Business Plan Template for Vendors

- Great for beginners

- Ready-to-use, fully customizable Subcategory

- Get started in seconds

As a vendor or small business owner, creating a solid business plan is essential to attracting investors, securing funding, and effectively managing your operations. With ClickUp's Business Plan Template for Vendors, you can now streamline the entire process and take your business to the next level!

This fully customizable template allows you to:

- Outline your business goals, strategies, and financial projections with ease

- Showcase your unique value proposition and competitive advantage

- Create a clear roadmap for growth and success

- Collaborate with team members, investors, and stakeholders in real-time

Don't let the complexity of creating a business plan hold you back. Get started with ClickUp's Business Plan Template for Vendors today and watch your business thrive!

Business Plan Template for Vendors Benefits

A business plan template for vendors offers a range of benefits to help vendors and small business owners succeed in their business endeavors:

- Provides a clear and structured framework to outline business goals, strategies, and financial projections

- Helps attract potential investors by showcasing a well-thought-out plan and potential for profitability

- Enables vendors to secure funding by presenting a professional and comprehensive business plan

- Assists in effectively managing operations by setting clear objectives and strategies

- Guides vendors in making informed decisions and adapting to market changes

- Supports long-term growth and sustainability by identifying potential risks and opportunities

Main Elements of Vendors Business Plan Template

ClickUp’s Business Plan Template for Vendors provides all the essential elements to help vendors or small business owners create a comprehensive and effective business plan:

- Custom Statuses: Track the progress of each section of your business plan with statuses like Complete, In Progress, Needs Revision, and To Do, ensuring that you stay on top of every task.

- Custom Fields: Utilize custom fields such as Reference, Approved, and Section to add specific details and organize important information within your business plan template.

- Custom Views: Access different views like Topics, Status, Timeline, Business Plan, and Getting Started Guide to gain a clear picture of your business plan's structure, track progress, and navigate through different sections easily.

- Collaboration Tools: Take advantage of ClickUp's collaboration features, including assigning tasks, leaving comments, and attaching files, to work seamlessly with your team members and stakeholders.

- Integration Capabilities: Connect ClickUp with other tools you use in your business, such as Google Drive, Slack, or Trello, to streamline your workflow and enhance productivity.

How To Use Business Plan Template for Vendors

If you're a vendor looking to create a solid business plan, the Business Plan Template in ClickUp can be an invaluable tool. Follow these six steps to get started:

1. Define your vision and mission

Before diving into the details, take some time to define your overall vision and mission for your vendor business. What do you hope to achieve? What value do you want to bring to your customers? Clearly articulating your vision and mission will set the foundation for your entire business plan.

Use a Doc in ClickUp to brainstorm and outline your vision and mission statements.

2. Conduct market research

To create an effective business plan, you need a deep understanding of your target market and competition. Research industry trends, identify your target audience, and analyze your competitors' strengths and weaknesses. This information will guide your marketing and sales strategies and help you stand out in a crowded market.

Use the Table view in ClickUp to organize and analyze your market research data.

3. Set clear goals and objectives

Now that you have a better understanding of your market, it's time to set specific and measurable goals for your vendor business. These goals will provide direction and focus for your business plan. Whether it's increasing sales, expanding into new markets, or improving customer satisfaction, make sure your goals align with your overall vision.

Create Goals in ClickUp to track and monitor your progress towards achieving your objectives.

4. Develop a product or service strategy

Outline your products or services and how they meet the needs of your target market. Define your unique selling proposition (USP) and highlight the key features and benefits that differentiate you from your competitors. Consider pricing strategies, distribution channels, and any additional services or add-ons you can offer to enhance customer value.

Use custom fields in ClickUp to track and organize your product or service strategy.

5. Create a marketing and sales plan

Your business plan should include a comprehensive marketing and sales strategy to promote and sell your products or services. Outline your target audience, marketing channels, advertising tactics, and sales goals. Consider leveraging digital marketing, social media, and partnerships to reach your target customers effectively.

Use Automations in ClickUp to automate repetitive marketing tasks and streamline your sales processes.

6. Monitor and refine your plan

Your business plan is not set in stone. It's essential to regularly review and refine your plan as your business evolves. Monitor your key performance indicators (KPIs), track your progress towards your goals, and make adjustments as necessary. Stay agile and adapt your strategies based on market feedback and changing customer needs.

Use Dashboards in ClickUp to track and visualize your KPIs and regularly review your business plan's effectiveness.

By following these steps and utilizing the Business Plan Template in ClickUp, you'll be well-prepared to navigate the vendor business landscape and achieve long-term success.

Get Started with ClickUp’s Business Plan Template for Vendors

Vendors and small business owners can use this Business Plan Template for Vendors to create a comprehensive plan that outlines their goals, strategies, and financial projections.

First, hit “Add Template” to sign up for ClickUp and add the template to your Workspace. Make sure you designate which Space or location in your Workspace you’d like this template applied.

Next, invite relevant members or guests to your Workspace to start collaborating.

Now you can take advantage of the full potential of this template to create a successful business plan:

- Use the Topics View to organize your business plan into different sections such as Executive Summary, Market Analysis, Marketing Strategy, etc.

- The Status View will help you track the progress of each section of your business plan, whether it's complete, in progress, needs revision, or to do

- The Timeline View will help you set deadlines and visualize the overall timeline of your business plan

- The Business Plan View will give you a comprehensive overview of your entire plan, including all sections and their statuses

- The Getting Started Guide View will provide you with a step-by-step guide on how to use the template effectively

- Customize the Reference, Approved, and Section custom fields to add additional information and categorize your business plan

- Update statuses and custom fields as you work on each section to keep track of progress and approvals

- Monitor and analyze your business plan to ensure it aligns with your goals and attracts investors.

- Business Plan Template for Marine Technicians

- Business Plan Template for Transportation Services

- Business Plan Template for Occupational Therapy

- Business Plan Template for Environmental Consultants

- Business Plan Template for Fenty Beauty

Template details

Free forever with 100mb storage.

Free training & 24-hours support

Serious about security & privacy

Highest levels of uptime the last 12 months

- Product Roadmap

- Affiliate & Referrals

- On-Demand Demo

- Integrations

- Consultants

- Gantt Chart

- Native Time Tracking

- Automations

- Kanban Board

- vs Airtable

- vs Basecamp

- vs MS Project

- vs Smartsheet

- Software Team Hub

- PM Software Guide

Vendor Management Plan Template

What is a Vendor Management Plan?

A vendor management plan provides an overview of the steps and processes involved in managing vendor relationships. The plan should be tailored to the organization’s specific goals and objectives, as well as to the scope of the products or services provided by the vendor. It should be designed to ensure that the organization is able to maintain consistent and effective communication with the vendor, track performance, and ensure compliance with vendor-specific policies and procedures.

What's included in this Vendor Management Plan template?

- 3 focus areas

- 6 objectives

Each focus area has its own objectives, projects, and KPIs to ensure that the strategy is comprehensive and effective.

Who is the Vendor Management Plan template for?

This Vendor Management Plan template is designed to help organizations of all sizes and industries create a plan to manage their vendors. It will provide a comprehensive framework that outlines the objectives and goals of the organization, as well as the actionable steps needed to achieve them. The template also includes key performance indicators (KPIs) and projects that can help organizations measure and monitor the effectiveness of their vendor management plan.

1. Define clear examples of your focus areas

Focus areas should be determined in order to best guide the development of the vendor management plan. A focus area is an area of a business, operation, or strategy that requires attention and is typically associated with a specific goal. Examples of focus areas for a vendor management plan may include understanding vendor performance, strengthening vendor relationships, and managing vendor compliance.

2. Think about the objectives that could fall under that focus area

Objectives are the specific goals that should be achieved in order to meet the focus area. These objectives should be specific, measurable, and achievable, and should be tailored to the organization’s individual needs. Examples of objectives for a vendor management plan may include improving vendor quality, increasing vendor efficiency, and strengthening vendor relationships.

3. Set measurable targets (KPIs) to tackle the objective

A key performance indicator (KPI) is a metric used to measure the progress of an objective. These KPIs should be specific, measurable, and achievable, and should be tailored to the organization’s individual needs. Examples of KPIs for a vendor management plan may include reducing defects from vendors, decreasing the average delivery time from vendors, increasing the frequency of communication with vendors, and increasing the vendor satisfaction score.

4. Implement related projects to achieve the KPIs

Projects are the actionable steps that need to be taken in order to achieve the objectives and KPIs. These projects should be specific, measurable, and achievable, and should be tailored to the organization’s individual needs. Examples of projects for a vendor management plan may include monitoring and assessing vendor quality, streamlining vendor processes, increasing vendor interactions, and verifying vendor compliance.

5. Utilize Cascade Strategy Execution Platform to see faster results from your strategy

Cascade Strategy Execution Platform is a software solution designed to help organizations create and execute their strategic plans. The platform allows organizations to track and monitor performance, measure KPIs, and develop and implement projects quickly and easily. Cascade can also help organizations analyze data and gain insights into the effectiveness of their plan, allowing them to make changes and improvements in real-time.

The Whatfix Blog | Drive Digital Adoption

- CIO CIO CIO Blog Explore all new CIO, change, and ITSM content on our enterprise digitalization blog hub. Explore by Category Business Processes Change Management Digital Adoption Digital Transformation ERP Healthcare Transformation ITSM Insurance Transformation Procurement

- Employee Experience Employee Experience EX Blog Explore all new employee experience related content on our EX blog hub. Explore by category Employee Onboarding Employee Training HCM HR & People Ops Instructional Design Learning Technology Performance Support Skill Development CRM Sales Ops

- CX & Product Product CX & Product Ops Blog Explore all new CX and product-related content on our CX and product manager hub. Explore by category Product Ops Support Technical Documentation User Feedback User Onboarding

- Resources Customer Experience What Is a Digital Adoption Platform? Learn how DAPs enable technology users in our ultimate guide. Resources Case Studies eBooks Podcasts White Papers

- Explore Whatfix What Is Whatfix? Whatfix DAP Create contextual in-app guidance in the flow of work with Whatfix DAP. Mirror Easily create simulated application experiences for hands-on IT training with Whatfix Mirror. Product Analytics Analyze how users engage with desktop and web apps with no-code event tracking. Resources About Us Pricing Userization Whatfix AI

- Back to Blog

- Procurement

What Is Vendor Management? (+Challenges, Process, Tools)

- May 18, 2022

Vendor management is the various business processes that organizations go through when working with multiple suppliers and vendors to control costs, reduce risk, and offer excellent service. It empowers companies to optimize costs, reduces potential risks, and ensures high-quality service deliverability – all while managing relationships with dozens of vendors and suppliers.

In this guide, we’ll cover the types of vendor management, break down the entire process into actionable steps, highlight the challenges you should be prepared for, and highlight the best vendor management system (or VMS) to help manage your supplier relationships.

What Is Vendor Management?

Vendor management is a set of practices that businesses follow to find the right vendors and build mutually beneficial relationships with them to control overall cost, reduce risk, and continue to offer excellent servce. It involves vendor analysis, sourcing, contract management, performance reviews, and all the other interactions that you might have with your suppliers.

Often, companies only create processes to manage the first few stages of vendor management – the stages where they source the most cost-effective solution and sign a contract. However, creating an effective vendor management framework offers benefits far beyond just agreeing to a relationship.

Types of Vendor Management

There are nine types of vendor management every company deals with regularly when managing their supplier relationships:

1. Procurement

Procurement is the practice of researching and obtaining products or services critical for performing organization operations.

It’s the first and probably most important stage of vendor management. If you manage to find the right supplier, the rest of the journey shouldn’t be a problem.

Procurement includes the following steps:

- Identifying the need

- Requesting the purchase

- Reviewing the request

- Assessing vendors

- Requesting quotations

- Negotiating and signing a contract

- Receiving supply

2. Vendor onboarding

The other aspect of vendor management is vendor onboarding. It’s the process of providing vendors with all the necessary information, tools, and permissions to activate new suppliers successfully. A solid onboarding process builds the ground for strong buyer-supplier relationships.

During the vendor onboarding process, you’ll:

- Complete risk assessments

- Establish clear expectations and requirements

- Verify vendors’ documents

- Develop an exit strategy

- Implement a communication system

- Provide invoicing details

3. Vendor relationship management

Vendor relationship management (VRM) refers to the process of deepening your relationships with suppliers by ensuring the proper investment into the alliance. The objective of vendor relationship management is to get the maximum possible value from a contractual arrangement.

Here are some of the VRM activities:

- Tracking and documenting disputes

- Collaborating with suppliers

- Running regular performance check-ins

- Inviting vendors to company workshops

- Building a sound contract management strategy

4. Vendor risk management

Vendor risk management, also known as VRM, is a set of activities aimed at reducing the likelihood of suppliers causing business disruptions or taking fraudulent actions.

83% of companies faced a third-party-related incident driving negative consequences for business in the last three years. 59% of respondents confirm that their organizations experienced a data breach caused by one of their suppliers. To mitigate these risks, you’d better perform the assessment process for each of your potential and existing vendors.

There are many risks associated with vendor management, including:

- Cybersecurity risk: possible cyber-attacks or data breach

- Operational risk: business operations disruptions

- Legal and compliance risk: failure to comply with local legislation

- Reputational risk: a negative impact of the partnership on the organization’s image

- Financial risk: revenue loss

5. Performance management

This type of vendor management aims at monitoring and evaluating vendor performance. In other words, it’s a practice of finding out how good your vendors are. To have metrics to compare your vendors’ performance against, you need to set KPIs for service providers and clear standards for product suppliers.

Vendor performance management spots issues with outsourced products or services and provides you with an opportunity to notify vendors about arising problems.

6. Contract management

Vendor contract management is the process of creating and executing vendor contracts to maximize the operational and financial outcomes of the partnership, all while reducing financial risk.

Managing vendor contracts can be a headache for your legal team or procurement managers. You can facilitate it by building a contract management plan and implementing contract lifecycle management (CLM) software or leveraging procurement software . A clear plan will draft the key workflows for the entire contract lifecycle, and software will help you automate the processes and store everything in one place.

7. Compliance management

Vendor compliance refers to requirements that a buyer sets for their vendors in order to regulate the buyer-vendor relationships.

Compliance management is the strategy aimed at assisting both buyers and suppliers to ensure vendors’ compliance with buyers’ statutory, legal, and technical requirements. The key to successful vendor compliance management is drafting a policy that sets clear expectations and provides unambiguous guidelines. When it’s in place, all you need to do is to communicate it to your vendors and keep an eye on their performance.

8. SLA management

Service-level agreements (SLAs) are a contract between a buyer and a vendor that sets the expectations between both parties. It outlines particular aspects of the supply being provided such as how and when the product or service should be delivered, which party is responsible for reporting faults, etc.

SLA management is the practice of keeping track of these contracts and making sure vendors meet the terms outlined there. As a part of SLA management, buyers may also lay out the metrics by which the service or product is measured, as well as the penalties applied if the outlined requirements are not fulfilled.

What Is Procurement? Types, Best Practices, Metrics

Contract Lifecycle Management 101: A CLM Guide

13 Best Digital Adoption Platforms (DAPs) in 2024

Benefits of Vendor Management

We’ve already touched upon vendor management benefits such as cost savings and reduced risks. Let’s see the full list of perks coming with a proper vendor management strategy:

1. Better vendor selection

A comprehensive vendor management plan supports the selection of the right strategic vendor partners. By identifying business needs and setting clear expectations, a business can find and invest in high-quality supplies that pay off in the long run.

2. Streamlined processes

When the responsibilities of both a buyer and vendor are outlined, it’s easier to establish smooth workflows. Delivery, compliance, and payments are managed according to a pre-defined scenario, making it easier to guarantee predictable outcomes and an overall more effective procure-to-pay process .

3. More efficient vendor onboarding

Onboarding new vendors and getting them up to speed might take a lot of time and resources. With a vendor management system, new vendors follow a tried and tested path which allows them to navigate through the onboarding process faster.

4. Reduced risk of disruption to supply chain

Vendor management gives you better control over your supply chain and eliminates the risk of disruptions. Having a handle on vendor relationships allows you to obtain critical vendor information promptly and oversee possible issues.

5. Better relationships with vendors

You can’t eliminate the human factor from your vendor relationships. Effective supplier management strengthens loyalty and encourages your vendors to maintain the quality of provided products or services.

6. Reduced costs with more overall efficiency and better vendor rates

As a result of strong vendor relationships, you can achieve better rates and negotiate lucrative deals for your company. Also, having a grasp on your supply chain, you see the hidden costs and gain higher control over your expenses.

Stages of the Vendor Management Process

Here are the six stages involved in the supplier and vendor management process:

1. Discovery, research, and selecting vendors

Vendor management starts with proper research. You need to find a vendor best suited for your needs based on a set of criteria:

- Industry-related experience

- Business management and operations

- Associated risks

- Economies of scale

- Social proof

- Terms and conditions

- Legal considerations

When you have all the data at hand, you can make an informed decision and choose the best vendor.

2. Contract negotiations

To set the foundation for long-lasting vendor relationships, you should reach mutually beneficial contract terms in the first place. The negotiation process includes:

- Outlining risks

- Setting security expectations

- Getting visibility into a vendor’s subcontractors

- Agreeing upon KPIs for performance monitoring

- Defining financial terms

It’s good to research your vendor’s business model at this stage and try to understand their objectives. This way, you’ll manage to negotiate the best terms without sacrificing the supply quality.

3. Vendor onboarding

Once the vendor is approved, they’re onboarded into your company’s system. To set them up for success, you’ll need to introduce them to the relevant procedures, establish standards, and set efficient lines of communication.

The vendor onboarding process involves collecting the documentation, sharing permissions, and other activities aimed at integrating a new vendor into the supply chain.

4. Monitoring performance and managing risk

You can’t always be sure that your vendors will keep to the standards set in your contract. That’s why you should be continuously monitoring supplier performance until the contract is terminated.

To make it easy to assess the performance of your vendors, you’d better set KPIs when negotiating contract terms. These might include:

- Order completion time

- Shipping time

- Product or service quality

- Customer service quality

Keep track of these performance metrics and keep open communication with your suppliers to have full control over your supply chain.

5. Payment collection and processing

Strong vendor relationships are based on mutual respect. The best way to show your respect to vendors is by making payments on time, in accordance with the terms outlined in the contract. Vendor management entails building a standardized procedure for processing invoices and making payments, eliminating unnecessary friction from the processes.

6. Feedback from vendors

You aren’t the only party that can share their feedback. It’s important that your vendors also feel encouraged to provide their views of this collaboration. Collecting feedback from vendors will help you get a 360-degree view of the state of things and make more informed decisions.

Challenges of Vendor Management

On your way to a strong vendor management program, you need to overcome certain challenges.

1. Organizing all vendors into one centralized view

You work with dozens of vendors – from coffee capsule suppliers to employee engagement software providers. Organizing and managing them effectively is impossible without suitable processes and tools.

2. Personalizing vendor onboarding and continuous support

You can’t standardize the entire onboarding process when you deal with vendors in completely different sectors. You must find a way to personalize onboarding while delivering a consistent experience.

3. Relying too heavily on certain vendors

With strong buyer-vendor relationships comes the danger of supplier overreliance. What if you lose them? Your business operations will inevitably be disrupted unless you have a supply chain backup plan.

4. Keeping your vendor data clean and compliant

With a vendor management system, your employees that are vendor and supplier-facing will be required to update order and vendor forms. However, companies will have various processes for different vendors and unique workflows for contextual situations.

With a tool like Whatfix, you can provide real-time performance support that helps employees know what data needs to be updated, what is required for each vendor, and in what format it is required – all right inside your vendor management application with smart tips.

4 Best Vendor Management Software in 2024

The following vendor management systems will help you address supplier and vendor challenges and build streamlined processes.

Vanta is a platform automating the processes of compliance certification for vendors. It makes it easy to craft policies and establish processes to achieve SOC 2, ISO 27001, HIPAA, PCI, and GDPR compliance painless.

A spend management platform, Airbase allows companies to take full control of their spending through one interface. It serves as a centralized command and control center that stores vendor details, creates bills from invoices, and supports international vendor payments. With Airbase, users can manage any types of payments such as cards, checks, ACH, vendor credits, and international transfers.

3. SAP Fieldglass

SAP Fieldglass is a comprehensive vendor management system (VMS) that enables organizations to organize, monitor, engage, and pay their vendors from a single app. The platform is best suited for enterprises for its advanced functionality.

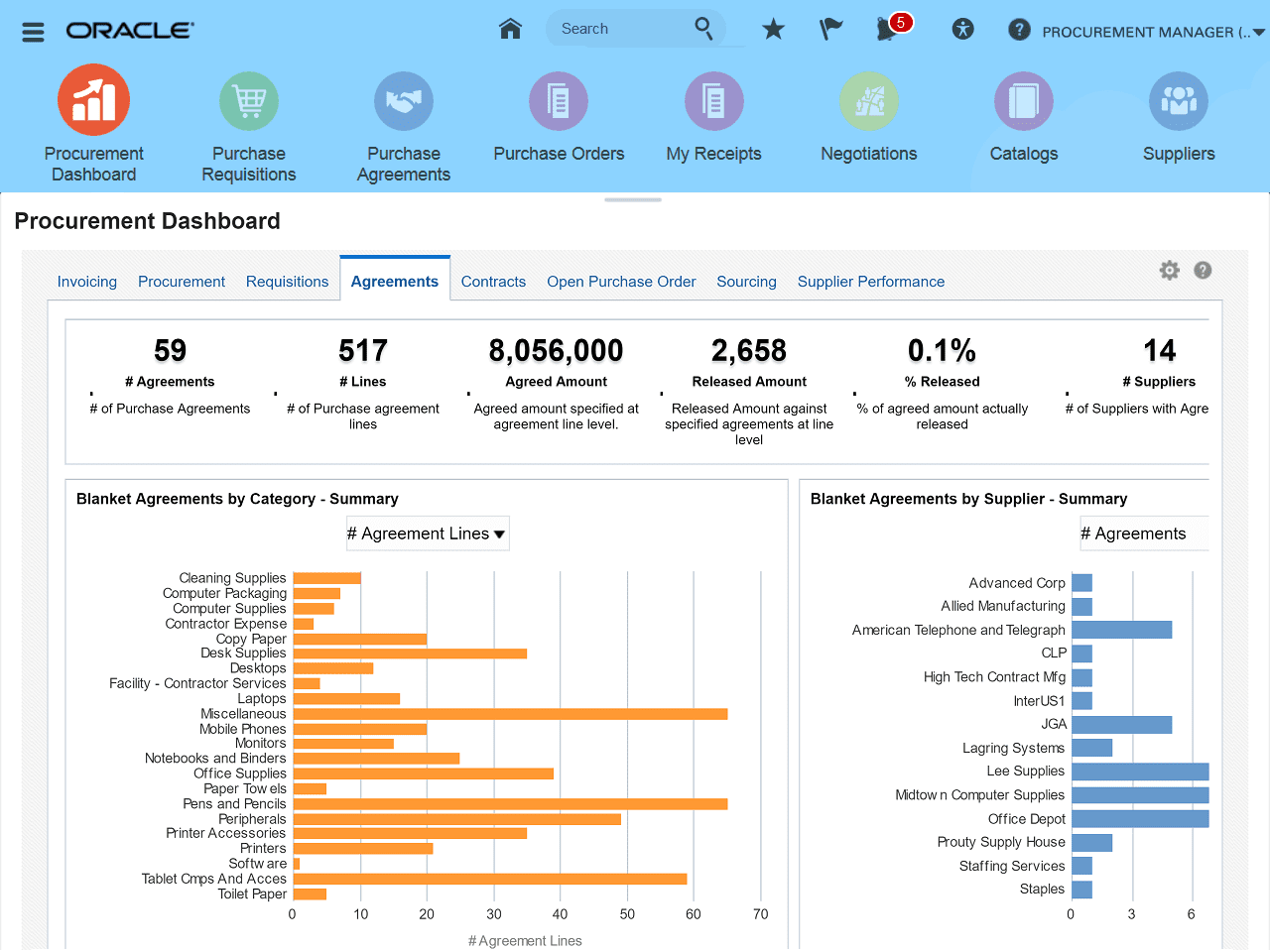

4. Oracle Procurement Cloud

Oracle Procurement presents a tool suite for automating procurement, strategic sourcing, and supplier management processes. Its tools facilitate shopping, order creation, vendor monitoring, payments, reporting, and other processes involved in vendor management.

With Whatfix, drive adoption of your source-to-pay , procurement, and vendor management applications across your suppliers, vendors, procurement teams, and more with contextual in-app guidance.

With Whatfix, you’re empowered to create in-app content such as:

- Interactive walkthroughs

- Step-by-step guides

- Smart tips

- Onboarding task lists

- Embedded knowledge bases

Whatfix lays on top of all modern S2P applications SAP Ariba, Jaggaer, Coupa, iValua, and more – as well as CLM software, procurement tools, CRM systems, and more.

Whatfix is also a fantastic solution for providing personalized, guided onboarding and on-demand self-support for your vendors.

Learn more about Whatfix for S2P applications and vendor management now!

Request a demo to see how Whatfix empowers organizations to improve end-user S2P application adoption, create effective vendor onboarding experiences, and provide on-demand vendor and customer self-support

Thank you for subscribing!

- Accounts Payable Software

- Accounts Receivable Software

- Travel & Expense Management

- Payment Automation

- Cash Flow Management

- Account Payable

- Account Receivable

- Travel & Expense

- Finance News

- Press Release

- Get Started

8 Step Guide to Creating a Vendor Management Framework

In today’s dynamic business landscape, establishing an efficient vendor management framework is imperative for sustainable growth and success.

In this comprehensive guide, we aim to uncover the importance of vendor management framework and provide a step-by-step guide to building a robust framework that aligns with your business needs.

What is a Vendor Management Framework?

A vendor management framework is a structured approach that businesses use to oversee and optimize interactions with their vendors. It encompasses strategies, processes, and policies that guide the entire vendor management lifecycle, from onboarding to evaluation.

The framework guides how a company evaluates, selects, and monitors the vendors to make sure they meet the company’s standards for quality, security, and compliance. The aim is to maintain healthy relationships and reduce risks.

Why do Businesses Need a Vendor Management Framework?

A vendor management framework is essential for businesses to control costs, manage risks, ensure quality, and build strong collaborative relationships with vendors , ultimately contributing to the overall success and sustainability of the business. Listed below are the top five reasons businesses need a vendor management framework.

Risk Mitigation: A standardized framework allows you to identify, assess, and mitigate risks associated with vendor relationships.

Cost Efficiency: By streamlining vendor management processes, businesses can optimize costs, negotiate better deals, and enhance overall financial performance.

Regulatory Compliance: Adhering to industry regulations becomes more manageable with a well-defined framework, reducing legal and compliance risks.

Enhanced Performance: A structured approach fosters collaboration, leading to improved vendor performance and, consequently, better service delivery.

Better Visibility: Implementing a vendor management framework enhances real-time visibility into the procurement process which is crucial for both the organization and its vendors. It ensures that all stakeholders have access to the most up-to-date information, fostering transparency and trust.

Types of Vendor Management Framework

Let’s take a look at the three crucial types of vendor management frameworks:

Centralized Framework: Consistency

In a centralized framework, all vendor management activities are consolidated under a central team. This ensures consistency in processes and allows for centralized control over vendor relationships. Standardized procedures and unified decision-making contribute to a collaborative and efficient vendor management approach.

Decentralized Framework: Autonomy

In a decentralized framework, different business units or departments independently manage their vendor relationships. This structure provides autonomy to units, enabling them to tailor vendor management to their specific needs. However, this framework may result in inconsistent processes and lack holistic visibility over vendor relationships.

Hybrid Framework: Flexibility

The hybrid framework strikes a balance by incorporating elements of both centralized and decentralized models. It allows for flexibility at the departmental level while maintaining overall control and collaboration. This hybrid approach is beneficial for organizations with diverse business units, offering adaptability without sacrificing the need for standardized processes.

Step-by-Step Guide to Building a Vendor Management Framework

Step 1: Define Objectives

Clearly outline the goals and objectives of your vendor management framework and align them with organizational goals.

Step 2: Conduct Risk Assessment

Identify potential risks associated with vendor relationships and categorize them based on impact and likelihood.

Step 3: Vendor Segmentation

Classify vendors based on criticality, value, and the nature of the services or products they provide. Tailor management strategies according to each segment.

Step 4: Establish Vendor Criteria

Define criteria for vendor selection, evaluation, and ongoing monitoring. Consider factors such as financial stability, performance history, and compliance.

Step 5: Develop Standardized Processes

Create standardized processes for vendor onboarding, performance measurement, and issue resolution. Ensure consistency and transparency in dealings with all vendors.

Step 6: Implement Technology Solutions

Leverage vendor management software to automate and streamline processes. Use technology for performance tracking, compliance management, and data analytics.

Step 7: Training and Communication

Provide training to internal stakeholders involved in vendor management. Establish clear communication channels to ensure alignment with the framework.

Step 8: Continuous Monitoring and Evaluation

Implement ongoing monitoring mechanisms to assess vendor performance. Regularly evaluate the effectiveness of the framework and make necessary adjustments.

By adhering to these steps, you can establish a vendor management process that suits the specific business needs. It’s crucial to note that this process would not be identical for every company; customization is necessary to align it with your unique requirements.

Essential Questions You Should Ask Before Building a Vendor Management Framework

When formulating a robust vendor management framework for your organization, consider the following key questions to guide your approach:

What Are Our Primary Objectives?

Clearly define the main goals and outcomes you intend to achieve through the vendor management framework. Are you prioritizing cost efficiency, risk mitigation, quality assurance, or a combination of these?

How Much Control Do We Aim for?

Determine the desired level of control over vendor selection and performance. Are you seeking a closely managed process, or prefer a more flexible approach that allows vendors a degree of autonomy?

What Expertise is Crucial?

Assess the required knowledge and skills for those overseeing vendor management. What expertise should individuals responsible for vendor relationships possess to make informed decisions?

How Will We Measure Vendor Performance?

Clearly outline the criteria and metrics for evaluating vendor performance. What benchmarks will be used to ensure vendors meet your organization’s standards and expectations?

How Will We Adapt to Change?

Anticipate the need for flexibility and adaptability in your framework. How will your vendor management process respond to changes in the business environment, technology, or industry regulations?

Closing Thoughts

The foundation for a robust vendor management system lies in the thoughtful planning and implementation of a vendor management framework. While navigating the complexities of vendor management may seem frustrating, the above steps provide a roadmap to a sustainable and effective framework tailored to your unique business needs. This framework not only sets the standards for vendor engagement but also plays a vital role in enhancing relationships between vendors and organizations.

Customization is key, recognizing that there’s no one-size-fits-all solution. To streamline the vendor management process, leverage technology such as Peakflo’s vendor management portal , which lets you customize according to your business needs.

Q: What are the steps of the vendor selection framework?

Ans: The vendor selection framework involves five key steps. First, define your requirements clearly. Second, evaluate potential vendors based on these requirements. Third, evaluate proposals from the shortlisted vendors. Fourth, negotiate and finalize the agreement with the selected vendor. Finally, establish ongoing vendor management processes to ensure the relationship remains successful.

Q: What are the components of vendor management? Ans: Vendor management encompasses several key components. These include vendor selection and onboarding, where vendors are selected based on predefined criteria and onboarded into the organization’s systems. It also involves contract management, performance management, risk management, communication and collaboration, and continuous improvement efforts to enhance the relationship and outcomes.

Q: What are the stages of managing a vendor? Ans: Managing a vendor involves four main stages. The first stage is onboarding, where the vendor relationship is established and necessary agreements are put in place. The second stage is monitoring the vendor’s performance to ensure it meets expectations and addressing any issues promptly. The third stage is regular review and assessment to identify areas for improvement. The final stage involves making decisions about renewing or terminating the vendor relationship based on performance and other relevant factors.

- accounts payable

5 Advantages of Cloud-Based Invoice Approval

Automating workflows with invoice approval software, benefits of payment automation in streamlining accounts payable, latest post, inverting the finance function pyramid: ai-powered cash application, inverting the finance function pyramid: ai-powered 3-way matching, invert finance function pyramid: ai-powered compliance check, peakflo renews soc 2 type 2 certification, ai-powered invoice processing for multi-entity companies.

- Accounts Payable

- Accounts Receivable

- Travel and Expense Management

- B2B Payment Software

- Invoice Management

- Procurement Software

- Product Tour

- Saving Calculator

© 2023 by Peakflo. All rights reserved.

The ultimate guide to effective vendor management: Overcoming challenges and best practices

In today's business landscape, organizations of all sizes rely on vendors to fulfill their resource requirements and execute projects. Vendor management plays a crucial role in ensuring that these relationships are successful, cost-effective, and aligned with the organization's goals and objectives. However, managing vendors can present a range of challenges that can hinder efficiency and productivity.

In this comprehensive guide, we will explore the concept of vendor management, its importance, the challenges associated with it, and the best practices to overcome those challenges. Whether you are a small business or a large enterprise, understanding effective vendor management is essential for optimizing your procurement processes, reducing risks, and maximizing the value derived from your vendor relationships.

Table of contents

- The importance of vendor management

- Understanding vendor management

- Challenges in vendor management

3.1 Lack of transparency in vendor spend

3.2 vendor segmentation and risk assessment, 3.3 vendor collaboration and communication, 3.4 vendor performance management.

- Best practices for effective vendor management

4.1 Establishing clear vendor management goals

4.2 implementing a vendor management system, 4.3 developing strong vendor relationships, 4.4 ensuring compliance and risk mitigation, 4.5 regular communication and collaboration, 4.6 vendor performance measurement and evaluation.

- The vendor management process

5.1 Vendor qualification

5.2 vendor onboarding, 5.3 ordering and delivery, 5.4 vendor payment, 5.5 vendor offboarding.

- The role of technology in vendor management

6.1 Vendor management software

6.2 automated procurement systems, 1. the importance of vendor management.

Vendor management is a critical component of effective procurement and supply chain management. It enables organizations to control costs, mitigate risks, ensure quality and timely delivery of goods and services, and maintain strong relationships with their vendors. By actively managing vendors, businesses can optimize their procurement processes, streamline operations, and enhance overall organizational efficiency.

Effective vendor management also allows businesses to align their vendor relationships with their strategic goals and objectives. It facilitates collaboration and communication between buyers and vendors, leading to better outcomes and mutual success. Moreover, successful vendor management helps businesses to protect their brand reputation, comply with regulations, and achieve greater customer satisfaction.

2. Understanding vendor management

Vendor management is a systematic approach to managing relationships with external suppliers or vendors. It involves various activities such as vendor selection, contract negotiation, performance measurement , and ongoing relationship management. The vendor management process aims to ensure that vendor relationships are aligned with the organization's goals and objectives, and that vendors meet the organization's expectations in terms of quality, cost, and delivery.

A well-defined vendor management process begins with establishing clear vendor management goals and objectives. It involves identifying the specific needs and requirements of the organization, evaluating potential vendors, negotiating contracts, and monitoring and evaluating vendor performance. Effective vendor management requires regular communication, collaboration, and feedback between the organization and its vendors.

3. Challenges in vendor management

While vendor management offers numerous benefits, it also presents several challenges that organizations need to overcome. Understanding and addressing these challenges is crucial for successful vendor management and optimizing procurement processes. Let's explore some of the common challenges in vendor management and how to overcome them.

One of the major challenges in vendor management is the lack of transparency in vendor spend. Organizations often struggle to accurately track and manage the amount spent on each vendor, leading to hidden costs and indirect spends. Manual tracking of vendor spend can be time-consuming and prone to errors.

To overcome this challenge, organizations can implement an automated procurement system that injects transparency into the procure-to-pay process. By automating the tracking of vendor spend, organizations can gain visibility into their vendor-related expenses, identify cost-saving opportunities, and streamline financial processes.

Another challenge in vendor management is vendor segmentation and risk assessment. Organizations need to categorize their vendors based on factors such as profitability and exposure to risks. Small businesses may prefer a simple vendor segmentation process, while large enterprises with a large supplier base may opt for more sophisticated methods such as the Kraljic Matrix.

To overcome this challenge, organizations should invest time and effort in evaluating vendors based on their experience, quality commitment, resources, and track record. Conducting thorough risk assessments and segmenting vendors based on their risk and profitability can help organizations make informed decisions and mitigate potential risks.

Effective collaboration and communication with vendors is crucial for successful vendor management. However, relying solely on emails and messengers for communication can be inefficient and may lead to miscommunication or delays in project execution.

Cloud-based digital vendor management tools can significantly enhance collaboration and communication with vendors. These tools provide a centralized platform for communication, document sharing, and real-time updates, enabling organizations to streamline vendor collaboration and ensure effective communication throughout the procurement process.

Measuring and analyzing vendor performance is essential for organizations to save costs, mitigate risks, and drive value from their vendor relationships. However, without a centralized data repository and effective vendor performance management processes, organizations may struggle to gather and analyze vendor performance data.

To overcome this challenge, organizations can leverage vendor management solutions that provide a centralized platform for storing and managing vendor-related information. These solutions often come with built-in reporting modules that make it easier to measure and evaluate vendor performance, identify areas for improvement, and drive better outcomes from vendor relationships.

4. Best practices for effective vendor management

To overcome the challenges in vendor management and achieve optimal results, organizations should adopt best practices that align with their goals and objectives. Implementing these best practices can help organizations establish strong vendor relationships, optimize procurement processes, and drive value from their vendor partnerships. Let's explore some of these best practices in detail.

The first step towards effective vendor management is to establish clear goals and objectives. By setting specific and measurable goals, organizations can align their vendor relationships with their overall business strategy. These goals can include cost reduction, quality improvement, timely delivery, innovation, and sustainability.

Having well-defined goals enables organizations to evaluate potential vendors based on their ability to contribute towards these goals. It also helps in setting performance metrics and expectations for vendors, ensuring that they understand the organization's requirements and deliver accordingly.

To streamline and automate vendor management processes, organizations should consider implementing a vendor management system. A vendor management system provides a centralized platform for managing vendor information, contracts, performance data, and communication.

Building strong and mutually beneficial relationships with vendors is crucial for successful vendor management. Organizations should focus on establishing open and transparent communication channels with their vendors, fostering trust and collaboration.

Regularly engaging with vendors through meetings, site visits, and feedback sessions can help develop a deeper understanding of their capabilities and challenges. By treating vendors as partners rather than just suppliers, organizations can create an environment of mutual respect and commitment.

Compliance with regulations and risk mitigation are essential aspects of effective vendor management. Organizations should establish clear policies and procedures for vendor selection, contract negotiation, and ongoing vendor management.

Regularly monitoring and evaluating vendor compliance with these policies and procedures helps mitigate risks and ensure that vendors adhere to ethical and legal standards. Organizations should also conduct periodic risk assessments to identify potential risks associated with vendors and take appropriate measures to mitigate those risks.

Effective communication and collaboration are vital for successful vendor management. Organizations should establish regular communication channels with their vendors to exchange information, address issues, and provide feedback.

Cloud-based vendor management tools can facilitate real-time communication, document sharing, and collaboration between organizations and their vendors. By utilizing these tools, organizations can streamline communication processes, reduce response times, and enhance overall collaboration with vendors.

Measuring and evaluating vendor performance is critical for optimizing vendor relationships and driving value. Organizations should establish clear performance metrics and key performance indicators (KPIs) to assess vendor performance.

Regularly evaluating vendor performance against these metrics helps organizations identify areas for improvement, provide feedback to vendors, and make informed decisions about vendor relationships. It also enables organizations to recognize top-performing vendors and incentivize their continued excellence.

5. The vendor management process

The vendor management process involves several stages and activities that organizations need to follow to effectively manage their vendors. By implementing a structured and systematic approach, organizations can ensure that their vendor relationships are well-managed and aligned with their goals and objectives. Let's explore the key stages of the vendor management process.

The vendor qualification stage involves assessing potential vendors based on their expertise, capabilities, and track record. Organizations should evaluate vendors against specific criteria such as experience, quality commitment, resources, and financial stability.

By thoroughly vetting potential vendors, organizations can ensure that they choose vendors who are best suited to meet their requirements and contribute to their goals. Vendor qualification also involves conducting due diligence, verifying vendor credentials, and assessing their compliance with regulatory and ethical standards.

Once vendors have been qualified and selected, the next step is vendor onboarding. This stage involves collecting and capturing all relevant vendor information and documentation, such as contact details, contract terms, insurance certificates, and financial data.

Organizations should establish a centralized database or vendor management system to store and manage vendor information. By streamlining the onboarding process, organizations can ensure that vendors are onboarded efficiently and that all necessary information is collected and verified.

The ordering and delivery stage involves initiating purchase orders or contracts with vendors for specific goods or services. Organizations should clearly define the specifications, requirements, and timelines for the orders to ensure that vendors understand and deliver accordingly.

Once the goods or services are delivered, organizations should conduct quality checks to ensure that they meet the specified requirements. Timely and accurate delivery is critical for maintaining operational efficiency and meeting customer expectations.

After the goods or services have been delivered and verified, organizations need to process vendor payments. This stage involves matching invoices with purchase orders, verifying the accuracy of the invoices, and approving them for payment.

Timely payment of vendors is crucial for maintaining strong vendor relationships and ensuring continued service delivery. Organizations should establish clear payment terms and processes to streamline the payment process and avoid delays or disputes.

When a contract ends or a vendor relationship terminates, organizations need to offboard the vendor from their systems and records. This stage involves removing the vendor from finance and administrative records, updating databases, and ensuring compliance with contractual obligations.

Proper vendor offboarding is essential for maintaining data integrity, compliance, and security. Organizations should follow established procedures for vendor offboarding to minimize any disruption to their operations.

6. The role of technology in vendor management

Technology plays a crucial role in streamlining and enhancing vendor management processes. Organizations can leverage various tools and solutions to automate and optimize their vendor management activities. Let's explore some of the key technologies that can support effective vendor management.

Vendor management software provides organizations with a centralized platform for managing vendor information, contracts, performance data, and communication. These software solutions often come with features such as vendor onboarding, contract management, performance measurement, and communication tools.

Assembled's purpose-built vendor management solution offers organizations a comprehensive and user-friendly platform for managing all aspects of vendor management. With features like vendor onboarding, contract management, performance measurement, and communication tools, businesses can enhance their vendor management processes and improve overall efficiency.

Automated procurement systems can significantly enhance vendor management processes by streamlining and automating various activities. These systems provide organizations with end-to-end visibility into their procurement processes, from requisition to payment.

Automated procurement systems enable organizations to streamline vendor qualification, contract negotiation, ordering, delivery, and payment processes. These systems often come with features such as purchase requisition management, vendor selection and evaluation, contract management, and invoice processing. By automating these processes, organizations can improve efficiency, reduce errors, and optimize their procurement operations.

7. Conclusion

Effective vendor management is essential for organizations to optimize their procurement processes, reduce risks, and derive maximum value from their vendor relationships. By understanding the challenges in vendor management and adopting best practices, organizations can overcome these challenges and establish strong, mutually beneficial relationships with their vendors.

The vendor management process, from vendor qualification to offboarding, provides a systematic framework for managing vendor relationships and ensuring that vendors meet the organization's expectations. Leveraging technology, such as vendor management software and automated procurement systems, can further enhance the efficiency and effectiveness of vendor management processes.

As organizations strive for BPO efficiency and operational excellence, investing in effective vendor management becomes crucial. By implementing the best practices outlined in this guide and leveraging technology, organizations can optimize their vendor management processes and drive better outcomes from their vendor relationships.

Remember, effective vendor management is an ongoing process that requires continuous evaluation, improvement, and adaptation. By prioritizing vendor management and adopting a proactive approach, organizations can build strong, long-lasting vendor relationships and achieve their procurement goals and objectives.

Now that you have a comprehensive understanding of effective vendor management, it's time to apply these principles and best practices to your own organization. Embrace the challenges, implement the best practices, and leverage technology to transform your vendor management processes and unlock the true potential of your vendor relationships.

Disclaimer: The information provided in this article is for informational purposes only and should not be considered as professional advice. Organizations should consult with their own legal and procurement experts to ensure compliance with applicable laws and regulations.

Related content

5 vendor management best practices for businesses

"vendor business plan")

Published on February 20, 2024

"vendor business plan")

As businesses grow and expand, it becomes less feasible for them to run every operation on their own. Companies outsource services and products to reduce the workload of their internal teams, and to boost business growth and productivity.

But working with third-party service providers comes with its own challenges, from risk assessment and pricing negotiations, to building long-term vendor relationships and optimizing cost savings .

Given the fact that vendor management is a multidisciplinary business practice that spans several teams and often involves executive oversight, many companies find it to be a complicated and stressful process.

The good news is there are several strategies that teams of all sizes can implement to handle vendor management more effectively. In addition to applying vendor management best practices that we’ll break down in this post, companies can also invest in spend or vendor management software, which use process automation and spend analysis to optimize business and finance operations .

What is vendor management?

The main goal of vendor management is building, maintaining, and strengthening mutually-beneficial supplier relationships that drive company success. This success can have multiple definitions, e.g. lowering business costs, increasing output, or driving product innovation.

There are many elements involved in this complex business practice, but effective vendor management should always consider the following:

Risk assessment - Naturally, there is increased security risk when businesses outsource projects to third-party vendors, and companies should have policies in place to mitigate this risk. Beyond avoiding high-risk collaborations, it’s imperative to have a solid framework and action plan for financial, legal, and even reputational liability in active partnerships.

Fit - When developing relationships and selecting external suppliers, both vendor and client need to clearly communicate their needs and expectations. The benefits of the collaboration should be reciprocal and remain so throughout the duration of the contract. Thoroughly review the terms of the contract (including penalties for breaching it) and make sure all parties involved are in agreement before proceeding.

Pricing - If a vendor’s prices exceed your allocated budget, finance will tell you they’re not the right fit. Details like billing frequency and rates, as well as payment methods and processes, should be clearly laid out and validated on both sides.

Finance teams aim to increase the value of outsourced staffing and products by controlling the overall vendor costs, while vendor-facing teams focus on improving vendor performance. Businesses often use finance tools like spend management software or a warehouse management system to organize their company’s vendor database.

5 vendor management best practices

Depending on team structures and company activities, the procurement process can be executed quite differently from one department to another. Be aware that major inconsistencies in vendor selection criteria can cause inefficiencies across the company or harm vendor relationships.

From sourcing the best suppliers and negotiating deals, to processing invoice payments and measuring vendor performance–there’s a lot to handle, even when everything is going as planned.

For that reason, every business should develop transparent and consistent processes for handling vendor relations and contracts. Optimize vendor management within your organization with these best practices:

1. Enforce a clear vendor management policy

Today there are increasing data security concerns when working with third-party service providers. Your company should have formal documentation that informs all teams, leadership and board members of the official vendor management policy.

Like any other business function, vendor management processes should be periodically reviewed and updated over time to improve performance, operations, and costs. Assign an internal committee with team members that are SME (subject matter experts) to oversee specific steps of the vendor management process, based on their professional knowledge or expertise.

For internal accountability, always include a clear outline in the policy that details official committee roles and what they are responsible for.

2. Choose the right vendors for your business

Finding the best suppliers for your business is all about strategic sourcing . Great vendors provide high quality service at an affordable price that consistently increases your company’s overall performance and competitive edge in the market.

That means you should follow a set of standards when it comes to picking vendors, even if you only need a one-time solution. To develop strong vendor partnerships for your business, look for these qualities:

Expertise . Your business will benefit most from vendors that are experts in your unique industry. Vendors who provide niche products or services that you need are more likely to understand the nuances of your business operations and market, giving both parties a competitive advantage.

Stability . Get a good sense of vendors’ financial stability, as this will have an effect on your own business. Assess whether they have a sound business model, and if they have stable partnerships with other similar clients in your field.

Due diligence . Before signing a contract with a new vendor, review their professional history, media presence, and client roster. This can help determine whether the vendor is safe to work with, is legally regulated and compliant, and serious about their data privacy and security.

Investing in smarter procurement builds healthy long-term relationships that will bring your business positive returns over time. Companies save significant time and money when they have an updated database of trustworthy and reliable vendors that they can immediately reach out to whenever necessary.

3. Proactively manage and nurture vendor relationships

A large part of vendor management is vendor relationship management. Nurturing supplier relationships is critical to balancing a healthy collaboration that delivers concrete benefits to both businesses.

This means exchanging honest feedback and staying flexible throughout the partnership, especially when negotiating prices or dealing with unexpected issues that may arise. To avoid miscommunication, it's imperative to be as transparent and specific as possible when detailing your expectations and needs–and your vendors should do the same.

Knowing when to compromise is a high-value skill here, as small concessions can lead to bigger returns in the long run for both businesses.

4. Monitor and track vendor spend

Maintaining control over your business spend is necessary for sustained growth. Yet manually tracking vendor spend is a laborious challenge for companies that want to scale their vendor management processes.

Spend management softwares like Spendesk are powerful online solutions that help companies run vendor management more smoothly. Finance teams gain increased visibility and control over company spending with advanced features that enable them to:

Track and reconcile every business transaction from one centralized platform, with real-time overview of all budgets and spend activity

Optimize finances by pinpointing the best cost savings opportunities

Manage all SaaS vendors and recurring payments automatically

Prevent and eliminate duplicate and redundant SaaS subscriptions with a click

Create unique payment cards with allocated budgets for individual or multiple vendors

Easily review vendor details and employee contacts on any transactions

To optimize vendor spending with these tools, businesses analyze and identify actionable insights or trends from their spend data and activity. Often, this may also require a deeper look at the qualitative performance of your vendors.

5. Measure vendor performance

It’s important to define what success looks like from the start of your collaboration, in order to set realistic expectations with your vendors and lay out how performance will be measured. This could be identifying the relevant KPIs (key performance indicators) for your industry or determining what kinds of qualitative results are important to your team. As KPIs are not static, it’s good to periodically review your shared business goals based on market changes or product updates.

Having a diverse array of data points and metrics helps you measure the true impact of vendor performance, and comparing these results against vendor spend gives you a better picture of your business ROI.

Evaluating vendor performance with both quantitative and qualitative factors enables you to accurately determine whether vendors are meeting expectations, underperforming, or even over-performing. Conducting in-depth reviews with your vendor also enables you to identify if business needs have changed, or if there are new opportunities to act on together.

Transform vendor management with smart spending

It’s evident that vendor management is no simple task. Finding the right balance of efficient logistics with reciprocal relationships is full of complex nuances. But with automation softwares like Spendesk and resources that drive smarter spend management and procurement , consolidating your company’s vendor management processes into a streamlined workflow is effortless.

Finance teams and budget managers can monitor, track, and approve spend in a few clicks, while vendor-facing team members can instantly get access to the funds they need on personalized company cards –all from one central dashboard. Strengthen your vendor relationships and empower your finance team with better processes using Spendesk’s complete spend management platform.

More reads on Finance Insights

"vendor business plan")

24 CFO blogs, resources, guides & events to grow as a leader

"vendor business plan")

How machine learning in finance automates repetitive tasks

"vendor business plan")

HMRC PAYE: a guide for employees and employers

Get started with spendesk.

Close the books 4x faster , collect over 95% of receipts on time , and get 100% visibility over company spending.

ZenBusinessPlans

Home » Sample Business Plans » Food

A Sample Hot Dog Vendor Business Plan Template

A hot dog vendor business is a business that sells different types of hot dogs and drinks from a shop, cart, or food truck. Hot dogs are prepared commercially by mixing the ingredients (meats, spices, binders, and fillers) in vats where rapidly moving blades grind and mix them all together. This mixture is forced through tubes for cooking.

The market size of the Hot Dog and Sausage Production industry is $19.2bn in 2023 and the industry is expected to increase by 3.6 percent going forward. in 2023, Americans spent more than $7.5 Billion on hot dogs and sausages in US Supermarkets. So also, 95 percent of American homes eat hot dogs; the average U.S. resident consumes about 70 hot dog pieces per year.

Steps on How to Write a Hot Dog Vendor Business Plan

Executive summary.

Tasty Tasha™ Hot Dog Company, Inc. is a registered hot dog and sausage business that will be located on one of the busiest roads in Tinton Falls, New Jersey. We have been able to lease a facility along a major road that can fit into the kind of hot dog and sausage restaurant that we intend launching and the facility is located in a corner piece property directly opposite the largest residential estate in Tinton Falls, New Jersey.

At Tasty Tasha™ Hot Dog Company, Inc., we will make our hot dogs with only the healthiest and freshest ingredients. Tasha Jordan is the founder and CEO of Tasty Tasha™ Hot Dog Company, Inc.

Company Profile

A. our products and services.

Tasty Tasha™ Hot Dog Company, Inc. will be involved in the sale of;

- Different types of hot dogs

- Different types of sausages

- Beverages and water.

b. Nature of the Business

Our hot dog shop will operate the business-to-consumer business model.

c. The Industry

Tasty Tasha™ Hot Dog Company, Inc. will operate in the hot dog and sausage production industry.

d. Mission Statement

Our mission is to make hot dogs and related snacks that will be irresistible to a wide range of customers.

e. Vision Statement

We want to be known as a hot dog company with a unique recipe and product.

f. Our Tagline (Slogan)

Tasty Tasha™ Hot Dog Company, Inc. – Mouth-Watering Hot Dog Is Our Specialty!

g. Legal Structure of the Business (LLC, C Corp, S Corp, LLP)

Tasty Tasha™ Hot Dog Company, Inc. will be formed as a Limited Liability Company (LLC). The reason why we are forming an LLC is to protect our assets by limiting the liability to the resources of the business itself. The LLC will protect our CEO’s assets from claims against the business, including lawsuits.

h. Our Organizational Structure

- Chief Executive Officer (Owner)

- Shop Manager

- Accountant (Cashier)

- Hot Dog Makers

- Salesgirls and Salesboys

i. Ownership/Shareholder Structure and Board Members

- Tasha Jordan (Owner and Chairman/Chief Executive Officer) 52 Percent Shares

- Garry Button (Board Member) 18 Percent Shares

- Christian Norman (Board Member) 10 Percent Shares

- Eden Jobs (Board Member) 10 Percent Shares

- Blessing Oliver (Board Member and Sectary) 10 Percent Shares.

SWOT Analysis

A. strength.

- Ideal location for a hot dog and sausage shop

- Highly experienced and qualified employees and management

- Access to finance from business partners

- Access to ingredients and supplies.

- A reliable, clean, healthy, and efficient method of preparing hot dogs and sausages.

b. Weakness

- Financial Constraints

- A new business that will be competing with well-established hot dog shops and fast-food restaurants.

- Inability to retain our highly experienced and qualified employees longer than we want

c. Opportunities

- A rise in people who want to experiment with hot dogs and sausages

- Online market, new services, new technology, and of course the opening of new markets

i. How Big is the Industry?

Trust me, the market for hot dogs and sausages is massive in the United States of America. This is supported by the fact that in 2023 Americans spent more than $7.5 Billion on hot dogs and sausages in US Supermarkets. So also, 95 percent of American homes eat hot dogs; the average U.S. resident consumes about 70 hot dogs per year.

ii. Is the Industry Growing or Declining?

The hot dog business is really growing. The market size of the hot dog and sausage production industry in the US grew 2.0 percent per year on average between 2017 and 2022.

iii. What are the Future Trends in the Industry

The future trends when it comes to hot dogs and sausage shops will revolve around technology. There will be new software that can predict what customers want from a hot dog shop.

iv. Are There Existing Niches in the Industry?

No, there is no existing niche idea when it comes to the hot dog and sausage line business because the business is a subset of the hot dog and sausage production industry.

v. Can You Sell a Franchise of your Business in the Future?

Tasty Tasha™ Hot Dog Company, Inc. has plans to sell franchises in the nearest future and we will target major cities with thriving markets in the United States of America.

- The arrival of a new hot dog shop or even fast-food restaurant within our market space

- Unfavorable government policy and regulations.

- Steady wage expenses

- Economic uncertainty

- Liability problems

- The U.S. Food and Drug Administration (FDA) could change its regulatory status and decide to enforce strict regulations that can strangulate new businesses like ours.

i. Who are the Major Competitors?

- Tyson Foods Inc.

- Smithfield Foods Inc.

- The Kraft Heinz Company

- Conagra Foods Inc.

- Rutt’s Hut.

- Superdawg Drive-In.

- Nathan’s Famous – Coney Island.

- Yocco’s.

- Olneyville NY System Restaurant.

- Lafayette Coney Island.

- American Coney Island.

- Gene & Jude’s

- Ben’s Chili Bowl

- Hillbilly Hot Dogs

- El Guero Canelo

- The Wiener’s Circle

- Biker Jim’s Gourmet Dogs

- The Happy Dog.

ii. Is There a Franchise for Hot Dog and Sausage business?

Yes, there are franchise opportunities for hot dog and sausage shops. Here are they;

- The Original Hot Dog Factory

- Nathan’s Famous Inc. Franchises

- Wienerschnitzel Franchises

- Hot Dog on a Stick Franchises

- Dog Haus Worldwide Franchises

- Sonic Drive-In Franchises

- Johnnie’s Dog House

- Dave’s the Dog House LLC Franchises

- Umai Savory Hot Dogs Franchises

- Dat Dog Specialty Franchises

- Destination Dogs

- Sam’s Hot Dog Stand.

iii. Are There Policies, Regulations, or Zoning Laws Affecting Hot Dog and Sausage Shop?

Yes, there are county or state regulations or zoning laws for hot dog and sausage shop businesses. Players in this industry are expected to work with existing regulations governing similar drinks and food-related businesses in the county where their business is domiciled.

The regulation of the industry is shared by the FDA and the Treasury Department’s Tax and Trade Bureau. Essentially, every hot dog and sausage shop must register with the FDA, and therefore any hot dog and sausage shop is subject to random FDA inspections without warning.

Marketing Plan

A. who is your target audience.

i. Age Range

Our target market comprises people of all ages.

ii. Level of Educational

We don’t have any restrictions on the level of education of those we will welcome to our hot dog shop.

iii. Income Level

There is no cap on the income level of those we will welcome to our hot dog shop.

iv. Ethnicity

There is no restriction when it comes to the ethnicity of the people who will purchase hot dog from us.

v. Language

There is no restriction when it comes to the language spoken by the people that will purchase hot dogs and sausage from us.

vi. Geographical Location

Anybody from any geographical location is free to purchase hot dogs and sausage from us.

vii. Lifestyle

Tasty Tasha™ Hot Dog Company, Inc. will not restrict any customer from purchasing hot dogs and sausage from us based on their lifestyle, culture, or race.

b. Advertising and Promotion Strategies

- Deliberately Brand All Our Vans and Delivery Bikes.

- Tap Into Text Marketing.

- Make Use of Bill Boards.

- Share Your Events in Local Groups and Pages.

- Turn Your Social Media Channels into a Resource

- Develop Your Business Directory Profiles

- Build Relationships with players in the event planning and food services industry.

i. Traditional Marketing Strategies

- Marketing through Direct Mail.

- Print Media Marketing – Newspapers & Magazines.

- Broadcast Marketing -Television & Radio Channels.

- OOH, Marketing – Public Transits like Buses and Trains, Billboards, Street shows, and Cabs.

- Leverage direct sales, direct mail (postcards, brochures, letters, fliers), print advertising (coupon books, billboards), and referral (also known as word-of-mouth marketing).

ii. Digital Marketing Strategies

- Social Media Marketing Platforms.

- Influencer Marketing.

- Email Marketing.

- Content Marketing.

- Search Engine Optimization (SEO) Marketing.

- Affiliate Marketing

- Mobile Marketing.

iii. Social Media Marketing Plan

- Start using chatbots.

- Create a personalized experience for our customers.

- Create an efficient content marketing strategy.

- Create a community for our target market and potential target market.

- Gear up our profiles with a diverse content strategy.

- Use brand advocates.

- Create profiles on the relevant social media channels.

- Run cross-channel campaigns.

c. Pricing Strategy

When working out our pricing strategy, Tasty Tasha™ Hot Dog Company, Inc. will make sure it covers profits, insurance, premium, license, economy or value, and full package. All our pricing strategies will reflect;

- Cost-Based Pricing

- Value-Based Pricing

- Competition-Based Pricing.

Sales and Distribution Plan

A. sales channels.

Our channel sales strategy will involve using partners and third parties—such as referral partners, affiliate partners, strategic alliances in the event planning industry, and the food services industry to help refer customers to us.

Tasty Tasha™ Hot Dog Company, Inc. will also leverage the 4 Ps of marketing which are place, price, product, and promotion. By carefully integrating all these marketing strategies into a marketing mix, we can have a visible, in-demand service that is competitively priced and promoted to our customers.

b. Inventory Strategy

The fact that we will need ingredients (emulsified meat trimmings of chicken, beef, or pork, vegetable oil, all-purpose flour, baking powder, preservatives, spices, and coloring et al), means that we will operate an inventory strategy that is based on a day-to-day methodology for ordering, maintaining and processing items in our warehouse.