – nothing too scary though.

Assets are items or resources that have financial value. They might be physical items, machinery and vehicles, or they could be intangible items, like copyrights or brand identity .

Assets are separated into two groups based on how quickly you can turn them into cash. There are current assets and fixed assets.

Current assets are things that are fairly simple to value and sell, such as:

- Stock and inventory

- Cash in the bank

- Money owed to you (through unpaid invoices )

- Customer deposits

- Office furniture, equipment or supplies

- Phones or laptops

- Even relatively trivial items like a coffee machine or pool table

Fixed assets are valuable items that take much longer to sell, such as:

- Property or buildings

- Specialised equipment for your business operations

- Investments

- Vehicles

On your balance sheet, the asset column is the simplest. All you need to do is list each item your business owns, along with their individual values, in a separate column. Then, add up the values to get a total at the bottom.

Liabilities are the funds that you owe to other people, banks, or businesses. They can be:

- A business loan (the total, not the monthly payment amount)

- A mortgage or rent payment on a property

- Supplier contracts you owe

- Your accounts payable total

- Other financial obligations, such as paying wages or freelancers for support

- Taxes you’ll owe to HMRC

List these in the same way you did with your assets – on a spreadsheet with their values in a separate column.

When you know the value of your assets and liabilities, working your equity is simple – it’s just the total value of your assets, minus the total value of your liabilities.

Record the owner’s equity in the same column as your liabilities. When you add them all up, it should be the same value as your assets.

After you’ve totalled up your assets, liabilities, and owner’s equity, all that’s left to do is fill in your balance sheet.

Using a spreadsheet, record your assets on the left and your liabilities and owner’s equity on the right.

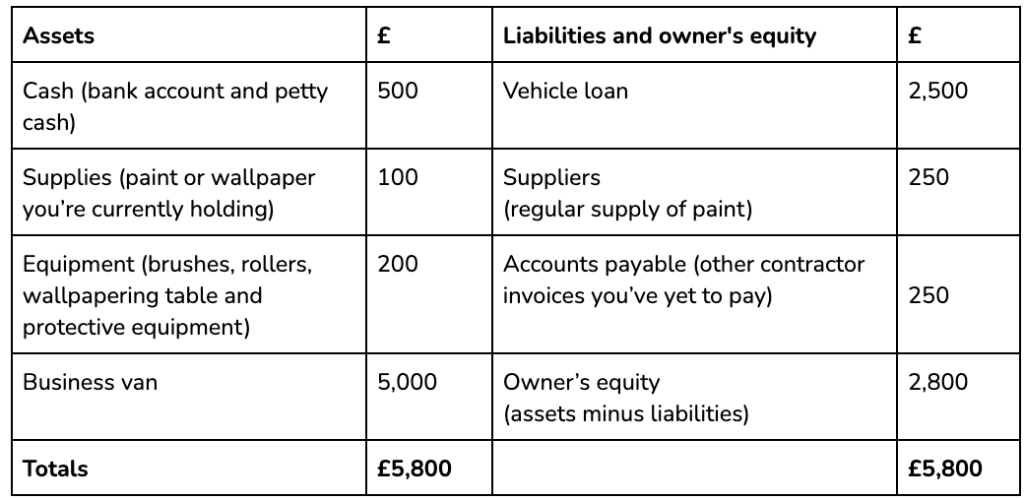

For example, here’s what a balance sheet might look like for a painter and decorator:

If you’ve recorded everything correctly, both sides should have the same total. Whenever you make a change, the balance sheet will change, but it should still be balanced.

For example, let’s say our painter and decorator sold their equipment. In that case, they’d lose an asset worth £200, but they’d also gain £200 in cash, so the asset total would stay the same.

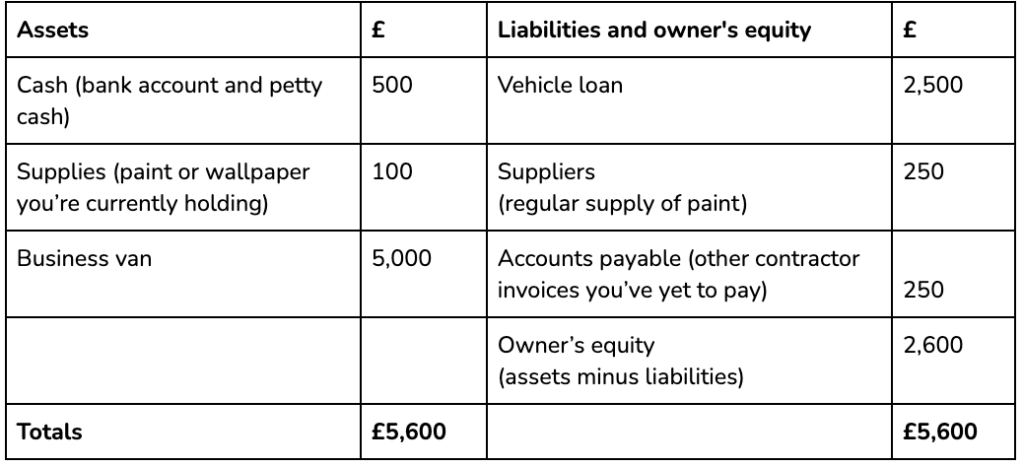

Alternatively, let’s say they lost the equipment altogether and got no money for it. In that case, they’d lose £200, leaving their asset total at £5,600. Then, they’d have to adjust the other side, so it remains balanced, like this:

If your two totals are not balanced, it’s most likely for one of these reasons:

- Incomplete or missing information

- Incorrect data entry

- A mistake in exchange rates

- And inventory miscount

Basically, if things don’t look right, try not to panic. It’s normally a simple mistake, so go over the figures again and you’ll find the culprit.

The trickiest part of writing a balance sheet for a business plan is accurately recording financial information.

With the Countingup business current account, you’ll have access to a digital record of all your transactions in one simple app, giving you all the financial information you’ll need for a business plan.

Start your three-month free trial today.

Find out more here .

- Counting Up on Facebook

- Counting Up on Twitter

- Counting Up on LinkedIn

Related Resources

Business insurance from superscript.

We’re partnered with insurance experts, Superscript to provide you with small business insurance.

How to register a company in the UK

There are over five million companies registered in the UK and 500,000 new

How to set up a TikTok shop (2024)

TikTok can be an excellent platform for growing a business, big or small.

Best Side Hustle Ideas To Make Extra Money In 2024 (UK Edition)

Looking to start a new career? Or maybe you’re looking to embrace your

How to throw a launch party for a new business

So your business is all set up, what next? A launch party can

How to set sales goals

Want to make manageable and achievable sales goals for your business? Find out

10 key tips to starting a business in the UK

10 things you need to know before starting a business in the UK

How to set up your business: Sole trader or limited company

If you’ve just started a business, you’ll likely be faced with the early

How to register as a sole trader

Running a small business and considering whether to register as a sole trader?

How to open a Barclays business account

When starting a new business, one of the first things you need to

6 examples of objectives for a small business plan

Your new company’s business plan is a crucial part of your success, as

How to start a successful business during a recession

Starting a business during a recession may sound like madness, but some big

- Business Essentials

- Leadership & Management

- Credential of Leadership, Impact, and Management in Business (CLIMB)

- Entrepreneurship & Innovation

- Digital Transformation

- Finance & Accounting

- Business in Society

- For Organizations

- Support Portal

- Media Coverage

- Founding Donors

- Leadership Team

- Harvard Business School →

- HBS Online →

- Business Insights →

Business Insights

Harvard Business School Online's Business Insights Blog provides the career insights you need to achieve your goals and gain confidence in your business skills.

- Career Development

- Communication

- Decision-Making

- Earning Your MBA

- Negotiation

- News & Events

- Productivity

- Staff Spotlight

- Student Profiles

- Work-Life Balance

- AI Essentials for Business

- Alternative Investments

- Business Analytics

- Business Strategy

- Business and Climate Change

- Creating Brand Value

- Design Thinking and Innovation

- Digital Marketing Strategy

- Disruptive Strategy

- Economics for Managers

- Entrepreneurship Essentials

- Financial Accounting

- Global Business

- Launching Tech Ventures

- Leadership Principles

- Leadership, Ethics, and Corporate Accountability

- Leading Change and Organizational Renewal

- Leading with Finance

- Management Essentials

- Negotiation Mastery

- Organizational Leadership

- Power and Influence for Positive Impact

- Strategy Execution

- Sustainable Business Strategy

- Sustainable Investing

- Winning with Digital Platforms

How to Prepare a Balance Sheet: 5 Steps for Beginners

- 10 Sep 2019

A company’s balance sheet is one of the most important financial statements it produces—typically on a quarterly or even monthly basis (depending on the frequency of reporting).

Depicting your total assets, liabilities, and net worth, this document offers a quick look into your financial health and can help inform lenders, investors, or stakeholders about your business. Based on its results, it can also provide you key insights to make important financial decisions.

When paired with cash flow statements and income statements , balance sheets can help provide a complete picture of your organization’s finances for a specific period. By determining the financial status of your organization, essential partners have an informative blueprint of your company’s potential and profitability.

Have you found yourself in the position of needing to prepare a balance sheet? Here's what you need to know to understand how balance sheets work and what makes them a business fundamental , as well as steps you can take to create a basic balance sheet for your organization.

Access your free e-book today.

What Is a Balance Sheet?

A balance sheet is a financial statement that communicates the “book value” of an organization, as calculated by subtracting all of the company’s liabilities and shareholder equity from its total assets.

A balance sheet offers internal and external analysts a snapshot of how a company is performing in the current period, how it performed during the previous period, and how it expects to perform in the immediate future. This makes balance sheets an essential tool for individual and institutional investors, as well as key stakeholders within an organization and any outside regulators who need to see the status of an organization during specific periods of time.

The Balance Sheet Format

Most balance sheet formats are arranged according to this equation : Assets = Liabilities + Shareholders’ Equity

The equation above includes three broad buckets, or categories, of value which must be accounted for:

An asset is anything a company owns which holds some amount of quantifiable value, meaning that it could be liquidated and turned to cash. They're the goods and resources owned by the company.

Assets can be further broken down into current assets and non-current assets:

- Current assets —or short-term assets—are typically what a company expects to convert into cash within a year’s time, such as cash and cash equivalents, prepaid expenses, inventory, marketable securities, and accounts receivable.

- Non-current assets —also called fixed or long-term assets—are investments that a company does not expect to convert into cash in the short term, such as land, equipment, patents, trademarks, and intellectual property.

Related: 6 Ways Understanding Finance Can Help You Excel Professionally

2. Liabilities

A liability is anything a company or organization owes to a debtor. This may refer to payroll expenses, rent and utility payments, debt payments, money owed to suppliers, taxes, or bonds payable.

As with assets, liabilities can be classified as either current liabilities or non-current liabilities:

- Current or short-term liabilities are typically those due within one year, which may include accounts payable and other accrued expenses.

- Non-current or long term liabilities are typically those that a company doesn’t expect to repay within one year. They're usually long-term obligations, such as leases, bonds payable, or loans.

3. Shareholders’ Equity

Shareholders’ equity refers generally to the net worth of a company, and reflects the amount of money that would be left over if all assets were sold and liabilities paid. Shareholders’ equity belongs to the shareholders, whether they're private or public owners.

Just as assets must equal liabilities plus shareholders’ equity, shareholders’ equity can be depicted by this equation: Shareholders’ Equity = Assets - Liabilities

Does a Balance Sheet Always Balance?

A balance sheet should always balance. The name itself comes from the fact that a company’s assets will equal its liabilities plus any shareholders’ equity that has been issued. If you find that your balance sheet is not truly balancing, it may be caused by one of these culprits:

- Incomplete or misplaced data

- Incorrectly entered transactions

- Errors in currency exchange rates

- Errors in inventory

- Incorrect equity calculations

- Miscalculated loan amortization or depreciation

How to Prepare a Basic Balance Sheet

Here are five steps you can follow to create a basic balance sheet for your organization. Even if some or all of the process is automated through the use of an accounting system or software, understanding how a balance sheet is prepared will enable you to spot potential errors so that they can be resolved before they cause lasting damage.

1. Determine the Reporting Date and Period

A balance sheet is meant to depict the total assets, liabilities, and shareholders’ equity of a company on a specific date, typically referred to as the reporting date. Often, the reporting date will be the final day of the accounting period .

How Often Is a Balance Sheet Prepared?

Companies, especially publicly traded ones, prepare their balance sheet reports on a quarterly basis. When this is the case, the reporting date usually falls on the final day of the quarter. For companies that operate on a calendar year, those dates are:

- Q1: March 31

- Q2: June 30

- Q3: September 30

- Q4: December 31

Companies that report on an annual basis will often use December 31st as their reporting date, though they can choose any date.

It's not uncommon for a balance sheet to take a few weeks to prepare after the reporting period has ended.

Related: 10 Important Business Skills Every Professional Needs

2. Identify Your Assets

After you’ve identified your reporting date and period, you’ll need to tally your assets as of that date.

Typically, a balance sheet will list assets in two ways: As individual line items and then as total assets. Splitting assets into different line items will make it easier for analysts to understand exactly what your assets are and where they came from; tallying them together will be required for final analysis.

Assets will often be split into the following line items:

- Current Assets:

- Cash and cash equivalents

- Short-term marketable securities

- Accounts receivable

- Other current assets

- Non-current Assets:

- Long-term marketable securities

- Intangible assets

- Other non-current assets

Current and non-current assets should both be subtotaled, and then totaled together.

3. Identify Your Liabilities

Similarly, you will need to identify your liabilities. Again, these should be organized into both line items and totals, as below:

- Current Liabilities:

- Accounts payable

- Accrued expenses

- Deferred revenue

- Current portion of long-term debt

- Other current liabilities

- Non-Current Liabilities:

- Deferred revenue (non-current)

- Long-term lease obligations

- Long-term debt

- Other non-current liabilities

As with assets, these should be both subtotaled and then totaled together.

4. Calculate Shareholders’ Equity

If a company or organization is privately held by a single owner, then shareholders’ equity will be relatively straightforward. If it’s publicly held, this calculation may become more complicated depending on the various types of stock issued.

Common line items found in this section of the balance sheet include:

- Common stock

- Preferred stock

- Treasury stock

- Retained earnings

5. Add Total Liabilities to Total Shareholders’ Equity and Compare to Assets

To ensure the balance sheet is balanced, it will be necessary to compare total assets against total liabilities plus equity. To do this, you’ll need to add liabilities and shareholders’ equity together.

Example of a Finished Balance Sheet

It's important to note that this balance sheet example is formatted according to International Financial Reporting Standards (IFRS), which companies outside the United States follow. If this balance sheet were from a US company, it would adhere to Generally Accepted Accounting Principles (GAAP).

Related: GAAP vs. IFRS: What Are the Key Differences and Which Should You Use?

If you’ve found that your balance sheet doesn't balance, there's likely a problem with some of the accounting data you've relied on. Double check that all of your entries are correct and accurate. You may have omitted or duplicated assets, liabilities, or equity, or miscalculated your totals.

The Purpose of a Balance Sheet

Balance sheets are one of the most critical financial statements , offering a quick snapshot of the financial health of a company. Learning how to generate them and troubleshoot issues when they don’t balance is an invaluable financial accounting skill that can help you become an indispensable member of your organization.

Do you want to learn more about what's behind the numbers on financial statements? Explore our finance and accounting courses to find out how you can develop an intuitive knowledge of financial principles and statements to unlock critical insights into performance and potential.

This post was updated on May 9, 2024. It was originally published on September 10, 2019.

About the Author

What Is a Balance Sheet? Definition, Formulas, and Example

Trevor Betenson

10 min. read

Updated May 2, 2024

Business financial statements consist of three main components: the income statement , statement of cash flows , and balance sheet. The balance sheet is often the most misunderstood of these components—but also extremely beneficial if you understand how to use it.

Check out our free downloadable Balance Sheet Template for more, and keep reading to learn the different elements of a balance sheet, and why they matter.

- What is a balance sheet?

The balance sheet provides a snapshot of the overall financial condition of your company at a specific point in time. It lists all of the company’s assets, liabilities, and owner’s equity in one simple document.

A balance sheet always has to balance—hence the name. Assets are on one side of the equation, and liabilities plus owner’s equity are on the other side.

Assets = Liabilities + Equity

- What is the purpose of the balance sheet?

Put simply, a balance sheet shows what a company owns (assets), what it owes (liabilities), and how much owners and shareholders have invested (equity).

Including a balance sheet in your business plan is an essential part of your financial forecast , alongside the income statement and cash flow statement.

These statements give anyone looking over the numbers a solid idea of the overall state of the business financially. In the case of the balance sheet in particular, what it’s telling you is whether or not you’re in debt, and how much your assets are worth. This information is critical to managing your business and the creation of a business plan.

The balance sheet includes spending and income that isn’t in the income statement (also called a profit and loss statement). For example, the money you spend to repay a loan or buy new assets doesn’t show up in the income statement. And the money you take in as a new loan or a new investment doesn’t show up in the income statement either. The money you are waiting to receive from customers’ outstanding invoices shows up in the balance sheet, not the income statement.

Among other things, your balance sheet can be used to determine your company’s net worth. By subtracting liabilities from assets, you can determine your company’s net worth at any given point in time.

- Key components of the balance sheet

Typically, a balance sheet is divided into three main parts: Assets, liabilities, and owner’s equity.

Assets on a balance sheet or typically organized from top to bottom based on how easily the asset can be converted into cash. This is called “liquidity.” The most “liquid” assets are at the top of the list and the least liquid are at the bottom of the list.

Brought to you by

Create a professional business plan

Using ai and step-by-step instructions.

Secure funding

Validate ideas

Build a strategy

In the context of a balance sheet, cash means the money you currently have on hand. In business planning, the term “cash” represents the bank or checking account balance for the business, also sometimes referred to as “cash and cash equivalents” or “CCE.”

A cash equivalent is an asset that is liquid and can be converted to cash immediately, like a money market account or a treasury bill.

Accounts receivable

Accounts receivable is money people are supposed to pay you, but that you have not actually received yet (hence the “receivables”).

Usually, this money is sales on credit, often from business-to-business (or “B2B”) sales, where your business has invoiced a customer but has not received payment yet.

Inventory includes the value of all of the finished goods and ready materials that your business has on hand but hasn’t sold yet.

Current assets

Current assets are those that can be converted to cash within one year or less. Cash, accounts receivable, and inventory are all current assets, and these amounts accumulated are sometimes referenced on a balance sheet as “total current assets.”

Long-term assets

Long-term assets are also referred to as “fixed assets” and include things that will have a long-standing value, such as land or equipment. Long-term assets typically cannot be converted to cash quickly.

Accumulated depreciation

Accumulated depreciation reduces the value of assets over time. For example, if a business purchases a car, the car will lose value as time goes on.

Total long-term assets

Total long-term assets is used to describe long-term assets plus depreciation on a balance sheet.

Liabilities

Like assets, liabilities are ordered by how quickly a business needs to pay them off. Current liabilities are typically due within one year. Long-term liabilities are due at any point after one year.

Accounts payable

Accounts payable is the money that your business owes to other vendors, the other side of the coin to “accounts receivable.” Your accounts payable number is the regular bills that your business is expected to pay.

Pay attention to whether this number is exceedingly high, especially if your business doesn’t have enough to cover it.

Sales taxes payable

This only applies to businesses that don’t pay sales tax right away, for example, a business that pays its sales tax each quarter. That might not be your business, so if it doesn’t apply, skip it.

Short-term debt

This is debt that you have to pay back within a year—usually any short-term loan. This can also be referred to on a balance sheet as a line item called current liabilities or short-term loans. Your related interest expenses don’t go here or anywhere on the balance sheet; those should be included in the income statement.

Total current liabilities

The above numbers added together are considered the current liabilities of a business, meaning that the business is responsible for paying them within one year.

Long-term debt

These are the financial obligations that it takes more than a year to pay back. This is often a hefty number, and it doesn’t include interest. For example, this number reflects long-term loans on things like buildings or expensive pieces of equipment. It should be decreasing over time as the business makes payments and lowers the principal amount of the loan.

Total liabilities

Everything listed above that you have to pay out or back is added together.

This is the sum of all shareholder money invested in the business and accumulated business profits. Owner’s equity includes common stock, retained earnings, and paid-in-capital.

Paid-in capital

Money is paid into the company as investments. This is not to be confused with the par value or market value of stocks. This is actual money paid into the company as equity investments by owners.

Retained earnings

Earnings (or losses) that have been reinvested into the company, that have not been paid out as dividends to the owners. When retained earnings are negative, the company has accumulated losses. This can also be referred to as “shareholder’s equity.”

This doesn’t apply to all legal structures for a business; if you are a pass-through tax entity , then all profits or losses will be passed on to owners, and your balance sheet should reflect that.

Net earnings

This is an important number—the higher it is, the more profitable your company is. This line item can also be called income or net profit. Earnings are the proverbial “bottom line”: sales less costs of sales and expenses.

Total owner’s equity

Equity means business ownership, also called capital. Equity can be calculated as the difference between assets and liabilities. This can also be referred to as “shareholder’s equity” or “stockholder’s equity.”

Total liabilities and equity

This is the final equation I mentioned at the beginning of this post, assets = liabilities + equity.

- How to use the balance sheet

Your balance sheet can provide a wealth of useful information to help improve financial management. For example, you can determine your company’s net worth by subtracting your balance sheet liabilities from your assets, as noted above.

Overall, the balance sheet gives you insights into the health of your business. It’s a snapshot of what you have (assets) and what you owe (liabilities). Keeping tabs on these numbers will help you understand your financial position and if you have enough cash to make further investments in your business.

Perhaps the most useful aspect of your balance sheet is its ability to alert you to upcoming cash shortages. After a highly profitable month or quarter, for example, business owners sometimes get lulled into a sense of financial complacency if they don’t consider the impact of upcoming expenses on their cash flow .

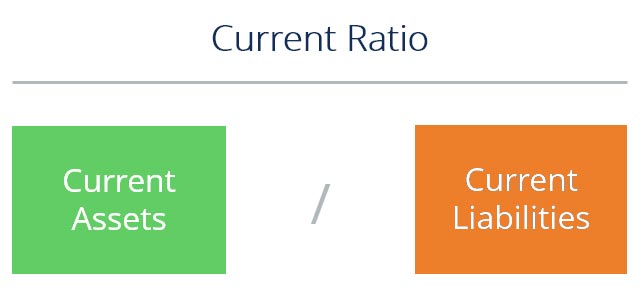

There are two easy-to-figure ratios that can be computed from the balance sheet to help determine whether your company will have sufficient cash flow to meet current financial obligations:

Current ratio

This measures liquidity to show whether your company has enough current (i.e., liquid) assets on hand to pay bills on-time and run operations effectively. It is expressed as the number of times current assets exceeds current liabilities.

The higher the current ratio, the better. A current ratio of 2:1 is generally considered acceptable for inventory-carrying businesses, although industry standards can vary widely. The acceptable current ratio for a retail business, for example, is different from that of a manufacturer.

Current ratio formula

Current Assets / Current Liabilities

Quick ratio

This ratio is similar to the current ratio but excludes inventory. A quick ratio of 1.5:1 is generally desirable for non-inventory-carrying businesses, but—just as with current ratios—desirable quick ratios differ from industry to industry.

Quick ratio formula

Current Assets – Inventory / Current Liabilities

Knowing your industry’s standards is an important part of evaluating your business’s balance sheet effectively.

- The limits of the balance sheet

Remember, the balance sheet alone doesn’t give you a complete view of your business finances. You’ll want to keep tabs on your profit & loss statement (income statement) and cash flow as well.

Your profit & loss statement will show you the sales you are making and your business expenses and calculates your profitability. This is crucial for understanding the core economics of your business and if you’re building a profitable business, or not.

Your cash flow forecast shows how cash is moving in and out of your business and can help you predict your future cash balances. Fast growth can reduce cash quickly, especially for businesses that carry inventory, so this is a crucial statement to pay attention to as well.

The three statements all work together to provide you with a complete picture of your business. The balance sheet also helps illustrate how cash and profits are very different things .

- Example of a balance sheet

Large businesses will have longer and more complex balance sheets for their businesses, sometimes having separate balance sheets for different segments or departments of their business. A small business balance sheet will be more straightforward and have fewer line items.

Here is a balance sheet from Apple, for example. You’ll see that it includes a complex stockholder’s equity section and several specifically itemized types of long-term assets and liabilities.

Apple’s balance sheet .

You’ll also notice that it says “Period Ending” at the top; this indicates that these numbers are reflective of the time up until the date listed at the top of the column. This terminology is used when you are reporting actual values, not creating a financial forecast for the future.

- Get familiar with your balance sheet

Most companies should update their balance once a month, or whenever lenders ask for an updated balance sheet. Today’s accounting software programs will create your balance sheet for you, but it’s up to you to enter accurate information into the program to generate useful data to work from.

The balance sheet can be an extremely useful financial tool for businesses that understand how to use it properly. If you’re not as familiar with your balance sheet as you’d like to be, now might be a good time to learn more about the workings of your balance sheet and how it can help improve financial management.

Create your balance sheet easily by downloading our Balance Sheet Template , and check out our full guide to write your financial plan.

Trevor is the CFO of Palo Alto Software, where he is responsible for leading the company’s accounting and finance efforts.

Table of Contents

Related Articles

5 Min. Read

9 Common Mistakes with Business Financial Projections

7 Min. Read

7 Financial Terms Small Business Owners Need to Know

3 Min. Read

What Is a Break-Even Analysis?

9 Min. Read

How to Create a Cash Flow Forecast

The LivePlan Newsletter

Become a smarter, more strategic entrepreneur.

Your first monthly newsetter will be delivered soon..

Unsubscribe anytime. Privacy policy .

The quickest way to turn a business idea into a business plan

Fill-in-the-blanks and automatic financials make it easy.

No thanks, I prefer writing 40-page documents.

Discover the world’s #1 plan building software

Business Plan Balance Sheet: Everything You Need to Know

Preparing a business plan balance sheet is an important part of starting your own business. 3 min read updated on September 19, 2022

Preparing a business plan balance sheet is an important part of starting your own business. The balance sheet serves as one of three crucial parts of the company's financials along with cash flow and the income statement. The basics of the balance sheet include a few straightforward parts:

- Company assets.

- Liabilities.

- Owner's equity.

The balance sheet will also include income and spending that isn't represented in the profit and loss statement. For example, it will show loan repayments and the purchase of new assets. Additionally, the money that is taken in as a new loan will not show up on the P & L either.

Accounts receivable, or the money you are waiting to receive from your customers, will show up as an asset on your balance sheet and as it is not yet reported as income on your P & L statement. A balance sheet is your business's representation of why your profits are not yet considered cash. It creates the broad financial picture of your business while the profit and loss statement will show the company's financial performance over a set length of time.

A balance sheet always has to balance. It will have assets on one side and liabilities and equity on the other. The basic formula that a balance sheet follows is Assets = Liabilities + Equity. In the end, it is the balance sheet that will show a company's net worth. To determine net worth at any given time, all you need to do is subtract the liabilities from the assets.

Balance sheets are used for planning and not accounting which is one of the principles of lean business planning. To get a useful cash flow projection, you will need to summarize the aggregate of the rows on the balance sheet. It is always important to look at a balance sheet as a tool to forecast your cash.

Components of a Balance Sheet

Just as one business will differ from another, so will the assets and liabilities of the business. Even though the titles will vary, the equation and goal remains the same. You will need to have your business assets equal your liabilities and equity .

The assets on your balance sheet will often be in order from the top to the bottom with how easy they can be converted to cash. This is called liquidity . Your most liquid assets will be on top and your least liquid on the bottom. Typically assets will be listed as follows:

- Cash — This is money currently on hands such as in checking and savings accounts. It can also include money market accounts that can be converted to cash quickly.

- Accounts Receivable — This represents money that is owed to you but has not actually been received yet. This is often credit that is extended to customers through invoicing.

- Inventory — This includes all the finished goods and materials that are ready at your place of business but has yet to be sold.

- Current Assets — These are assets that can be considered able to be converted into cash within a year or less. This includes all your cash, accounts receivable, and inventory which will all be grouped together as current assets.

- Long-Term Assets — These are fixed assets that have a long-standing value such as land and equipment. They cannot be converted to cash as quickly.

- Accumulated Depreciation — This is the value that your assets will be reduced over time due to depreciation.

- Long-Term Assets — This is the total of long-term assets plus depreciation.

Liabilities

Liabilities will be ordered for time it would take to pay them off, with current liabilities needing to be paid in a year or less and long-term liabilities longer than a year.

- Accounts Payable — This is the amount of money that your business will owe to vendors or for regular bills.

- Sales Tax Payable — If your sales tax is not paid right away, it will accrue in this account until payment is made.

- Short-Term Debt — This is usually short-term loans that will be repaid in less than a year.

- Total Current Liabilities — The total amount of debt that the business will need to pay back in a year.

- Long-Term Debt — This amount includes the financial responsibilities that will take more than a year to pay back.

If you need help with a business plan balance sheet, you can post your legal need on UpCounsel's marketplace. UpCounsel accepts only the top 5 percent of lawyers to its site. Lawyers on UpCounsel come from law schools such as Harvard Law and Yale Law and average 14 years of legal experience, including work with or on behalf of companies like Google, Menlo Ventures, and Airbnb.

Hire the top business lawyers and save up to 60% on legal fees

Content Approved by UpCounsel

- S Corp Balance Sheet

- How to Prepare Annual Report of a Company

- Are Patents Intangible Assets

- How to Evaluate a Company for Investment?

- What Is Liability Business - Everything You Need to Know

- Common Stock Asset or Liability

- Financial Plan Sample For Small Business

- How to Check Up on a Business

- Cash on Hand

- Personal Assets

Understanding a Balance Sheet (With Examples and Video)

Frances McInnis

Reviewed by

May 3, 2024

This article is Tax Professional approved

Balance sheets can help you see the big picture: the net worth of your small business, how much money you have, and where it’s kept. They’re also essential for getting investors, securing a loan , or selling your business.

So you definitely need to know your way around one. That’s where this guide comes in. We’ll walk you through balance sheets, one step at a time.

I am the text that will be copied.

What is a balance sheet?

The balance sheet is one of the three main financial statements , along with the income statement and cash flow statement .

While income statements and cash flow statements show your business’s activity over a period of time, a balance sheet gives a snapshot of your financials at a particular moment. It incorporates every journal entry since your company launched. Your balance sheet shows what your business owns (assets), what it owes (liabilities) , and what money is left over for the owners ( owner’s equity ).

Because it summarizes a business’s finances, the balance sheet is also sometimes called the statement of financial position. Companies usually prepare one at the end of a reporting period, such as a month, quarter, or year.

The purpose of a balance sheet

Because the balance sheet reflects every transaction since your company started, it reveals your business’s overall financial health. Investors, business owners, and accountants can use this information to give a book value to the business, but it can be used for so much more.

At a glance, you’ll know exactly how much money you’ve put in, or how much debt you’ve accumulated. Or you might compare current assets to current liabilities to make sure you’re able to meet upcoming payments.

The information in your company’s balance sheet can help you calculate key financial ratios, such as the debt-to-equity ratio, a metric which shows the ability of a business to pay for its debts with equity (should the need arise). Even more immediately applicable is the current ratio : current assets / current liabilities. This will tell you whether you have the ability to pay all your debts in the next 12 months.

You can also compare your latest balance sheet to previous ones to examine how your finances have changed over time. You’ll be able to see just how far you’ve come since day one.

A simple balance sheet template

You can download a simple balance sheet template here . You record the account name on the left side of the balance sheet and the cash value on the right.

What goes on a balance sheet

At a high level, a balance sheet works the same way across all business types. They are organized into three categories: assets, liabilities, and owner’s equity.

Let’s start with assets—the things your business owns that have a dollar value.

List your assets in order of liquidity , or how easily they can be turned into cash, sold or consumed. Bank accounts and other cash accounts should come first followed by fixed assets or tangible assets like buildings or equipment with a useful life longer than a year. Even intangible assets like intellectual properties, trademarks, and copyrights should be included. Anything you expect to convert into cash within a year are called current assets.

Current assets include:

- Money in a checking account

- Money in transit (money being transferred from another account)

- Accounts receivable (money owed to you by customers)

- Short-term investments

- Prepaid expenses

- Cash equivalents (currency, stocks, and bonds)

Long-term assets (or non-current assets), on the other hand, are things you don’t plan to convert to cash within a year.

Long-term assets include:

- Buildings and land

- Machinery and equipment (less accumulated depreciation )

- Intangible assets like patents, trademarks, copyrights, and goodwill (you would list the market value of what fair price a buyer might purchase these for)

- Long-term investments

Let’s say you own a vegan catering business called “Where’s the Beef”. As of December 31, your company assets are: money in a checking account, an unpaid invoice for a wedding you just catered, and cookware, dishes and utensils worth $900. Here’s how you’d list your assets on your balance sheet:

| ASSETS | |

|---|---|

| Bank account | $2,050 |

| Accounts receivable | $6,100 |

| Equipment | $900 |

| Total assets | $9,050 |

Liabilities

Next come your liabilities—your business’s financial obligations and debts.

List your liabilities by their due date. Just like assets, you’ll classify them as current liabilities (due within a year) and non-current liabilities (the due date is more than a year away). These are also known as short-term liabilities and long-term liabilities.

Your current liabilities might include:

- Accounts payable (what you owe suppliers for items you bought on credit)

- Wages you owe to employees for hours they’ve already worked

- Loans that you have to pay back within a year

- Credit card debt

And here are some non-current liabilities:

- Loans that you don’t have to pay back within a year

- Bonds your company has issued

Returning to our catering example, let’s say you haven’t yet paid the latest invoice from your tofu supplier. You also have a business loan, which isn’t due for another 18 months.

Here are Where’s the Beef’s liabilities:

| LIABILITIES | |

|---|---|

| Accounts payable | $150 |

| Long-term debt | $2,000 |

| Total liabilities | $2,150 |

Equity is money currently held by your company. This category is usually called “owner’s equity” for sole proprietorships and “stockholders’ equity” or “shareholders’ equity” for corporations. It shows what belongs to the business owners and the book value of their investments (like common stock, preferred stock, or bonds).

Owners’ equity includes:

- Capital (the amount of money invested into the business by the owners)

- Private or public stock

- Retained earnings (all your revenue minus all your expenses and distributions since launch)

Equity can also drop when an owner draws money out of the company to pay themself, or when a corporation issues dividends to shareholders.

For Where’s the Beef, let’s say you invested $2,500 to launch the business last year, and another $2,500 this year. You’ve also taken $9,000 out of the business to pay yourself and you’ve left some profit in the bank.

Here’s a summary of Where’s the Beef’s equity:

| EQUITY | |

|---|---|

| Capital | $5,000 |

| Retained earnings | $10,900 |

| Drawing | -$9,000 |

| Total equity | $6,900 |

The balance sheet equation

This accounting equation is the key to the balance sheet:

Assets = Liabilities + Owner’s Equity

Assets go on one side, liabilities plus equity go on the other. The two sides must balance—hence the name “balance sheet.”

It makes sense: you pay for your company’s assets by either borrowing money (i.e. increasing your liabilities) or getting money from the owners (equity).

A sample balance sheet

We’re ready to put everything into a standard template ( you can download one here ). Here’s what a sample balance sheet looks like, in a proper balance sheet format:

Nice. Your balance sheet is ready for action.

Great. Now what do I do with it?

Because the balance sheet reflects every transaction since your company started, it reveals your business’s overall financial health. At a glance, you’ll know exactly how much money you’ve put in, or how much debt you’ve accumulated. Or you might compare current assets to current liabilities to make sure you’re able to meet upcoming payments.

You can also compare your latest balance sheet to previous ones to examine how your finances have changed over time. You’ll be able to see just how far you’ve come since day one. If you need help understanding your balance sheet or need help putting together a balance sheet, consider hiring a bookkeeper .

Here’s some metrics you can calculate using your balance sheet:

- Debt-to-equity ratio (D/E ratio): Investors and shareholders are interested in the D/E ratio of a company to understand whether they raise money through investment or debt. A high D/E ratio shows a business relies heavily on loans and financing to raise money.

- Working capital : This metric shows how much cash you would hold if you paid off all your debts. It signals to investors and lenders how capable you are to pay down your current liabilities.

- Return on Assets: A formula for calculating how much net income is being earned relative to the assets owned. The more income earned relative to the amount of assets, the higher performing a business is considered to be.

Next, we’ll cover the three most important ratios that you can calculate using your balance sheet: the current ratio, the debt-to-equity ratio, and the quick ratio.

The current ratio

Can your company pay its debts? The current ratio measures the liquidity of your company—how much of it can be converted to cash, and used to pay down liabilities. The higher the ratio, the better your financial health in terms of liquidity .

The ratio for finding your current ratio looks like this:

Current Ratio = Current Assets / Current Liabilities

You should aim to maintain a current ratio of 2:1 or higher. Meaning, your company holds twice as much value in assets as it does in liabilities. If you had to, you could pay off all the money you owe two times over.

Once you drop below a current ratio of 2:1, your liquidity isn’t looking so good. And if you dip below 1:1, you’re entering hot water. That means you don’t have enough liquidity to pay off your debts.

You can improve your current ratio by either increasing your assets or decreasing your liabilities.

The quick ratio

Also called the acid test ratio, the quick ratio describes how capable your business is of paying off all its short-term liabilities with cash and near-cash assets. In this case, you don’t include assets like real estate or other long-term investments. You also don’t include current assets that are harder to liquidate, like inventory. The focus is on assets you can easily liquidate.

Here’s how you get the quick ratio:

Quick Ratio = (Cash and Cash Equivalents + Marketable Securities + Accounts Receivable) / Current Liabilities

If your ratio is 1:1 or better, you’re sitting pretty. That means you’ve got enough quick-to-liquidate assets to cover all your short term liabilities in a pinch.

The debt-to-equity ratio

Similar to the current ratio and quick ratio, the debt-to-equity ratio measures your company’s relationship to debt. Only, in this case, the key value is your total equity.

This ratio tells you how much your company depends upon equity to keep running versus how much it depends on outside lenders. It’s calculated like this:

Debt to Equity Ratio = Total Outside Liabilities / Owner or Shareholders’ Equity

Generally speaking, a 2:1 ratio is considered acceptable. If the ratio gets bigger, you start running into trouble. It means your business relies heavily on debt to keep running, which turns off investors. The higher the ratio, the higher the chance that, in the event you need to pay off your debt, you’ll use up all your earnings and cash flows—and investors will end up empty-handed.

Examples of balance sheet analysis

We’ll do a quick, simple analysis of two balance sheets, so you can get a good idea of how to put financial ratios into play and measure your company’s performance.

Annie’s Pottery Palace, a large pottery studio, holds a lot of its current assets in the form of equipment—wheels and kilns for making pottery. Accounts receivable play a relatively minor role.

Liabilities are few—a small loan to pay off within the year, some wages owed to employees, and a couple thousand dollars to pay suppliers.

Annie’s is a single-member LLC—there are no shareholders, so her equity includes only her initial investment, retained earnings, and Annie’s draw($4,000).

Ratio analysis:

Current ratio: 22,000 / 7,000 = 3.14:1

Annie’s current ratio is very healthy. If necessary, her current assets could pay off her current liabilities more than three times over.

Quick ratio: 6,000 / 7,000 = 0.85:1

Her quick ratio isn’t looking so hot, though. Annie’s currently sitting just below 1:1, meaning she wouldn’t be able to quickly pay off debt.

Debt-to-equity ratio: 7,000 / 15,000 = 0.46:1

Annie’s debt-to-equity looks good. She’s got more than twice as much owner’s equity than she does outside liabilities, meaning she’s able to easily pay off all her external debt.

Final analysis:

Annie is able to cover all of her liabilities comfortably—until we take her equipment assets out of the picture. Most of her assets are sunk in equipment, rather than quick-to-cash assets. With this in mind, she might aim to grow her easily liquidated assets by keeping more cash on hand in the business checking account.

That being said, her owner’s equity is more than capable of covering her debt, so this problem shouldn’t be difficult to fix. It would be wise for Annie to take care of it before applying for loans or bringing on investors.

Example balance sheet analysis: Bill’s Book Barn LTD.

A lot of Bill’s assets are tied up in inventory—his large collection of books. The rest mostly consists of long-term investments and intangible assets. (Bill’s Book Barn is famous among collectors of rare fly-tying manuals; a business consultant valued his list of dedicated returning customers at $10,000.)

He doesn’t have a lot of liabilities compared to his assets, and all of them are short-term liabilities. Meaning, he’ll need to pay off that $17,000 within a year.

Finally, since Bill is incorporated, he has issued shares of his business to his brother Garth. Currently, Garth holds a $12,000 share in the business, a little shy of half its total equity.

Ratio analysis

Current ratio: 30,000 / 17,000 = 1.76:1

Since long-term investments and intangible assets are tough to liquidate, they’re not included in current assets—meaning Bill has $30,000 in assets he can more or less easily use to cover his liabilities. His ratio of 1.76:1 isn’t great—it doesn’t leave much wiggle room if he wants to pay off his liabilities. But it isn’t terrible, either—he’s just shy of a healthy 2:1 ratio.

Quick ratio: 7,000 / 17,000 = 0.41:1

Bill’s quick ratio is pretty dire—he’s well short of paying off his liabilities with cash and cash equivalents, leaving him in a bind if he needs to take care of that debt ASAP.

Debt-to-equity ratio: 17,000 / 15,000 = 1.13:1

Once we take into account his $13,000 owner’s draw, Bill’s owner’s equity comes to just $15,000, shy of his $17,000 in debt. Remember, an acceptable debt-to-equity ratio is 2:1. Bill is falling short of acceptable; if he had to pay off all his debts quickly, his equity wouldn’t cover it, and he’d need to dip into his company’s income. That makes his business unattractive to potential investors. Unless he changes course, Bill will have trouble getting financing for his business in the future.

Summary Analysis

Bill’s ratios don’t look great, but there’s hope. If he starts liquidating some of his long-term investments now, he can bump his current ratio up to 2:1, meaning he’d be in a healthy position to pay off liabilities with his current assets.

His quick ratio will take more work to improve. A lot of Bill’s assets are tied up in inventory. If he could convert some of that inventory to cash, he could improve his ability to pay of debt quickly in an emergency. He may want to take a look at his inventory, and see what he can liquidate. Maybe he’s got shelves full of books that have been gathering dust for years. If he can sell them off to another bookseller as a lot, maybe he can raise the $10,000 cash to become more financially stable.

Finally, unless he improves his debt-to-equity ratio, Bill’s brother Garth is the only person who will ever invest in his business. The situation could be improved considerably if Bill reduced his $13,000 owner’s draw. Unfortunately, he’s addicted to collecting extremely rare 18th century guides to bookkeeping. Until he can get his bibliophilia under control, his equity will continue to suffer.

Balance sheets can tell you a lot of information about your business, and help you plan strategically to make it more liquid, financially stable, and appealing to investors. But unless you use them in tandem with income statements and cash flow statements, you’re only getting part of the picture. Learn how they work together with our complete guide to financial statements .

Related Posts

.png)

Owner’s Draw vs. Salary: How to Pay Yourself

How do you pay yourself when you're the boss?

A Quick Guide to Proforma Invoices

If you sell on consignment, you might at some point have to send or receive a proforma invoice, which is different than a regular invoice. Here’s why that’s important.

What is a Chart of Accounts? A How-To with Examples

This is a straightforward guide to the chart of accounts—what it is, how to use it, and why it’s so important for your company’s bookkeeping.

Join over 140,000 fellow entrepreneurs who receive expert advice for their small business finances

Get a regular dose of educational guides and resources curated from the experts at Bench to help you confidently make the right decisions to grow your business. No spam. Unsubscribe at any time.

- Starting a Business

- Growing a Business

- Small Business Guide

- Business News

- Science & Technology

- Money & Finance

- For Subscribers

- Write for Entrepreneur

- Tips White Papers

- Entrepreneur Store

- United States

- Asia Pacific

- Middle East

- South Africa

Copyright © 2024 Entrepreneur Media, LLC All rights reserved. Entrepreneur® and its related marks are registered trademarks of Entrepreneur Media LLC

- Write Your Business Plan | Part 1 Overview Video

- The Basics of Writing a Business Plan

- How to Use Your Business Plan Most Effectively

- 12 Reasons You Need a Business Plan

- The Main Objectives of a Business Plan

- What to Include and Not Include in a Successful Business Plan

- The Top 4 Types of Business Plans

- A Step-by-Step Guide to Presenting Your Business Plan in 10 Slides

- 6 Tips for Making a Winning Business Presentation

- 3 Key Things You Need to Know About Financing Your Business

- 12 Ways to Set Realistic Business Goals and Objectives

- How to Perfectly Pitch Your Business Plan in 10 Minutes

- Write Your Business Plan | Part 2 Overview Video

- How to Fund Your Business Through Friends and Family Loans and Crowdsourcing

- How to Fund Your Business Using Banks and Credit Unions

- How to Fund Your Business With an SBA Loan

- How to Fund Your Business With Bonds and Indirect Funding Sources

- How to Fund Your Business With Venture Capital

- How to Fund Your Business With Angel Investors

- How to Use Your Business Plan to Track Performance

- How to Make Your Business Plan Attractive to Prospective Partners

- Is This Idea Going to Work? How to Assess the Potential of Your Business.

- When to Update Your Business Plan

- Write Your Business Plan | Part 3 Overview Video

- How to Write the Management Team Section to Your Business Plan

- How to Create a Strategic Hiring Plan

- How to Write a Business Plan Executive Summary That Sells Your Idea

- How to Build a Team of Outside Experts for Your Business

- Use This Worksheet to Write a Product Description That Sells

- What Is Your Unique Selling Proposition? Use This Worksheet to Find Your Greatest Strength.

- How to Raise Money With Your Business Plan

- Customers and Investors Don't Want Products. They Want Solutions.

- Write Your Business Plan | Part 4 Overview Video

- 5 Essential Elements of Your Industry Trends Plan

- How to Identify and Research Your Competition

- Who Is Your Ideal Customer? 4 Questions to Ask Yourself.

- How to Identify Market Trends in Your Business Plan

- How to Define Your Product and Set Your Prices

- How to Determine the Barriers to Entry for Your Business

- How to Get Customers in Your Store and Drive Traffic to Your Website

- How to Effectively Promote Your Business to Customers and Investors

- Write Your Business Plan | Part 5 Overview Video

- What Equipment and Facilities to Include in Your Business Plan

- How to Write an Income Statement for Your Business Plan

- How to Make a Balance Sheet

- How to Make a Cash Flow Statement

- How to Use Financial Ratios to Understand the Health of Your Business

- How to Write an Operations Plan for Retail and Sales Businesses

- How to Make Realistic Financial Forecasts

- How to Write an Operations Plan for Manufacturers

- What Technology Needs to Include In Your Business Plan

- How to List Personnel and Materials in Your Business Plan

- The Role of Franchising

- The Best Ways to Follow Up on a Buisiness Plan

- The Best Books, Sites, Trade Associations and Resources to Get Your Business Funded and Running

- How to Hire the Right Business Plan Consultant

- Business Plan Lingo and Resources All Entrepreneurs Should Know

- How to Write a Letter of Introduction

- What To Put on the Cover Page of a Business Plan

- How to Format Your Business Plan

- 6 Steps to Getting Your Business Plan In Front of Investors

How to Make a Balance Sheet Create this important document to show investors the true net worth of your business, and to keep track of your financial trajectory.

By Eric Butow Oct 27, 2023

Key Takeaways

- What a balance sheet should include

- Why you should compare balance sheets year after year

Opinions expressed by Entrepreneur contributors are their own.

This is part 4 / 12 of Write Your Business Plan: Section 5: Organizing Operations and Finances series.

If the income sheet shows what you're earning, the balance sheet shows what you're worth. A balance sheet can help an investor see that a company owns valuable assets that don't show up on the income statement or that it may be profitable but is heavily in debt. It adds up everything your business owns, subtracts everything the business owes, and shows the difference as the net worth of the business.

Actually, accountants put it differently and, of course, use different names. The things you own are called assets. The things you owe money on are called liabilities. And net worth is referred to as equity.

Related: How to Calculate Your Net Worth and Grow Your Wealth

A balance sheet shows your condition on a given date, usually the end of your fiscal year. Sometimes balance sheets are compared. That is, next to the figures for the end of the most recent year, you place the entries for the end of the prior period. This gives you a snapshot of how and where your financial position has changed.

A balance sheet also places a value on the owner's equity in the business. When you subtract liabilities from assets, what's left is the value of the equity in the business owned by you and any partners. Tracking changes in this number will tell you whether you're getting richer or poorer.

An asset is basically anything you own of value. It gets a little more complicated in practice, but that's the working definition.

Assets come in two main varieties: current assets and fixed assets. Current assets are anything that is easily liquidated or turned into cash. They include cash, accounts receivables, inventory, marketable securities, and the like.

Related: How to Write an Income Statement for Your Business Plan

Fixed assets include stuff that is harder to turn into cash. Examples are land, buildings, improvements, equipment, furniture, and vehicles.

The fixed asset part of the balance sheet sometimes includes a negative value—that is, a number you subtract from the other fixed asset values. This number is depreciation, and it's an accountant's way of slowly deducting the cost of a long-lived asset such as a building or a piece of machinery from your fixed asset value.

Intellectual properties, such as patents and copyrights, also fall into the asset category. For some companies, a recipe, a formula, or a new invention may actually be their most valuable asset. Of course, the actual value is often very hard to determine. Patents, trademarks, copyrights, exclusive distributorships, protected franchise agreements, and the like do have somewhat more accessible value.

Related: Net Worth Calculator for Franchises

You'll also have intangibles such as your reputation, your standing in the community, and "goodwill," which are difficult to put a value on. Probably the best way to think of goodwill is like this: If you sell your company, the IRS says the part of the sales price that exceeds the value of the assets is goodwill. As a result of its slipperiness, some planners never include an entry for goodwill, although its value may in fact be substantial.

Liabilities

Liabilities are the debts your business owes. They come in two classes: short-term and long-term.

Short-term liabilities are also called current liabilities. Any debt that is going to be paid off within twelve months is considered current. That includes accounts payable you owe suppliers, short-term bank loans (shown as notes payable), and accrued liabilities you have built up for such things as wages, taxes, and interest.

Related: Tips and Strategies for Using the Balance Sheet as Your Franchise Scorecard

Any debt that you won't pay off in a year is long-term. Mortgages and bank loans with more than a one-year term are considered in this class.

A Note on Land

Almost anything can lose value, but for accounting purposes, land doesn't. As a rule, you never depreciate land, although you may depreciate buildings as well as other long-lived purchases.

Buzzword: Book Value

The book value of the business is the net worth (or owner's equity). Most valuation methods for small and midsized businesses use the net worth plus adjusted earnings or free cash flow multiple to create a rough and ready valuation. If you are just starting out, you will probably feel that you are undervalued because you have nothing on which to base your value. Don't fret: Value grows with time as you build your business. It's better that the value of your business honestly reflects your business. If you recall the dot-com crash of 2000, it was largely the result of many up-and-coming dot-coms being greatly overvalued.

Related: How to Make a Cash Flow Statement

Tax Considerations

You always want to maximize profits, right? Savvy entrepreneurs know that managing reported profits can save on taxes. Part of the trick is balancing salaries, dividends, and retained earnings.

Tax regulations treat each differently, and you can't exactly do whatever you want. Get good advice and be ready to sacrifice reported profits for real savings.

Personal Financial Statement

Investors and lenders like to see business plans with substantial investments by the entrepreneur or with an entrepreneur who is personally guaranteeing any loans and has the personal financial strength to back those guarantees. Your personal financial statement is where you show plan readers how you stack up financially as an individual.

Related: The Definition of Value Is Changing — Here's What Entrepreneurs Need to Know to Survive the Shifting Global Trends

The personal financial statement comes in two parts. One is similar to a company balance sheet and lists your liabilities and assets. A net worth figure at the bottom, like the net worth figure on a company balance sheet, equals total assets minus total liabilities.

A second statement covers your personal income. It is similar to a company profit and loss statement, listing all your personal expenses, such as rent or mortgage payments, utilities, food, clothing, and entertainment. It also shows your sources of income, including earnings from a job, income from another business you own, child support or alimony, interest and dividends, and the like.

The figure at the bottom is your net income; it equals total income minus total expenses. If you've ever had to fill out a personal financial statement to borrow money for a car loan or home mortgage, you've had experience with a personal financial statement. You should be able to simply update figures from a previous personal financial statement.\

Related: How to Make Realistic Financial Forecasts

Because this is important only to investors or lenders, you want to be careful to include this only when necessary. For a small business looking for a small amount of funding, you may be able to draft something with your accountant verifying your net worth and/or previous year's income.

More in Write Your Business Plan

Section 1: the foundation of a business plan, section 2: putting your business plan to work, section 3: selling your product and team, section 4: marketing your business plan, section 5: organizing operations and finances, section 6: getting your business plan to investors.

Successfully copied link

.webp "create business plan balance sheet")

How to make a balance sheet: A step-by-step guide

Building a balance sheet is an important practice that must be conducted on either a quarterly or monthly basis. This financial statement provides insight into your company’s financial health by detailing your assets, liabilities, and shareholders’ equity.

Not sure how to create a balance sheet? Below, we’ll delve into the purpose of creating balance sheets (also known as net worth statements) and then provide a step-by-step guide of how to make your own. P.S. For more templates, check out our Accounting Documents Library .

What is a balance sheet?

An accounting balance sheet is a snapshot of your company’s financial situation. Balance sheets help with financial planning and give businesses visibility into company assets, liabilities, and owner’s equity. It’s one of the three fundamental financial statements that every business owner needs to have in order to perform financial modeling and accounting—the other two documents being an income statement and cash flow statement.

At its essence, an accounting balance sheet is one of the most accurate ways to analyze the company’s financial position. When fleshed out, a balance sheet can show you:

- What the business owns

- What the business owes

- How much has been invested into the company

As the name suggests, your company’s assets must always be equal to the combined value of your liabilities and equity. Some businesses use hedge accounting to reduce volatility impact in financial statements, however, the sheet must be balanced. If either is out of alignment, your calculations or notations are incorrect. According to Harvard University : “A balance sheet is a financial statement that communicates the so-called ’book value’ [assets - liabilities] of an organization, as calculated by subtracting all of the company’s liabilities and shareholder equity from its total assets.”

What’s the difference between a balance sheet and an income statement?

An income statement, also called a profit and loss (P&L) statement, lists out a company’s revenue streams (such as sales) and expenses (payroll, operating expenses, etc.) over a given period of time.

A balance sheet, on the other hand, covers a company’s assets (cash, outstanding receivables, securities, inventory, etc.) and liabilities (outstanding payables, debt payments, taxes, rent, etc.) at a certain point of time.

These two statements provide complementary information. An income statement tells you a company’s profitability, margins, and revenue over a period of time, while a company’s balance sheet gives you a snapshot of their overall financial health and solvency at a certain point.

The purpose of a balance sheet

A balance sheet is a snapshot of the company’s financial position at a specific point in time. It’s a critical measurement both internally and externally, but for different reasons:

Internal analysis

Balance sheets help you see whether a business is succeeding or struggling. By analyzing your liquidity position (i.e. cash and receivables), you’ll see whether you can afford upcoming expenses or handle a market shock. Additionally, you can analyze historical trends in your assets and liabilities to ensure your business is running properly, or to identify problem areas quickly. If the numbers don’t look good, it can prompt an internal shift in how you conduct the business.

External evaluation

Balance sheets are a tool that help investors, lenders, stakeholders, and external regulators gauge the financial position of a business, what resources are currently available, and how they were financed. For investors, this can help them see whether or not it would be smart to invest in the company. They can extrapolate upon these numbers to determine other financial performance metrics like debt-to-equity ratio, equity multiplier , profitability, and liquidity. For external auditors, a balance sheet can help them confirm that the company is complying with reporting laws.

What’s on a balance sheet?

Practically every balance sheet boils down to the following equation:

Assets = Liabilities + Shareholder’s equity

In addition, this equation is tied to a particular date, known as the “reporting date.” Although it depends on your business, in most cases, a balance sheet should be prepared and then distributed at least on a quarterly basis, if not monthly. Larger businesses will often create monthly balance sheets, while small businesses or startups typically create them quarterly.

Balance sheets are made up of three key elements:

The asset section of a balance sheet reveals what items of value your business owns. These assets are typically arranged by order of liquidity—in other words, how easily they can be converted into cash. This typically breaks down further into two categories of assets:

Current assets

Assets that could likely be converted into cash within a year. These have various sub categories, including:

- Cash and cash equivalents – Your most liquid assets —cash, checks, and money kept in your bank account.

- Accounts receivable – Money your clients owe that will be paid in the near future.

- Marketable securities – Traded investments that you can easily sell off.

- Prepaid expenses – Valuables you’ve already paid for such as insurance or rent.

- Inventory – Equipment, raw materials, and finished products.

Long-term assets

According to Investopedia , long-term assets (also called non liquid or illiquid assets and non-current assets) are defined as “a company's value of property, plant, and equipment that can be used for more than 1 year, minus depreciation.” These include:

- Fixed assets – Property, buildings, equipment, and machinery.

- Intangible assets – Nonphysical assets such as patents, copyrights, licenses, and franchise agreements.

- Long-term securities – Investments that can't be sold off within a year such as bonds or real estate.

2. Liabilities

The liability section of the balance sheet demonstrates what money you currently owe to others, this includes recurring expenses and various forms of debt. Liabilities are broken down into two subcategories. They are either long-term liabilities (also called non-current liabilities) or current liabilities.

- Current liabilities – Utilities, taxes, rent, accounts payable, and payments toward long-term debt interest such as business loans or credit cards.

- Long-term liabilities – Bonds payable and long-term debts.

See our guide on how to calculate liabilities for more info.

3. Shareholder’s equity

The shareholder's equity section of the balance sheet shows the value of funds that shareholders have invested in the company as well as retained earnings . For retained earnings, the company must pay out dividends from the net income. Shareholders’ Equity = Total Assets – Total Liabilities.

How to make a balance sheet in 8 steps

Now that you know what’s in a balance sheet, how do you make your own? Follow these steps:

Step 1: Pick the balance sheet date

A balance sheet is meant to show all of your business assets, liabilities, and shareholders’ equity on a specific day of the year, or within a given period of time. Most companies prepare reports on a quarterly basis, typically on the last day of March, June, September, and December. Companies may also choose to prepare balance sheets on a monthly basis, in which case they would report on the last day of each month.

Step 2: List all of your assets

Once you’ve set a date, your next task is to list out all of your current asset items in separate line items. To make this section more actionable, it’s best to separate them in order of liquidity. More liquid items like cash and accounts receivable go first, whereas illiquid assets like inventory will go last. After listing a current asset, you’ll then need to include your non-current (long-term) ones. Don’t forget to include non-monetary assets as well.

Step 3: Add up all of your assets

After detailing your various asset categories, add them all up. The final tally will then go under the total assets category. To ensure that your numbers are correct, double check this figure against the company’s general ledger.

Step 4: Determine current liabilities

List the current liabilities that are due within a year of the balance sheet date. These include accounts payable, short-term notes payable, and accrued liabilities.

Step 5: Calculate long-term liabilities

List the liabilities that won’t be settled within the year. These include long-term notes, bonds payable, pension plans, and mortgages.

Step 6: Add up liabilities

Add up the current liabilities subtotal with the long-term liabilities subtotal to find your total liabilities.

Step 7: Calculate owner’s equity

Determine your business’ retained earnings and working capital, as well as the total shareholders’ equity. Retained earnings are the business’ profits which are reserved for reinvestments (not distributed as dividends to shareholders). Shareholders’ equity is the combination of share capital plus retained earnings.

Step 8: Add up liabilities and owners’ equity

If your liabilities + equity = assets, you’ve performed the balance correctly. If it doesn’t, you may have to go back and review your work.

Ramp: greater visibility & helping you close books faster

By building your three core financial statements (balance sheet, income statement, and cash flow statement) into your calendar, you’ll enjoy greater visibility into your company’s financial future which can help make better business and financial decisions. However, building balance sheets on a quarterly or monthly basis can be a time-consuming process even with accounting software or bookkeeping software.

That’s where Ramp comes in.

Ramp is the only corporate card that can help you streamline the balance sheet creation process and close books faster at the end of the month. This is accomplished thanks to the automated expense management and real-time spend tracking platform built into the card. With Ramp on your team, it’s easier to create a balance sheet and close your books faster.

Don't miss these

How Ramp helped Quora’s finance team streamline operations, simplify AP, and stay lean

How Ramp helped Apprentice.io modernize accounting with automation

How Ramp helped Zola do more with less

How Gill’s Onions increased compliance, drove efficiency, and reduced tears with Ramp

How Dragonfly Pond Works leveled up expense management with Ramp

.png "create business plan balance sheet")

How Girl Scouts of the Green & White Mountains saved 20+ hours per month with Ramp

How 8VC resolved accounting coding challenges, increased spend visibility, and cut time to close with Ramp

| You might be using an unsupported or outdated browser. To get the best possible experience please use the latest version of Chrome, Firefox, Safari, or Microsoft Edge to view this website. |

What Is A Balance Sheet? (Example Included)

Updated: Jun 1, 2024, 2:22pm

Table of Contents

What is a balance sheet, components of a balance sheet, how to balance a balance sheet, why is a balance sheet important, balance sheet example, frequently asked questions (faqs).

When you’re starting a company, there are many important financial documents to know. It might seem overwhelming at first, but getting a handle on everything early will set you up for success in the future. Today, we’ll go over what a balance sheet is and how to master it to keep accurate financial records.